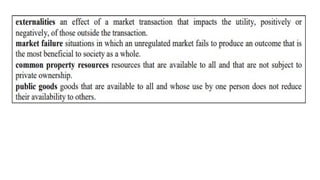

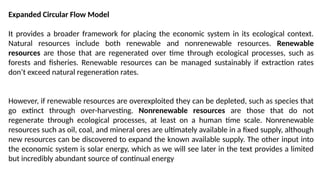

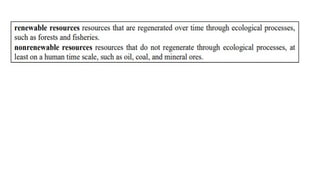

The document discusses the evolution of human economic growth, emphasizing the 400-year boom linked to industrialization, which has simultaneously led to significant environmental degradation. It highlights the emergence of environmental and ecological economics as fields that assess the impact of economic activities on the environment, proposing a pluralistic approach to understanding this relationship. The conclusion underscores the need for sustainable development that balances economic and environmental objectives, considering the limitations of natural resources and ecological systems.

![Pluralistic Approach

• Pluralism the perspective that a full understanding of an issue can

only come from a variety of viewpoints, disciplines, and approaches.

• Core concept in ecological economics is the promotion of a

pluralistic approach to studying the relationship between the

economy and the environment.

•To make ethical conduct central and to place the social, ecological and economic discourses on an

equal footing. . . . Deep ecological economics requires challenging both personal and social pre-

conceptions, while taking a campaigning sprit to change public policy and the institutions blocking

the necessary transition to [alternative economic systems].](https://image.slidesharecdn.com/lecture1-250210103819-54070350/85/Resource-and-Environmental-Economics-lect-21-320.jpg)

![NR_chapter_one_and_two_-2024[1].pptx eco](https://cdn.slidesharecdn.com/ss_thumbnails/nrchapteroneandtwo-20241-240802123027-ab512880-thumbnail.jpg?width=640&height=640&fit=bounds)