Downloaded 26 times

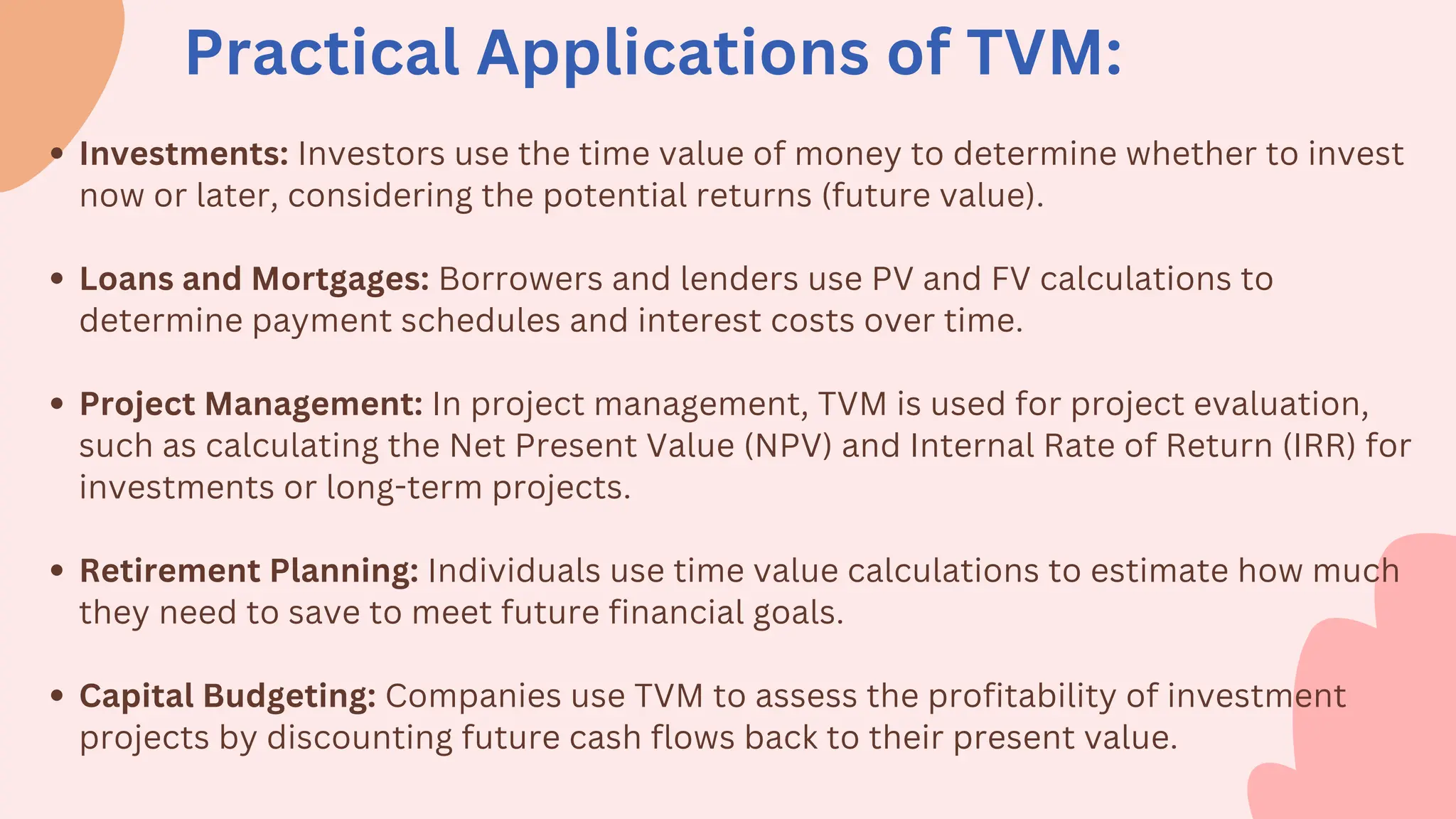

The time value of money (TVM) is a crucial financial concept that demonstrates how the value of money changes over time due to its potential earning capacity. It emphasizes that money today is worth more than the same amount in the future because of factors like interest rates, inflation, and investment opportunities. TVM concepts are applied in various fields, including investments, loans, project management, and retirement planning to evaluate financial decisions and forecast future values.