Downloaded 65 times

![An introduction to the consolidation and equity method framework

1-18 PwC

962, respectively. We do not believe that it is intended to require employee benefit

plans to consolidate entities in which they invest.

1.3.3.2 Investment companies

Investment companies generally are not required to evaluate their investees for

consolidation.

ASC 810-10-15-12(d)

Except as discussed in paragraph 946-810-45-3, an investment company within the

scope of Topic 946 [Financial Services-Investment Companies] shall not consolidate

an investee that is not an investment company.

This scope exception only applies to investments that are owned by a reporting entity

that qualifies as an investment company under the guidance of ASC 946 and are

reported at fair value.

The scope exception does not apply to reporting entities that hold interests in an

investment company. An investor, investment adviser, or any other party having an

interest in an investment company entity under ASC 946 must evaluate whether it

should consolidate the investment company.

A reporting entity that consolidates an investment company retains the investment

company’s specialized accounting in the reporting entity’s consolidated financial

statements, as noted in ASC 810.

Excerpt from ASC 810-10-25-15

For the purposes of consolidating a subsidiary subject to guidance in an industry-

specific Topic, an entity shall retain the industry-specific guidance applied by that

subsidiary.

Similarly, a reporting entity that applies the equity method of accounting to an

investment in an investment company would also retain the investee’s specialized

accounting as noted in ASC 323, Investments—Equity Method and Joint Ventures.

See also CG 4.5.6.3.

ASC 323-10-25-7

For the purposes of applying the equity method of accounting to an investee subject to

guidance in an industry-specific Topic, an entity shall retain the industry-specific

guidance applied by that investee.

1.3.3.3 Governmental organizations

In most cases, it would be inappropriate for a reporting entity to consolidate a

governmental organization or a financing entity established by a governmental](https://image.slidesharecdn.com/pwc-consolidation-equity-method-accounting-2015-150930181755-lva1-app6892/85/PwC-Consolidation-Equity-Method-Accounting-2015-44-320.jpg)

![Variable interest entity model

2-6 PwC

2.1.2.4 The business scope exception

Determining whether the VIE model applies to an entity that meets the definition of a

business can be one of the more challenging aspects of ASC 810. The VIE model

provides the following scope exception (the “business scope exception”) for reporting

entities having a variable interest(s) in a business entity.

ASC 810-10-15-17(d)

A legal entity that is deemed to be a business need not be evaluated by a reporting

entity to determine if the legal entity is a VIE under the requirements of the Variable

Interest Entities Subsections unless any of the following conditions exist (however, for

legal entities that are excluded by this provision, other generally accepted accounting

principles [GAAP] should be applied):

1. The reporting entity, its related parties (all parties identified in paragraph 810-10-

25-43, except for de facto agents under paragraph 810-10-25-43(d)), or both

participated significantly in the design or redesign of the legal entity. However,

this condition does not apply if the legal entity is an operating joint venture under

joint control of the reporting entity and one or more independent parties or a

franchisee.

2. The legal entity is designed so that substantially all of its activities either involve

or are conducted on behalf of the reporting entity and its related parties.

3. The reporting entity and its related parties provide more than half of the total of

the equity, subordinated debt, and other forms of subordinated financial support

to the legal entity based on an analysis of the fair values of the interests in the

legal entity.

4. The activities of the legal entity are primarily related to securitizations or other

forms of asset-backed financings or single-lessee leasing arrangements.

A legal entity that previously was not evaluated to determine if it was a VIE because of

this provision need not be evaluated in future periods as long as the legal entity

continues to meet the conditions in (d).

The VIE model addresses situations where the voting interest entity approach may not

identify the party having a controlling financial interest in an entity. When

deliberating FIN 46R, the Board considered, but ultimately opposed, providing a

scope exception for all businesses, believing that such a distinction was contrary to the

principle underlying the VIE model. Therefore, ASC 810-10-15-17(d) is not intended to

provide a scope exception to all businesses.

