流程:线性 流程 : 圆周式 Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text

5.

影响因素: 互动 /相互制约: Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Goal Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text

6.

整体 / 部分:Text Text Text Text Text Label A Label B 原因 - 结果: Text Text Text Text Text Text Text Text Text Text Text Text Text Text

7.

矛盾: 障碍 /阻力: Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text Text

Understanding buyer valueshelps prove or disprove current hypotheses as well as generate strategy solutions. Approach Identify Buyer Value Segments Situation Assessment Hypothesis List Development Survey Collection Data Coding and Utility Calculation Instrument Design and Testing Sample Quota Design and List Pull Data Analysis Market Research & Visioning Conceptual Design Detailed Design & Pilot Implementation (phased) Systems Development/ Enhancement Field Administration Preparation

32.

Organizational beliefs andstrategy alternatives identified in the situation assessment are translated into hypotheses for testing. Hypothesis Development Situation Assessment Hypothesis List Development Survey Collection Data Coding and Utility Calculation Instrument Design and Testing Field Administration Preparation Sample Quota Design and List Pull Data Analysis

33.

Identifying Buyer Value-Basedsegments creates the foundation for creating the distribution channel strategy and design. Summary — Identify Buyer Value Segments Identify Buyer Value Segments What do consumers value? How can we segment consumers based on these values? Develop Conceptual Strategy Design Based on what consumers value, what is our strategic direction? Conceptually, what types of products do we want to offer? Conceptually, what channels do we want consumers to use? Develop Migration Strategy How do we communicate these changes to our key stakeholders? How do we prepare our consumers and employees for these changes? How do we actually get to where we want to be? Pilot Plan Roll-Out Plan Estimate Anticipated Customer Behavior To which channels will customers migrate? Develop Product/Pricing Strategy What products should we offer? How should they be priced? Determine Distribution Network How do we change our branch and ATM networks? How many? Where should they be located? Minimize Business Decision Risk How will consumers react? How will this affect our bottom line? Develop Data Mining Opportunities How do we exploit buyer value insights to better target market segments? iterative Plan Implementation Develop Detailed Strategy Design Develop Conceptual Strategy Design Understand Value Propositions Customer Migration Strategy

34.

Value based segmentstrategies can produce incremental revenues of $700 million and reduce costs up to $150 million. Benefits — Quantitative Identify Buyer Value Segments - Quantifiable Benefits - These cost savings will be offset by the $52 million increase in central delivery unit costs... By 1999, even after absorbing significant implementation/infrastructure costs, project can contribute over $700 million pre-tax annually . . . $493 $670 $309 The shareholder value effect can be significant. Year Branch and City Administration annual operating costs will be reduced by nearly $200 million . . . $MM ILLUSTRATIVE

35.

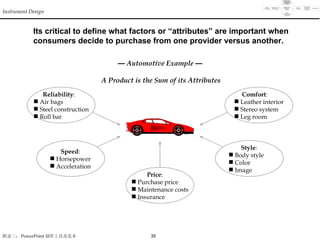

Its critical todefine what factors or “attributes” are important when consumers decide to purchase from one provider versus another. — Automotive Example — A Product is the Sum of its Attributes Instrument Design Reliability : Air bags Steel construction Roll bar Speed : Horsepower Acceleration Price : Purchase price Maintenance costs Insurance Style : Body style Color Image Comfort : Leather interior Stereo system Leg room

36.

With traditional research,when you ask how important any particular feature is individually, consumers tend to say each is very important. 1 2 3 4 5 6 7 8 9 10 Styling Price Speed Reliability Not at all important Very important Instrument Design

These groups orsegments of consumers not only have different profit potentials... — Investment Buyer Value Segments — % of Market (Consumers) — Investment Buyer Value Segments — % of Market ($) — Average Investment Balance Per Value Segment — Source: Andersen Consulting National Buyer Values Study for Retail Financial Services Consumers Value Segment Channel Rate / Speed Liquidity / Access Sensitive Speed Avg.. Investment Balance $77,725 $92,264 $96,335 $68,212 Case Study Channelists Speed Liquidity / Access Sensitive 34% Rate / Speed Sensitive 16% Speed Liquidity / Access Channel Rate / Speed

39.

