Personal Loan at Attractive Interest Rates by HDFC Bank

•

1 like•224 views

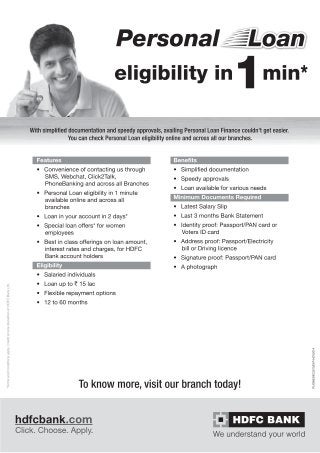

Apply for personal loan at HDFC Bank for all your personal financing needs and enjoy super fast application processing and disbursal at attractive interest rates. Apply online for instant personal loan with HDFC.

Report

Share

Report

Share

Download to read offline

Recommended

Idbi home loan

IDBI Bank provides home loans with flexible options to suit customers' needs. It offers loans for up to 90% of a property's value, with maximum tenures of 30 years for salaried individuals. Eligibility includes being aged 22-70 and having proper income documents. The home loan interest rate is transparent and set according to RBI guidelines, currently around 10.4%. IDBI maintains a home loan calculator to provide estimates of costs and EMIs upfront and remove ambiguities. Its home loans have become popular for their customized nature and transparent dealings.

Bank deposits, nominations and deposit insurance

Deposits are a key source of low-cost funds for banks and are profitable as banks can lend these funds and earn a higher return. There are various types of deposits including demand deposits like savings and current accounts, term deposits for fixed periods, and non-resident accounts for NRIs. Banks offer benefits to customers like a safe place to park funds, earning interest, and payment/withdrawal abilities. Joint accounts and nominations are also discussed.

Ch 4 DEPOSITS IN COMMERCIAL BANKS

Bank deposits provide a key source of low-cost funds for banks and come in several types:

Demand deposits like savings accounts that allow withdrawals on demand and earn interest; term deposits for fixed periods that pay higher interest but may charge penalties for early withdrawal; and hybrid/flexi deposits that automatically shift surplus funds into term deposits. Deposits serve various purposes for account holders and banks aim to lend deposits at higher returns to earn a profit. Accounts also exist for non-residents in foreign currencies or rupees.

IDBI

IDBI Bank is one of India's largest public sector banks that was established in 1964. It provides various banking services like deposits, loans, payments, investments and cards to personal and corporate customers. IDBI Bank has over 991 branches across India and overseas with subsidiaries in areas like capital markets, home finance, and investments. The bank offers a wide range of products for retail, SME, corporate and agricultural customers.

IDBI ppt

This document provides an overview of IDBI Bank and discusses its history, business strengths, and strategic priorities. IDBI Bank was established in 1964 as India's apex development financial institution and played a critical role in the country's industrial and economic progress. It has since transitioned to a universal bank while maintaining its leadership in corporate and infrastructure lending. The bank has a strong technology platform, high operational efficiencies, and aims to expand its retail footprint and global presence while upholding high standards of governance and social responsibility.

Deposit schemes

This document contains guidelines from the Reserve Bank of India (RBI) regarding know-your-customer (KYC) procedures and monitoring of cash transactions for banks in India. It outlines requirements for banks to establish customer identity and monitor suspicious transactions. Key points include obtaining proper identification for new accounts, completing KYC procedures for existing accounts, issuing demand drafts and money transfers over Rs. 50,000 only by debit to accounts, monitoring cash withdrawals and deposits over Rs. 10 lakhs, and reporting such cash transactions and suspicious activity to controlling offices. The guidelines aim to prevent money laundering and terrorist financing through strict KYC norms and monitoring of large cash transactions.

Industrial development bank of india

IDBI Bank is an Indian state-owned banking and financial services company headquartered in Mumbai, India. It was established in 1964 as the Industrial Development Bank of India to provide credit and other financial facilities for the establishment and development of industries in India. Over the years, IDBI has expanded its operations to include various banking services such as consumer banking, corporate banking, investment banking, private banking, wealth management and more. As of 2021, IDBI Bank has over 15435 employees and total assets of Rs. 2650 billion.

