Recommended

Recommended

More Related Content

What's hot

What's hot (7)

Similar to Redundancy tax planning case study

Similar to Redundancy tax planning case study (20)

Recently uploaded

Recently uploaded (20)

Redundancy tax planning case study

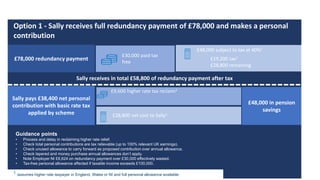

- 1. Tax year end opportunities 1 assumes higher rate taxpayer in England, Wales or NI and full personal allowance available Option 1 - Sally receives full redundancy payment of £78,000 and makes a personal contribution £78,000 redundancy payment £30,000 paid tax free £48,000 subject to tax at 40%1 £9,600 higher rate tax reclaim1 Sally receives in total £58,800 of redundancy payment after tax £19,200 tax1 Sally pays £38,400 net personal contribution with basic rate tax applied by scheme £28,800 net cost to Sally1 £48,000 in pension savings Guidance points • Process and delay in reclaiming higher rate relief. • Check total personal contributions are tax relievable (up to 100% relevant UK earnings). • Check unused allowance to carry forward as proposed contribution over annual allowance. • Check tapered and money purchase annual allowances don’t apply. • Note Employer NI £6,624 on redundancy payment over £30,000 effectively wasted. • Tax-free personal allowance affected if taxable income exceeds £100,000. £28,800 remaining

- 2. Tax year end opportunities Option 2a - Sally agrees with employer to sacrifice £48,000 of redundancy payment in return for employer pension contribution - employer retains NICs saving £78,000 redundancy payment £30,000 tax free redundancy Employer pays contribution of £48,000 and retains NICs saving of £6,624 that would have been payable on amount over £30,000 Sally receives £30,000 tax free redundancy payment £48,000 in employer pension contributions Guidance points • Must be sacrificed before becoming entitled to payment • No tax payable on redundancy element • No tax reclaim process or delays - effectively benefits from higher rate relief immediately • No check against 100% of relevant UK earnings • Check unused allowance to carry forward as proposed contribution over annual allowance • Check tapered and money purchase annual allowances don’t apply • Employer likely to be agreeable to sacrifice if retaining NICs saving. Sally has given up £28,8001 net after tax she would have received if she’d taken full redundancy payment 1 assumes higher rate taxpayer in England, Wales or NI and full personal allowance available

- 3. Tax year end opportunities Option 2b - Sally agrees with employer to sacrifice £48,000 of redundancy payment in return for employer pension contribution - employer adds in its NICs saving £78,000 redundancy payment £30,000 tax free redundancy Employer pays contribution of £48,000 and adds in NICs saving of £6,624 that would have been payable on amount over £30,000 Sally receives £30,000 tax free redundancy payment £54,624 in employer pension contributions Guidance points • Must be sacrificed before becoming entitled to payment • No tax payable on redundancy element • No tax reclaim process or delays - effectively benefits from higher rate relief immediately • No check against 100% of relevant UK earnings • Check unused allowance to carry forward as proposed contribution over annual allowance • Check tapered and money purchase annual allowances don’t apply • Employer may be willing to add part of its NICs saving if not all. Sally has given up £28,8001 net after tax she would have received if she’d taken full redundancy payment 1 assumes higher rate taxpayer in England, Wales or NI and full personal allowance available

- 4. Tax year end opportunities Sally takes benefits immediately Option 1 – personal contribution Option 2a – employer contribution, employer retains NICs saving Pension contributions £48,000 Option 2b – employer contribution, employer adds in NICs saving £48,000 £54,624 Cost to Sally/what Sally gives up £28,800 (net cost after higher rate tax reclaim) £28,800 (net of tax, if redundancy paid in full) £28,800 (net of tax, if redundancy paid in full) £12,000 £12,000 £13,656PCLS Difference £16,800 £16,800 £15,144 £36,000 Funds available to provide income £36,000 £40,968 1 assumes higher rate taxpayer in England, Wales or NI and full personal allowance available