In summary, usingvalue based segmentation is a powerful tool to improve a client’s bottom line. $ Creates Revenue Opportunities Retain most profitable customers Improve profitability of other customers by fulfilling their values with lower cost structures Generate new business Identify revenue enhancement opportunities Simplify and increase effectiveness of client ’ s target market activities Identifies Substantial Cost Reduction Better manage utilization of client ’ s delivery network Focus on delivery on required service thresholds Strip costs from non-value added processes Don ’ t have to build one delivery option that fits all Better Positions Relative to Client ’ s Competition Increased customer satisfaction due to fulfilled value sets Organization clearly understands goals and delivery expectations Sets stage for adaptable organization better able to respond to competitive change

40.

Based on AndersenConsulting’s investigation of the target markets, there is identifiable change in buyer preferences from window to split and cabinet air conditioners. -- Product -- Yesterday Today Future trends Window and split account for the majority of the air conditioners possession before 1996. Split air conditioners account for the majority of sales. Cabinets sales begin to increase and windows share of the market begin to decline (From distributors perspective) Cabinet air conditioners will continue to grow cabinet air conditioners show strong growth due to increasing size of homes and price cuts. Future sales growth will continue with improvements in residential power Some customer segments (especially rural) regard air conditioners as a type of high-end furniture (whose secondary purpose is to cool). Cabinets, best meet this type of customer’s buyer value and will grow with this segment. Split will remain stable, and even decline in some areas Splits will keep the same market share Compared to the cabinets, it will decline slightly in some areas because of installation difficulties Generally, window air conditioners will decrease dramatically, but still account for a certain proportion acting as a transition product for price conscious buyers in hot areas Because of this income limitation, window air conditioners will still account for a large proportion of sales in economically developing markets (i.e. Changsha and Chongqing) Windows will continue to sell well in markets such as Hangzhou as transition products for people who are waiting to move into new housing Growth in Mini Central and Ceiling air conditioners Mini-central or residential used ceiling ones will gain in popularity amongst people in large apartments and houses (especially as market awareness of product availability grows). Breakdown of different types of air conditioners (Before 1996) Current purchase preferences (1996-1998) Window 48% Split 48% Cabinet 9% Window 26% Split 53% Cabinet 21% Market Overview

41.

Competition Today LocalChinese manufacturers upgrade production technology to offer quality levels on par with JV operations Local Chinese manufacturers develop marketing capability/expertise JV operations, crippled by ability to understand market and operate within local business culture’s drop in position JVs begin to compete more on price as perception of added value differentiation disappears. Over the last three to four years, local air conditioner manufacturers have been able to reposition themselves successfully through combined advances in quality and marketing… Perceived Added Value Price Low Low High High Low Low High High Meidi Kelon Chunlan Gree Perceived Added Value Price National Mitsubishi Sharp Hitachi Chunlan Gree National Mitsubishi Hitachi -- Yesterday -- -- Today -- Competition Yesterday Local and JV manufacturers target two different market segments separated by price/quality trade off JV operations target quality conscious upper end of market while local manufacturers target bottom end Local manufacturers limited in terms of production quality capability and marketing experience Market Overview

42.

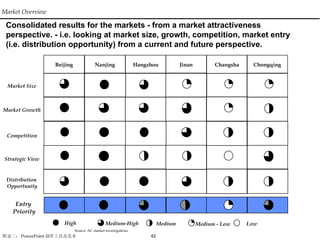

Consolidated results forthe markets - from a market attractiveness perspective. - i.e. looking at market size, growth, competition, market entry (i.e. distribution opportunity) from a current and future perspective. Entry Priority High Medium-High Medium Medium - Low Low Market Size Strategic View Distribution Opportunity Competition Market Growth Market Overview Source: AC market investigations Beijing Nanjing Hangzhou Jinan Changsha Chongqing

43.

From the salesoffices and warehouses established in these several markets, strategic nodes can be established to allow access to nearby markets. Market Overview Source: AC market investigations High Priority Medium to High Priority Medium Priority Medium to Low Priority Cities to be covered Cities Requiring Investigation Year One Beyond Year One Beijing Jinan Nanjing Shanghai Hangzhou Changsha Shenzhen Chongqing Tianjin ShijiaZhuang (Hebei) Zhengzhou (Henan) Qingdao Hefei (Anhui) Suzhou Chengdu Shantou Xiamen Wuhan Xi’an (Shaanxi) Zhanjiang Guiyang Kunming