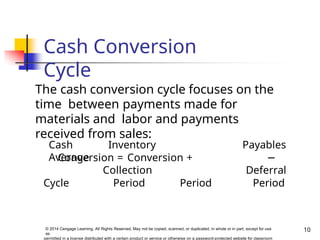

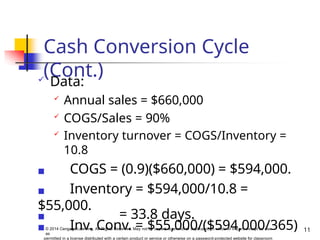

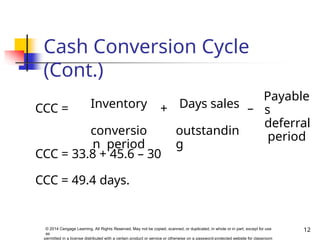

The document discusses working capital management, focusing on cash, inventory, and accounts receivable management, as well as their implications for a firm's financial health. It highlights the importance of effective cash management, the analysis of cash conversion cycles, and the evaluation of working capital policies in relation to industry standards. Additionally, it emphasizes the need for a balanced credit policy to optimize cash inflows and minimize risk while maintaining customer relationships.