State bank of india

State Bank of India (SBI) is India's largest bank. It was formed in 1955 by the government merging the Imperial Bank of India with various state-associated banks. SBI has over 21,500 branches across India and 172 offices in foreign countries. It has various subsidiaries and associate banks within India. SBI continues to be a pioneer in the Indian banking sector and aims to further financial inclusion through its services.

Recommended

Idbi home loan

IDBI Bank provides home loans with flexible options to suit customers' needs. It offers loans for up to 90% of a property's value, with maximum tenures of 30 years for salaried individuals. Eligibility includes being aged 22-70 and having proper income documents. The home loan interest rate is transparent and set according to RBI guidelines, currently around 10.4%. IDBI maintains a home loan calculator to provide estimates of costs and EMIs upfront and remove ambiguities. Its home loans have become popular for their customized nature and transparent dealings.

Bank deposits, nominations and deposit insurance

Deposits are a key source of low-cost funds for banks and are profitable as banks can lend these funds and earn a higher return. There are various types of deposits including demand deposits like savings and current accounts, term deposits for fixed periods, and non-resident accounts for NRIs. Banks offer benefits to customers like a safe place to park funds, earning interest, and payment/withdrawal abilities. Joint accounts and nominations are also discussed.

Ch 4 DEPOSITS IN COMMERCIAL BANKS

Bank deposits provide a key source of low-cost funds for banks and come in several types:

Demand deposits like savings accounts that allow withdrawals on demand and earn interest; term deposits for fixed periods that pay higher interest but may charge penalties for early withdrawal; and hybrid/flexi deposits that automatically shift surplus funds into term deposits. Deposits serve various purposes for account holders and banks aim to lend deposits at higher returns to earn a profit. Accounts also exist for non-residents in foreign currencies or rupees.

IDBI

IDBI Bank is one of India's largest public sector banks that was established in 1964. It provides various banking services like deposits, loans, payments, investments and cards to personal and corporate customers. IDBI Bank has over 991 branches across India and overseas with subsidiaries in areas like capital markets, home finance, and investments. The bank offers a wide range of products for retail, SME, corporate and agricultural customers.

IDBI ppt

This document provides an overview of IDBI Bank and discusses its history, business strengths, and strategic priorities. IDBI Bank was established in 1964 as India's apex development financial institution and played a critical role in the country's industrial and economic progress. It has since transitioned to a universal bank while maintaining its leadership in corporate and infrastructure lending. The bank has a strong technology platform, high operational efficiencies, and aims to expand its retail footprint and global presence while upholding high standards of governance and social responsibility.

Deposit schemes

This document contains guidelines from the Reserve Bank of India (RBI) regarding know-your-customer (KYC) procedures and monitoring of cash transactions for banks in India. It outlines requirements for banks to establish customer identity and monitor suspicious transactions. Key points include obtaining proper identification for new accounts, completing KYC procedures for existing accounts, issuing demand drafts and money transfers over Rs. 50,000 only by debit to accounts, monitoring cash withdrawals and deposits over Rs. 10 lakhs, and reporting such cash transactions and suspicious activity to controlling offices. The guidelines aim to prevent money laundering and terrorist financing through strict KYC norms and monitoring of large cash transactions.

Industrial development bank of india

IDBI Bank is an Indian state-owned banking and financial services company headquartered in Mumbai, India. It was established in 1964 as the Industrial Development Bank of India to provide credit and other financial facilities for the establishment and development of industries in India. Over the years, IDBI has expanded its operations to include various banking services such as consumer banking, corporate banking, investment banking, private banking, wealth management and more. As of 2021, IDBI Bank has over 15435 employees and total assets of Rs. 2650 billion.

