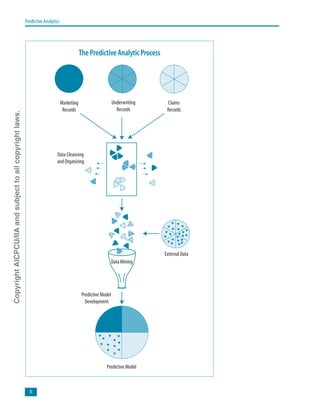

This document provides an overview of predictive analytics and its growing use in the insurance industry. Predictive analytics uses statistical techniques and data mining to develop models that predict future events or behaviors. Insurers are increasingly using predictive analytics in marketing, underwriting, and claims functions. Key drivers of its adoption include technological advances enabling complex analytics, greater data availability, insurers' desire for growth in slow markets, and seeking competitive advantages. The document discusses various predictive analytic applications and their potential benefits for insurers.