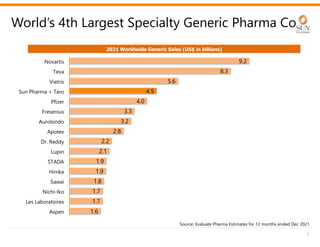

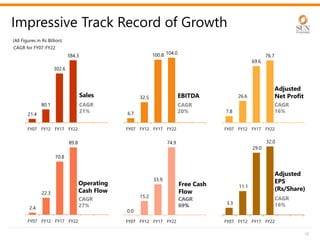

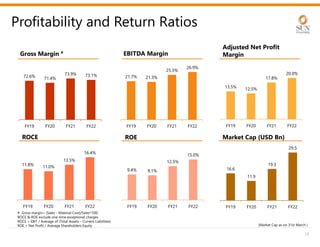

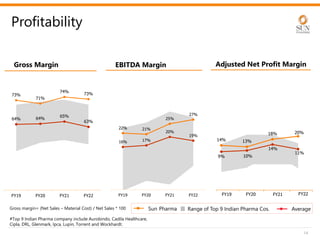

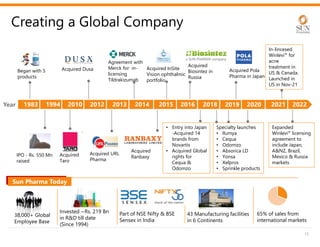

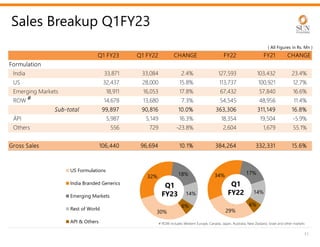

The document provides an investor presentation for Sun Pharmaceutical Industries Limited. It summarizes Sun Pharma's position as the 4th largest global specialty generic company, with a presence in over 100 countries. It outlines Sun Pharma's long-term strategy of enhancing its specialty business portfolio and achieving differentiation through complex products. The presentation provides details on Sun Pharma's revenue composition, history of growth and acquisitions, operations, and financial performance.