State bank of india

State Bank of India (SBI) is India's largest bank. It was formed in 1955 by the government merging the Imperial Bank of India with various state-associated banks. SBI has over 21,500 branches across India and 172 offices in foreign countries. It has various subsidiaries and associate banks within India. SBI continues to be a pioneer in the Indian banking sector and aims to further financial inclusion through its services.

Types Of Deposit Account

The document discusses various types of bank deposit accounts and services, and poses problems related to banking transactions.

1. A customer lost a fixed deposit receipt and approaches the bank manager for assistance in redeeming the deposit.

2. A joint fixed deposit was issued to X and Y, and now X wants to redeem after one year or take a loan using the deposit as collateral.

3. A joint current account was held by Ram and Raj payable to either survivor, and now the bank must determine how to handle a cheque presented for payment after Raj's death.

Non banking financial institutions

The document summarizes key aspects of non-banking financial institutions (NBFIs) and non-banking financial companies (NBFCs) in India based on the Economic Survey of 2009-10. It discusses the role of NBFIs in providing medium-to-long term financing. It also describes various types of financial institutions and how NBFCs were impacted by the financial crisis. The RBI provided liquidity support to NBFCs through measures like a special repo window. Regulations for NBFCs were also strengthened regarding capital adequacy ratios and other requirements.

IDBI

IDBI was established in 1964 as a wholly-owned subsidiary of RBI to provide long-term financing to industry and agriculture. In 1976, ownership was transferred to the Government of India. IDBI has set up important financial institutions like NSE. It continues to raise capital through bonds and shares to fund its developmental activities. However, moving more into commercial banking has led to high NPAs and difficulty maintaining low funding costs.

Bank deposits

This document discusses bank deposits, including the types of deposits, factors that affect deposits, and measures to increase deposits. It also covers pricing deposits, "Know Your Customer" guidelines for opening accounts, deposit insurance, and non-deposit sources of funds for banks.

Deposits

Savings bank deposits are meant for small savers and have restrictions on withdrawals and minimum balance requirements. Current deposits are for business people and allow withdrawals by cheque but no interest. Recurring deposits encourage regular monthly savings over a fixed period by automatically depositing a set amount each month to earn interest. Fixed deposits are repaid after a specific time period but penalties apply for early closure. Proper documentation and verification is required to open any type of bank deposit.

HDFC Bank

HDFC Bank was established in 1994 as a private sector bank. It has grown to become one of the largest banks in India with over 2,000 branches and 5,000 ATMs across the country. The bank offers a wide range of products and services including credit cards, personal loans, home loans, mutual funds, and trade services. It has pursued an aggressive expansion strategy and targets both retail and corporate customers. The bank has received several awards recognizing its strong financial performance and use of technology.

non banking financial institution

This document discusses non-banking financial institutions (NBFIs) in India. It defines NBFIs as financial institutions that provide banking services without a full banking license. It outlines key differences between NBFIs and banks, importance of NBFIs, functions of NBFIs like mobilizing savings and channeling funds, types of NBFIs including insurance companies and mutual funds, regulations NBFIs must follow, guidelines on fair practices, and top performing NBFIs in India like HDFC and Bajaj Finance.

HDFC PPT

HDFC Bank was incorporated in 1994 and is headquartered in Mumbai, India. It is a major private sector bank that offers various banking products and services including loans, credit cards, savings accounts, investments, and insurance. HDFC Bank has expanded rapidly over the years through mergers and acquisitions as well as organically by opening new branches across India. It aims to continue growing its market share and delivering high quality customer service through product innovation and disciplined risk management practices.

HDFC Persentation

This document provides information about HDFC Bank, one of the major players in the Indian banking sector. It discusses HDFC Bank's history and founding in 1977, its profile including services offered such as loans, credit cards, savings accounts, and insurance. The document also outlines HDFC Bank's network of over 2,000 branches and 6,520 ATMs across India, its board of directors, and performs a basic SWOT analysis.