The business scope exception allows reporting entities to avoid applying the VIE

model in circumstances where it is unlikely that the reporting entity would be

required to consolidate the entity (as the primary beneficiary), even if the entity is a

VIE. The Board concluded that the most useful way to provide this implementation](https://image.slidesharecdn.com/pwc-consolidation-equity-method-accounting-2015-150930181755-lva1-app6892/85/PwC-Consolidation-Equity-Method-Accounting-2015-69-320.jpg)

![Variable interest entity model

PwC 2-69

□ Evaluate whether the holders of equity at risk, as a group, have the power,

through voting rights or similar rights, to direct the entity’s most significant

activities.

□ If decision making has been outsourced to one of the at-risk equity investors

through a separate variable interest that does not qualify as equity at risk,

determine whether the decision making rights conveyed through that other

variable interest are embedded in the investor’s equity investment.

□ If the holders of equity at risk, as a group, lack rights that constrain the decision

maker’s level of authority, consider whether a single party has substantive kick-

out or participating rights over the decision maker.

Applying Characteristic 2 to limited partnerships and similar entities

ASU 2015-02 introduced a separate analysis when applying Characteristic 2 to limited

partnerships and similar entities. This requirement was added based on the unique

purpose and design of limited partnerships as compared to corporations. Entities that

are determined to be “similar” to limited partnerships would also be subject to this

new requirement. For example, some entities may be similar to a limited partnership

if they have a governance structure that is the functional equivalent of a limited

partnership’s governance structure.

Excerpt from ASC 810-10-15-14(b)

ii. For limited partnerships, partners lack that power if neither (01) nor (02) below

exists. The guidance in this subparagraph does not apply to entities in industries (see

paragraphs 910- 810-45-1 and 932-810-45-1) in which it is appropriate for a general

partner to use the pro rata method of consolidation for its investment in a limited

partnership (see paragraph 810-10- 45-14). [Content amended as shown and moved

from paragraph 810-20-15-3(c)]

01. A simple majority or lower threshold of limited partners (including a single

limited partner) with equity at risk is able to exercise substantive kick-out rights

(according to their voting interest entity definition) through voting interests over

the general partner(s).

A. For purposes of evaluating the threshold in (01) above, a general partner’s kick-

out rights held through voting interests shall not be included. Kick-out rights

through voting interests held by entities under common control with the general

partner or other parties acting on behalf of the general partner also shall not be

included.

02. Limited partners with equity at risk are able to exercise substantive participating

rights (according to their voting interest entity definition) over the general

partner(s).](https://image.slidesharecdn.com/pwc-consolidation-equity-method-accounting-2015-150930181755-lva1-app6892/85/PwC-Consolidation-Equity-Method-Accounting-2015-132-320.jpg)

![Equity method of accounting

4-44 PwC

□ The excess of the investor’s share of the investee’s net assets over the initial cost

measurement (including contingent consideration otherwise recognized under

ASC 323-10-30-2A).

Subsequent accounting for contingent consideration recognized under this model

requires that, upon resolution of the contingency, the fair value of the consideration

paid should be compared to the initial liability recorded. If the consideration paid

exceeds the liability initially recorded, that amount should be recognized as an

additional cost of the investment. If the consideration paid is less than the liability

initially recorded, then that amount should reduce the cost of the investment.

The accounting for contingent consideration issued in the acquisition of an equity

method investment, as described above, is different from the contingent consideration

model associated with business combinations. See BCG 2 for information on

accounting for contingent consideration in a business combination.

Examples 4-24 and 4-25 illustrate the accounting for contingent consideration

associated with the acquisition of an investment accounted for under the equity

method.

EXAMPLE 4-24

Contingent consideration recognized pursuant to ASC 815

Investor acquired a 20% interest in the voting common stock of Investee for cash

consideration of $100 and a contingent consideration arrangement meeting the

definition of a derivative with a fair value of $10. Investor’s interest in Investee

provides it with the ability to exercise significant influence over the operating and

financial policies of Investee. Therefore, Investor accounts for its investment in

Investee pursuant to the equity method of accounting.

At what amount should Investor’s investment in the common stock of Investee be

measured on the date of acquisition?

Analysis

The contingent consideration arrangement is required to be recognized pursuant to

ASC 815. Therefore, the initial cost of Investor’s investment should be measured at

$110 ($100 [cash consideration] plus $10 [fair value of derivative]). Subsequent

changes in the fair value of the contingent consideration would be accounted for

pursuant to ASC 815 and separate from the equity method investment.

