KGHM International reported its Q1 2013 results, with key highlights including:

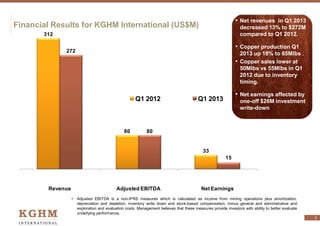

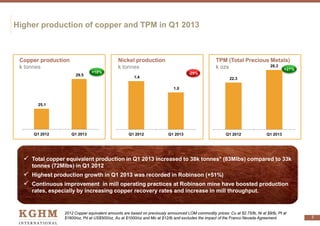

- Copper production increased 18% compared to Q1 2012, to 65 million pounds, while copper sales decreased to 50 million pounds.

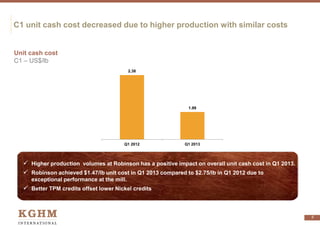

- C1 cash costs decreased to $1.99 per pound of copper, from $2.38 in Q1 2012.

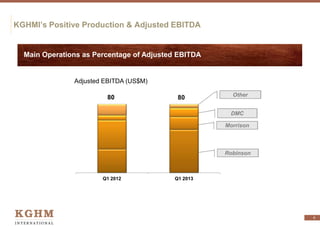

- Adjusted EBITDA remained unchanged at $80 million compared to Q1 2012.

- The Sierra Gorda project in Chile progressed construction and is now 41% complete, on track to begin operations in 2014.