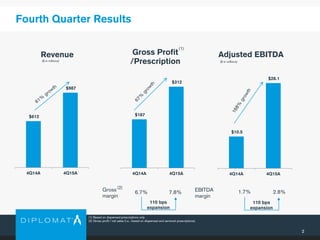

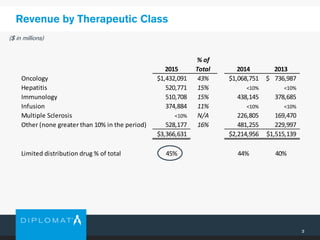

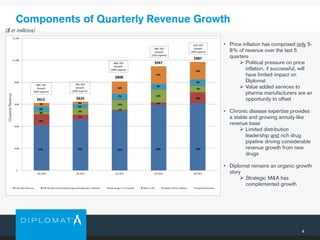

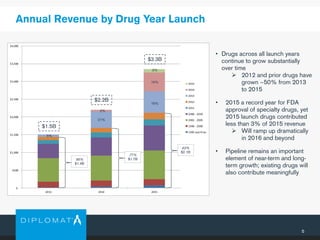

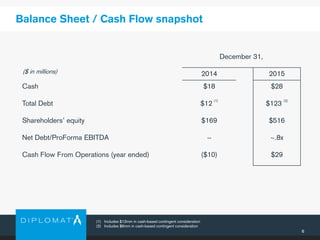

This document summarizes the financial highlights and results of a company for 4Q 2015 and full year 2015. It reported 61% revenue growth in 4Q 2015 and 52% for full year 2015. Gross margins expanded 110 bps in 4Q and 150 bps for the year. Adjusted EBITDA grew 168% in 4Q and 170% for 2015. Revenue was driven by growth in oncology, hepatitis, immunology and other therapeutic classes. The company expects continued strong revenue growth of 32% and adjusted EBITDA growth of 26% in 2016.

![[ls머트리얼즈]LS Materials 417200 Algorithm Investment Report](https://cdn.slidesharecdn.com/ss_thumbnails/lsmaterials417200algorithminvestmentreport-260202182715-66072c7b-thumbnail.jpg?width=640&height=640&fit=bounds)