EXAMPLE 4-25

Contingent consideration when the fair value of the Investor’s share of the Investee’s

net assets exceeds the investor’s initial cost

On January 1, 20X0, Investor acquired a 20% interest in the voting common stock of

Investee for cash consideration of $100. On the date of acquisition, the fair value of

Investor’s share of the Investee’s net assets was $120. Investor is required to pay

additional consideration of $25 to Investee if certain performance targets are met.](https://image.slidesharecdn.com/pwc-consolidation-equity-method-accounting-2015-150930181755-lva1-app6892/85/PwC-Consolidation-Equity-Method-Accounting-2015-299-320.jpg)

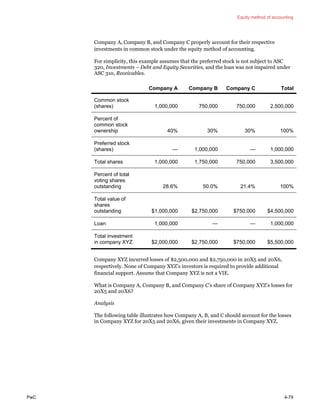

![Equity method of accounting

PwC 4-67

ASC 323-10-55-54

Under this approach, Investor A would recognize equity method losses based on the

change in the investor’s claim on the investee’s book value.

ASC 323-10-55-55

With respect to 20X1, if Investee hypothetically liquidated its assets and liabilities at

book value at December 31, 20X1, it would have $207 available to distribute. Investor

A would receive $120 (Investor A’s 60% share of a priority claim from the loan [$100]

and a priority distribution of its preferred stock investment of $20 [which is 50% of

the $40 remaining to distribute after the creditors are paid]). Investor A’s claim on

Investee’s book value at January 1, 20X1, was $200 (60% × $167 = $100 and 50% ×

$200 = $100). Therefore, during 20X1, Investor A’s claim on Investee’s book value

decreased by $80 and that is the amount Investor A would recognize in 20X1 as its

share of Investee’s losses. Investor A would record the following journal entry.

Equity method loss $80

Preferred stock investment $80

ASC 323-10-55-56

With respect to 20X2, if Investee hypothetically liquidated its assets and liabilities at

book value at December 31, 20X2, it would have $7 available to distribute. Investor A

would receive $4 (Investor A’s 60% share of a priority claim from the loan). Investor

A’s claim on Investee’s book value at December 31, 20X1, was $120 (see the preceding

paragraph). Therefore, during 20X2, Investor A’s claim on Investee’s book value

decreased by $116 and that is the amount Investor A would recognize in 20X2 as its

share of Investee’s losses. Investor A would record the following journal entry.

Equity method loss $116

Preferred stock investment $20

Loan $96

ASC 323-10-55-57

With respect to 20X3, if Investee hypothetically liquidated its assets and liabilities at

book value at December 31, 20X3, it would have $507 available to distribute. Investor

A would receive $256 (Investor A’s 60% share of a priority claim from the loan [$100],

Investor A’s 50% share of a priority distribution from its preferred stock investment

[$100], and 40% of the remaining cash available to distribute [$140 × 40% = $56]).

Investor A’s claim on Investee’s book value at December 31, 20X2, was $4 (see above).

Therefore, during 20X3, Investor A’s claim on Investee’s book value increased by

$252 and that is the amount Investor A would recognize in 20X3 as its share of

Investee’s earnings. Investor A would record the following journal entry.

Loan $ 96

Preferred stock 100

Investment in investee 56

Equity method income $252](https://image.slidesharecdn.com/pwc-consolidation-equity-method-accounting-2015-150930181755-lva1-app6892/85/PwC-Consolidation-Equity-Method-Accounting-2015-322-320.jpg)

![Equity method of accounting

4-78 PwC

Excerpt from ASC 323-10-35-24

[T]he investor shall continue to report its share of equity method losses in its

statement of operations to the extent of and as an adjustment to the adjusted basis of

the other investments in the investee. The order in which those equity method losses

should be applied to the other investments shall follow the seniority of the other

investments (that is, priority in liquidation). For each period, the adjusted basis of the

other investments shall be adjusted for the equity method losses, then the investor

shall apply Subtopics 310-10 and 320-10 to the other investments, as applicable.

