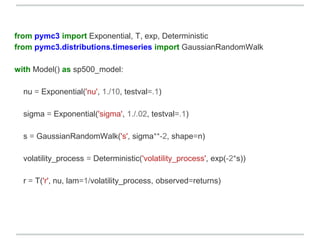

Downloaded 76 times

![with disaster_model:

trace = sample(10000, step=[Metropolis(), NUTS()])

traceplot(trace, ['early_mean', 'late_mean', 'switchpoint'])](https://image.slidesharecdn.com/probabilisticprogramminginpythonwithpymc3-150806165133-lva1-app6891/85/Probabilistic-programming-in-python-with-PyMC3-John-Salvatier-11-320.jpg)

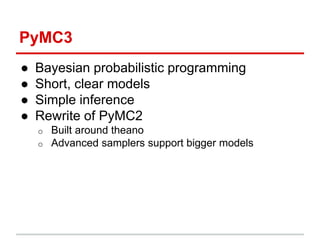

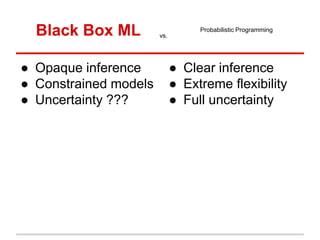

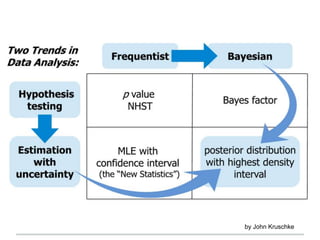

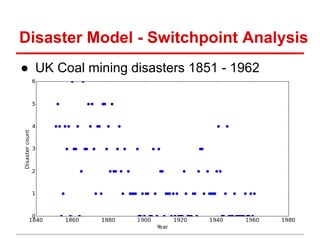

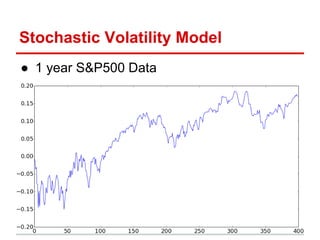

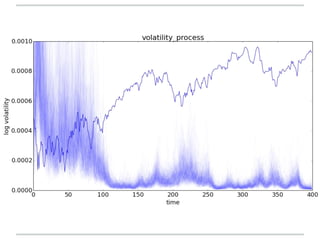

This document summarizes probabilistic programming in Python using PyMC3. PyMC3 allows users to write probabilistic models and automatically perform Bayesian inference to estimate unknown parameters. It features a simple and clear syntax for model specification, supports advanced sampling methods for large models, and can handle tasks like time series analysis, generalized linear models, and more. The document provides examples of disaster and stock volatility models in PyMC3 and directs readers to additional resources.

![[261] 실시간 추천엔진 머신한대에 구겨넣기](https://cdn.slidesharecdn.com/ss_thumbnails/216-150915054828-lva1-app6891-thumbnail.jpg?width=640&height=640&fit=bounds)

![[기초개념] Recurrent Neural Network (RNN) 소개](https://cdn.slidesharecdn.com/ss_thumbnails/agistpurnndkim190430-190430140949-thumbnail.jpg?width=640&height=640&fit=bounds)

![[P.D.F] Bayesian Methods for Hackers: Probabilistic Programming and Bayesian ...](https://cdn.slidesharecdn.com/ss_thumbnails/bayesian-methods-for-hackers-probabilistic-programming-and-bayesian-inference-191119012050-thumbnail.jpg?width=640&height=640&fit=bounds)