Sbi PPT

This document provides an analysis of opportunity for promotional strategies for State Bank of India. It begins with an overview of SBI as the largest nationalized commercial bank in India. It then defines various banking services including investment banking, retail banking, commercial banking, private banking, and asset management. It identifies SBI's target markets as current and potential customers in rural areas and tier 2/3 cities. The document outlines SBI's communication objectives of increasing awareness, attention, and purchase actions. It notes factors that affect the communication budget such as company strategy, product life cycle stage, and competitive intensity. Finally, it recommends creating communications strategies that match SBI's strategy and focus on opportunities/threats while fitting the company image, and

State Bank Of India

State Bank of India (SBI) is India's largest bank and traces its origins back to 1806. It has focused on reducing staff, computerizing operations, and improving staff attitudes through training programs like "Parivartan". SBI has a centralized organizational structure but some decentralization in loan approvals. It provides training through the State Bank Academy and has implemented new technology like SAP to respond faster to customers and enable innovation.

17689260 summer-project-on-sbi

State Bank of India (SBI) is India's largest bank with over 200 years of history. It has a large network of over 14,000 branches across India and 73 overseas offices. SBI offers a wide range of corporate, commercial, and retail banking services. Some key points about SBI include its large size and market share in India, acquisition of banks in other countries, and recognition as one of the oldest and most established banks in India. The document provides an overview of SBI's history, operations, management, products, and awards.

Financial institutions

The document provides an overview of financial institutions in India, including their definition, functions, classifications, and examples. It discusses regulatory institutions like RBI and SEBI, as well as intermediaries like IFCI, ICICI, IDBI, LIC, SIDBI, state financial corporations, and specialized institutions like EXIM Bank. It describes the roles of these institutions, the types of assistance they provide like loans and guarantees, and the process of project appraisal.

IDBI

The document provides an overview of IDBI Bank including:

- IDBI Bank was established in 1964 and was originally fully owned by the government but has since seen decreasing government ownership and an increase in private ownership.

- It has a large network of over 900 branches across India and provides various corporate and retail banking services.

- Some key investments and subsidiaries of IDBI Bank that have helped develop India's financial system are listed.

Introduction to idbi bank

Industrial Development Bank of India (IDBI) was established in 1964 to provide long-term financing to industries. It has since diversified into providing various banking services. IDBI provides loans, deposits, investment services to individuals and businesses. It has over 8,000 employees and 689 branches across India. IDBI plays an important role in the development of industries and financial markets in India by establishing institutions like the National Stock Exchange.

loans and advances in iob

Indian Overseas Bank provides various types of loans and advances to customers. These include secured loans like term loans which are granted against assets and can be paid back over longer periods. They also offer unsecured loans like demand loans which are repayable on demand. The bank aims to meet business needs through flexible financing options like cash credits while ensuring safety of funds through security and assessing borrower creditworthiness. A study of IOB's Ashoknagar branch found that term loans contribute significantly to advances and customers appreciate the bank's service, suggesting they focus on faster loan processing and financial education.

Project on SBI

Project on SBI -

I would like to acknowledge a deep sense of gratitude to Mr. Hitesh Rawat, Senior Manager of State Bank of India at Kalbadevi Road, Mumbai for giving me the opportunity & time to work on this project and given me all vital input which has led to completion of this project. Without their guidance this project would have remained in pipe dream.

I am also thankful to State Bank of India employees, who directly & indirectly extended their co-operation and invaluable support to me

Hdfc Bank

HDFC Bank is one of the major private sector banks in India. It was established in 1994 and is headquartered in Mumbai. The bank has over 5,000 branches and ATMs across India that serve corporate and retail customers. HDFC Bank aims to be a world-class bank through high quality customer service, innovative products, and leveraging new technologies. It has experienced significant growth and received several awards for its performance and services.

Independent Study - College of Wooster Research (2023-2024) FDI, Culture, Glo...

Independent Study - College of Wooster Research (2023-2024) FDI, Culture, Glo...AntoniaOwensDetwiler

"Does Foreign Direct Investment Negatively Affect Preservation of Culture in the Global South? Case Studies in Thailand and Cambodia."

