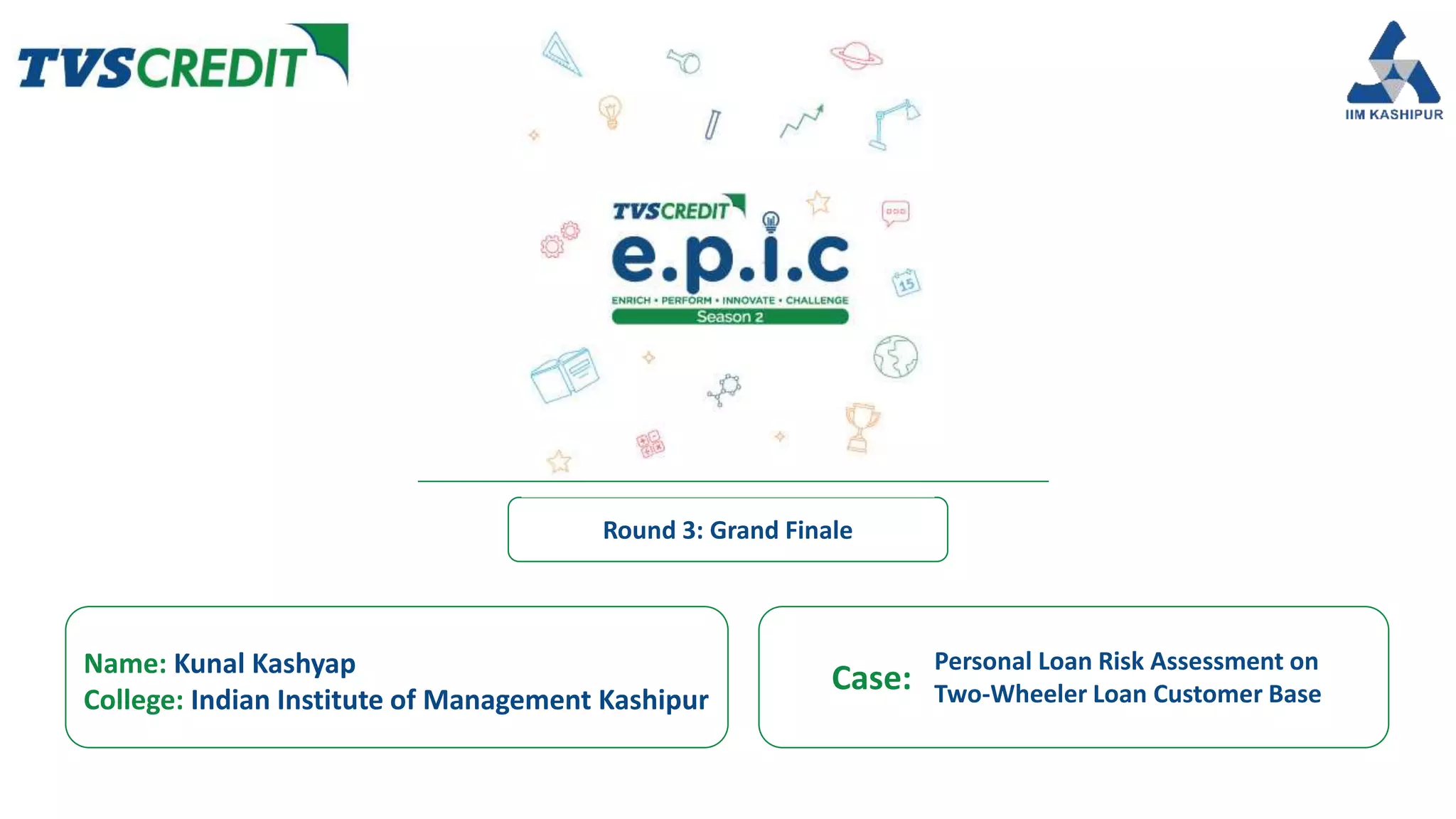

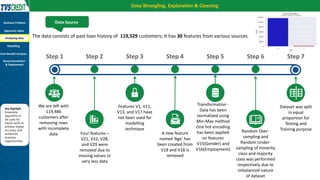

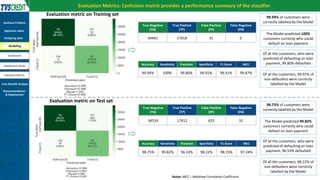

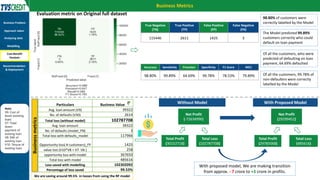

The document presents a case study by Kunal Kashyap focusing on risk assessment for personal loans using a two-wheeler loan customer base at IIM Kashipur. The objectives include identifying customers likely to default and developing a predictive model to manage loan offerings effectively. The study employs a Random Forest classification model, achieving 99.94% accuracy on training data and highlighting significant parameters for classification, ultimately demonstrating substantial savings in potential losses through model implementation.

![ai it hw mst prac[1] - Read-Offnly.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/aiithwmstprac1-read-only-250118093323-c97d352c-thumbnail.jpg?width=640&height=640&fit=bounds)