Download to read offline

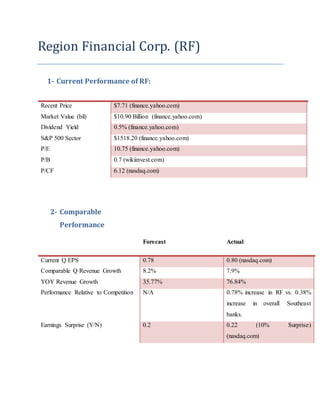

Region Financial Corp (RF) is a regional bank headquartered in Birmingham, Alabama. In the recent quarter, RF beat earnings estimates with EPS of $0.80 compared to the forecast of $0.78. However, revenue growth was lower than expected at 7.9% versus the forecast of 8.2%. The document provides an analysis of RF's current performance, earnings surprise outcome, qualitative analysis of management statements discussing future risks and opportunities, and recommendations to consider buying RF stock.