When an investor’s investment in common stock has been reduced to zero and it has

other investments in the investee, the investor should generally not recognize equity

method losses against its other investments based solely on its percentage of investee

common stock held. In such instances, there are two acceptable methods that could be

applied. An investor would either recognize investee losses based on (1) the ownership

level of the particular investee security or loan/advance held by the investor to which

the equity method losses are being applied, or (2) the change in the investor’s claim on

the investee book value.

Excerpt from ASC 323-10-35-28

[T]he investor shall not recognize equity method losses based solely on the percentage

of investee common stock held by the investor. Example 5 (see paragraph 323-10-55-

48) illustrates two possible approaches for recognizing equity method losses in such

circumstances.

The following example illustrates one approach that an investor may apply in order to

attribute investee losses to different investments it holds. For another example, see

CG 4.5.1.3 from ASC 323-10-55-48.

EXAMPLE 4-34

Attribution of investee losses when an investor holds other investments

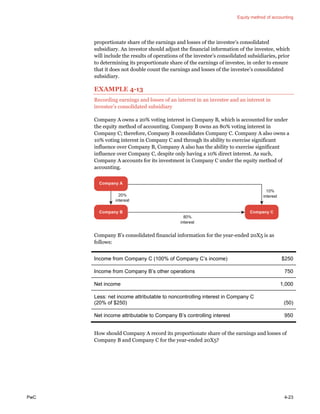

On January 1, 20X5, Company XYZ began its operations with three investors,

Company A, Company B, and Company C.

Company A acquired 1,000,000 shares of Company XYZ’s common stock for $1 per

share and loaned Company XYZ $1,000,000 in cash.

Company B acquired 750,000 shares of Company XYZ’s common stock for $1 per

share and 1,000,000 shares of Series A voting preferred stock (preferred stock) in

Company XYZ for $2 per share. The preferred stock is not considered in-substance

common stock.

Company C acquired 750,000 shares of Company XYZ’s common stock for $1 per

share.](https://image.slidesharecdn.com/pwc-consolidation-equity-method-accounting-2015-150930181755-lva1-app6892/85/PwC-Consolidation-Equity-Method-Accounting-2015-333-320.jpg)

![Equity method of accounting

4-80 PwC

Company A

Common

Stock Loan

Equity investment in Company XYZ - 1/1/20X5 $1,000,000 $1,000,000

Company A’s share of 20X5 net losses

(($2,500,000) x 40%) (1,000,000) —

Equity investment in Company XYZ - 12/31/20X5 (A) — 1,000,000

Company A’s share of 20X6 net losses ($750,000)

[that is, $2,750,000 less $2,000,000 that is first

applied to preferred stock] — (750,000)

Equity investment in Company XYZ - 12/31/20X6 (B) — 250,000

Company B

Common

Stock

Preferred

Stock

Equity investment in Company XYZ - 1/1/20X5 $750,000 $2,000,000

Company B’s share of 20X5 net losses

(($2,500,000) x 30%) (750,000) —

Equity investment in Company XYZ - 12/31/20X5 (A) — 2,000,000

Company B’s share of 2006 net losses [that is,

$2,750,000, of which $2,000,000 is first applied to

preferred stock] — (2,000,000)

Equity investment in Company XYZ - 12/31/20X6 (B) — —

Company C

Common

Stock

Equity investment in Company XYZ - 1/1/20X5 $750,000

Company C’s share of 20X5 of net losses

(750,000)](https://image.slidesharecdn.com/pwc-consolidation-equity-method-accounting-2015-150930181755-lva1-app6892/85/PwC-Consolidation-Equity-Method-Accounting-2015-335-320.jpg)

![Equity method of accounting

PwC 4-103

the original 10-year life determined at acquisition, the remaining asset lives may not

necessarily be 5 years. The estimated remaining lives of Investee’s fixed assets at the

date of impairment would need to be considered in determining the appropriate

amortization period. For purposes of this example, we have assumed 5 years.

