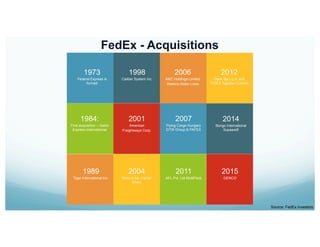

The document provides an overview of the courier industry and FedEx's position within it. It begins with a brief history of the industry from the 1700s to present day. It then discusses the current state, noting tight competition between major players like UPS and FedEx, the impact of e-commerce growth, and trends in different geographic segments. The document concludes by focusing on FedEx specifically, highlighting its priorities around financial returns, customer service, and business relationships.