Downloaded 10 times

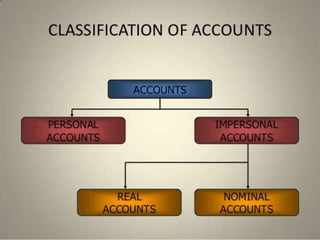

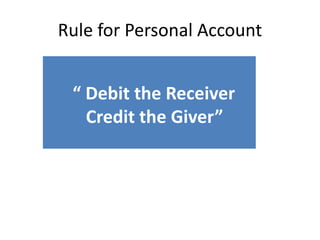

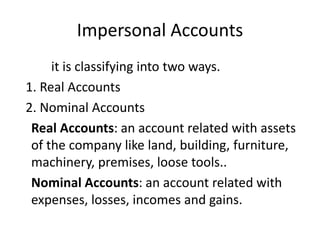

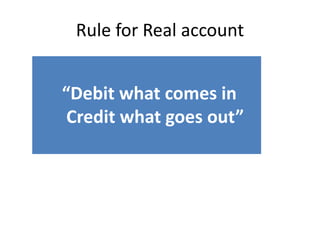

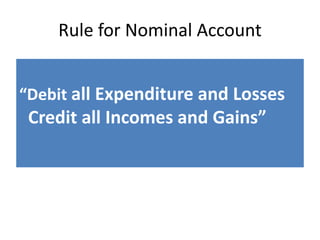

This document discusses accounting principles and rules. It describes different types of accounts including personal accounts (natural, artificial), real accounts, and nominal accounts. It provides rules for each type of account: debit the receiver and credit the giver for personal accounts, debit what comes in and credit what goes out for real accounts, and debit expenditures/losses and credit incomes/gains for nominal accounts. The document concludes that the first step to recording financial transactions is creating a chart of accounts to classify transactions.