Investee’s net income would include $2,000,000 of depreciation expense

($20,000,000 [investee’s carrying value of its fixed assets]/10 years [estimated useful

life]), which reflects the carrying value of the fixed assets as reported in Investee’s

financial statements. Investor would recognize its proportionate share of Investee’s

net income; however, Investor should also amortize $500,000 ($2.5 million/5 years)

of the negative basis difference as an increase (credit) to equity in earnings in order to

reflect Investor’s lower cost basis in Investee’s fixed assets, which results in lower

annual depreciation expense.

4.6.2 Investor accounting for impairments recorded at the investee level

An investor applying the equity method does not need to separately test the investee’s

underlying assets for impairment (or the value it has recorded in its equity method

memo accounts related to those assets). Equity method goodwill is also not required

to be separately assessed for impairment. ASC 350 indicates that the impairment

guidance is not applicable to an investor applying the equity method on the basis that

the investor does not control the business or underlying assets that give rise to the

goodwill.

If the investee recognizes an impairment charge, including for goodwill, then the

investor would generally need to record at least its share of that impairment charge.

An impairment charge at the investee may also impact the investor’s basis differences

in those impaired assets.

As illustrated in Example 4-39, the investor and investee often apply different

impairment models and at a different unit of account − impairment is tested at the

investment level under the equity method versus at a lower level by the investee.

Therefore, an impairment charge may need to be recorded at the investor level where

no impairment exists at the investee level, or an impairment charge may need to be

recorded at the investee level but not at the investor level.

4.7 Accounting for changes in interest

4.7.1 Overview of changes in interest

An investor would continue to apply the equity method until its ownership interest is

reduced or other changes are made such that the investor is no longer able to exert

significant influence over the investee, or in the event that the investor gains a

controlling financial interest over the investee. The reassessment of whether an

investor has significant influence over the investee is an ongoing evaluation.

A change in ownership interest could cause an investment to either qualify for the

equity method of accounting for the first time, continue to be accounted for as an](https://image.slidesharecdn.com/pwc-consolidation-equity-method-accounting-2015-150930181755-lva1-app6892/85/PwC-Consolidation-Equity-Method-Accounting-2015-358-320.jpg)

![Equity method of accounting

PwC 4-115

EXAMPLE 4-41

Investor is net purchaser due to investee transaction

Investor owns 40 common shares in Investee representing a 40% ownership interest

(a total of 100 shares are outstanding). The carrying value of the investment on

Investor’s books is $10 per share, which is also Investee’s book value per share (i.e., no

basis differences exist). Investee subsequently purchases 25 shares from third parties

at $12 per share in a treasury stock transaction. The price exceeds Investee’s book

value per share of $10.

As a result of this transaction, Investor’s ownership interest in Investee has increased

from 40% to 53.3% (or 40 shares/75 shares). Investor, in not selling any of its

ownership interest has, in substance, purchased an additional interest in Investee.

Assume Investor does not obtain control of Investee.

What entries should Investor and Investee record?

Analysis

Investor would record $27 in its equity method memo accounts, the difference

between its investment carrying amount of $400 and its underlying equity in

Investee’s net assets of $373 (53.3% x $700 [Investee’s initial net assets of $1,000,

less the $300 paid by Investee to purchase 25 shares from third parties at $12 per

share]) arising from Investor not participating in Investee’s treasury stock transaction

and, therefore, not maintaining its proportionate interest in Investee. This could also

be illustrated as follows:

Decrease in book value attributable to the repurchase of

shares from third parties ($2 per share X 25 shares) $50

Investor’s share after the transaction 53.3%

Investor’s loss of equity in Investee’s net assets $27

Investor’s loss of equity of $27 due to the change of interest should be allocated to

assets and liabilities with the excess being recorded as goodwill.

The accounting entries for this example are illustrated as follows:](https://image.slidesharecdn.com/pwc-consolidation-equity-method-accounting-2015-150930181755-lva1-app6892/85/PwC-Consolidation-Equity-Method-Accounting-2015-370-320.jpg)

The document is a comprehensive guide by PwC on consolidation and the equity method of accounting, providing detailed information on accounting standards relevant to investments, partnerships, and joint ventures. It covers the frameworks for consolidation, specific accounting methods, and includes a variety of illustrative examples and questions to clarify these principles. The guide serves as a resource for financial statement preparers, emphasizing the importance of professional advice and referencing authoritative literature.