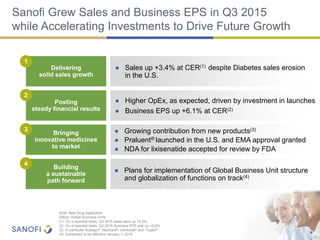

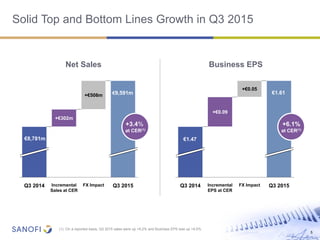

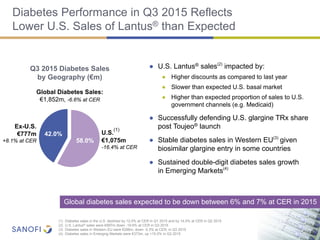

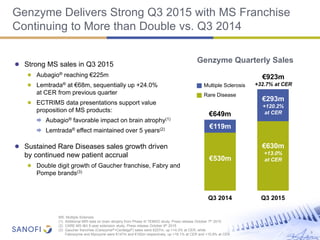

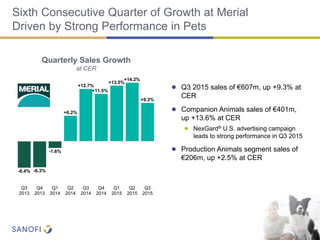

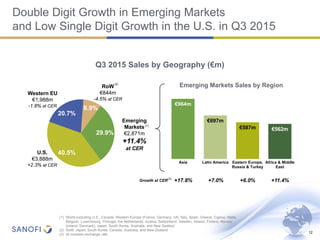

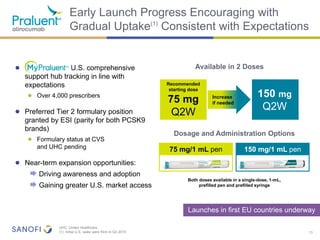

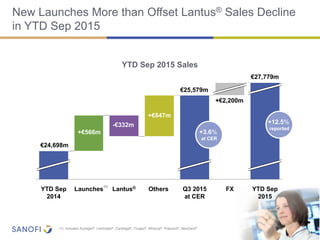

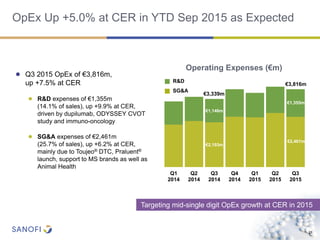

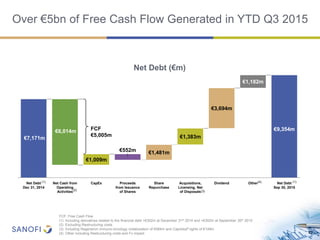

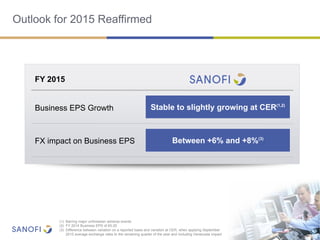

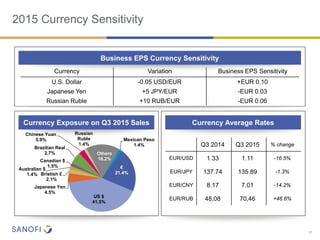

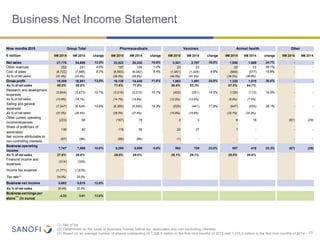

Sanofi reported results for Q3 2015 with sales growing 3.4% at constant exchange rates. Business EPS grew 6.1% at constant exchange rates. While diabetes sales declined 6.6% due to lower sales of Lantus in the US, other businesses such as Genzyme, vaccines, and Merial showed solid sales growth. Praluent was launched in the US and Europe for cholesterol treatment.

![[ls머트리얼즈]LS Materials 417200 Algorithm Investment Report](https://cdn.slidesharecdn.com/ss_thumbnails/lsmaterials417200algorithminvestmentreport-260202182715-66072c7b-thumbnail.jpg?width=640&height=640&fit=bounds)