Download as PDF, PPTX

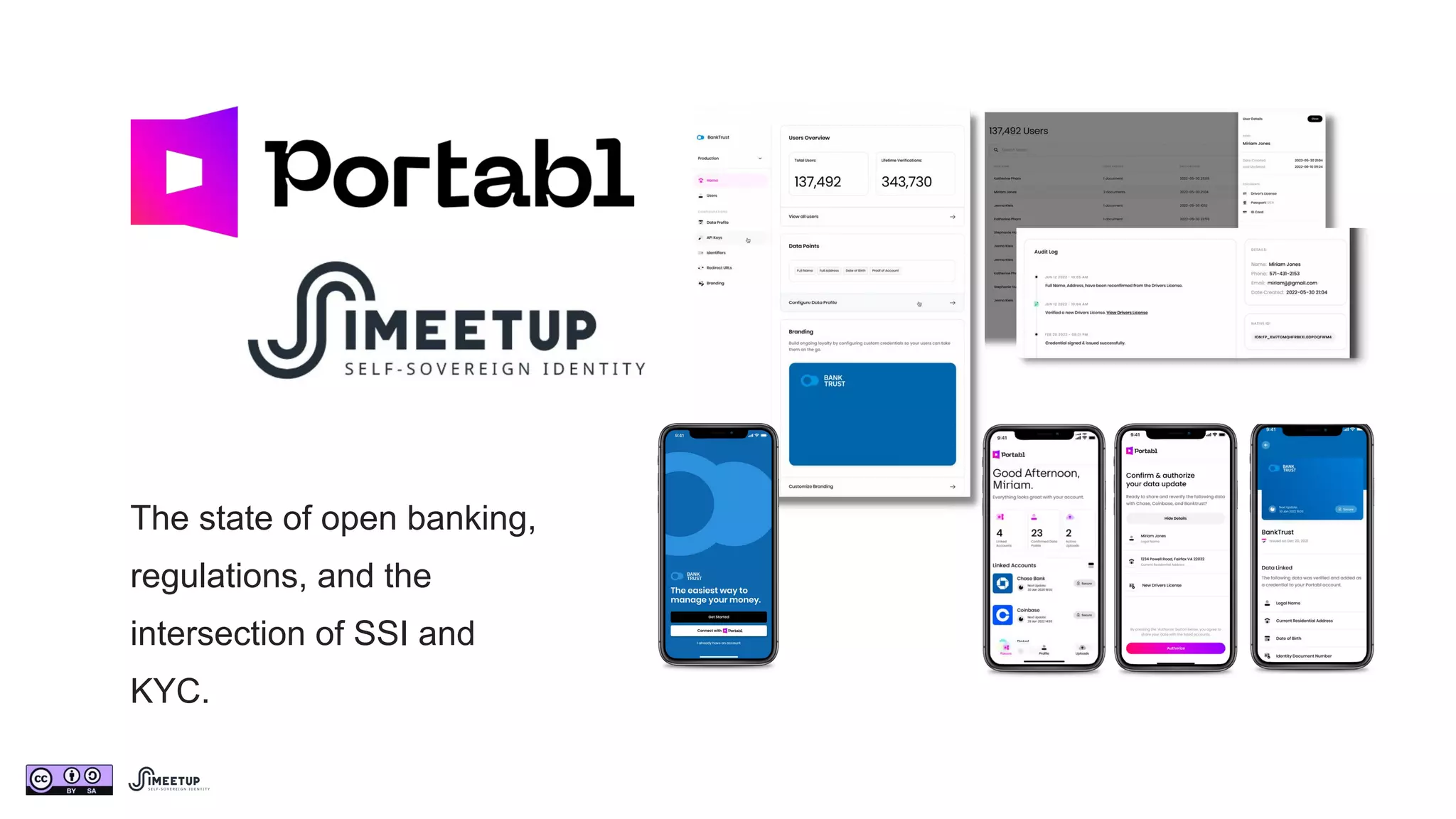

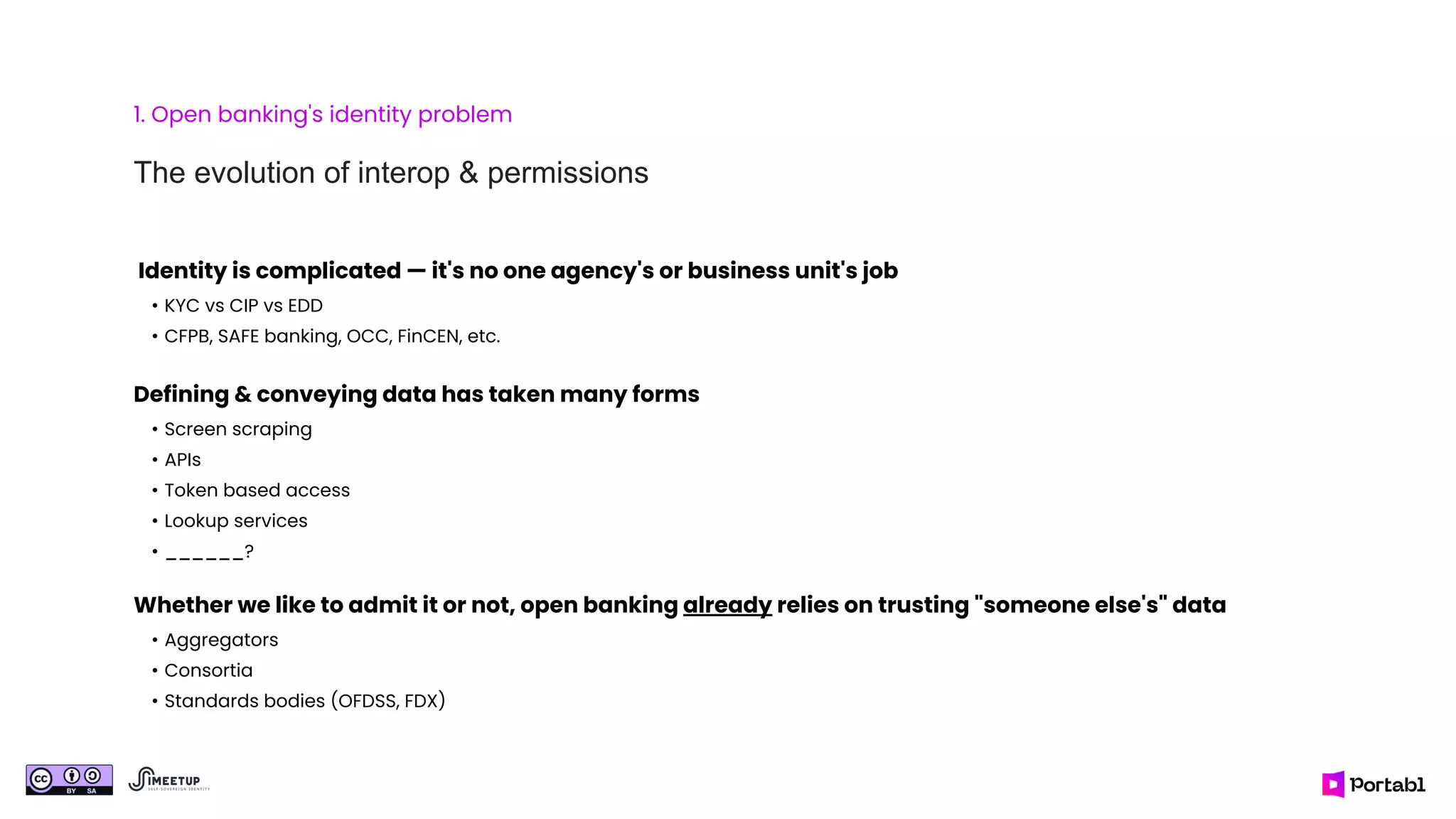

The document discusses the state of open banking, emphasizing the integration of self-sovereign identity (SSI) and know your customer (KYC) regulations. It highlights the challenges of trust, security, and user control in financial identity management, advocating for a user-first approach that simplifies access and enhances overall lifecycle standards. The vision includes creating a universal financial identity that enables reusable credentials while addressing compliance, privacy, and fraud concerns.

![[WSO2 Open Banking & Security Forum Mexico 2019] Walking the Tightrope: Balan...](https://cdn.slidesharecdn.com/ss_thumbnails/wso2openbankingsecurityforummexico2019-walkingthetightrope-190528051555-thumbnail.jpg?width=640&height=640&fit=bounds)