Do elements of globalization, such as Foreign Direct Investment (FDI), negatively affect the ability of countries in the Global South to preserve their culture? This research aims to answer this question by employing a cross-sectional comparative case study analysis utilizing methods of difference. Thailand and Cambodia are compared as they are in the same region and have a similar culture. The metric of difference between Thailand and Cambodia is their ability to preserve their culture. This ability is operationalized by their respective attitudes towards FDI; Thailand imposes stringent regulations and limitations on FDI while Cambodia does not hesitate to accept most FDI and imposes fewer limitations. The evidence from this study suggests that FDI from globally influential countries with high gross domestic products (GDPs) (e.g. China, U.S.) challenges the ability of countries with lower GDPs (e.g. Cambodia) to protect their culture. Furthermore, the ability, or lack thereof, of the receiving countries to protect their culture is amplified by the existence and implementation of restrictive FDI policies imposed by their governments.

My study abroad in Bali, Indonesia, inspired this research topic as I noticed how globalization is changing the culture of its people. I learned their language and way of life which helped me understand the beauty and importance of cultural preservation. I believe we could all benefit from learning new perspectives as they could help us ideate solutions to contemporary issues and empathize with others.The Impact of Generative AI and 4th Industrial Revolution

This infographic explores the transformative power of Generative AI, a key driver of the 4th Industrial Revolution. Discover how Generative AI is revolutionizing industries, accelerating innovation, and shaping the future of work.

OAT_RI_Ep20 WeighingTheRisks_May24_Trade Wars.pptx

How will new technology fields affect economic trade?

Fabular Frames and the Four Ratio Problem

Digital, interactive art showing the struggle of a society in providing for its present population while also saving planetary resources for future generations. Spread across several frames, the art is actually the rendering of real and speculative data. The stereographic projections change shape in response to prompts and provocations. Visitors interact with the model through speculative statements about how to increase savings across communities, regions, ecosystems and environments. Their fabulations combined with random noise, i.e. factors beyond control, have a dramatic effect on the societal transition. Things get better. Things get worse. The aim is to give visitors a new grasp and feel of the ongoing struggles in democracies around the world.

Stunning art in the small multiples format brings out the spatiotemporal nature of societal transitions, against backdrop issues such as energy, housing, waste, farmland and forest. In each frame we see hopeful and frightful interplays between spending and saving. Problems emerge when one of the two parts of the existential anaglyph rapidly shrinks like Arctic ice, as factors cross thresholds. Ecological wealth and intergenerational equity areFour at stake. Not enough spending could mean economic stress, social unrest and political conflict. Not enough saving and there will be climate breakdown and ‘bankruptcy’. So where does speculative design start and the gambling and betting end? Behind each fabular frame is a four ratio problem. Each ratio reflects the level of sacrifice and self-restraint a society is willing to accept, against promises of prosperity and freedom. Some values seem to stabilise a frame while others cause collapse. Get the ratios right and we can have it all. Get them wrong and things get more desperate.

More Related Content

Viewers also liked

Types Of Deposit Account

The document discusses various types of bank deposit accounts and services, and poses problems related to banking transactions.

1. A customer lost a fixed deposit receipt and approaches the bank manager for assistance in redeeming the deposit.

2. A joint fixed deposit was issued to X and Y, and now X wants to redeem after one year or take a loan using the deposit as collateral.

3. A joint current account was held by Ram and Raj payable to either survivor, and now the bank must determine how to handle a cheque presented for payment after Raj's death.

Non banking financial institutions

The document summarizes key aspects of non-banking financial institutions (NBFIs) and non-banking financial companies (NBFCs) in India based on the Economic Survey of 2009-10. It discusses the role of NBFIs in providing medium-to-long term financing. It also describes various types of financial institutions and how NBFCs were impacted by the financial crisis. The RBI provided liquidity support to NBFCs through measures like a special repo window. Regulations for NBFCs were also strengthened regarding capital adequacy ratios and other requirements.

IDBI

IDBI was established in 1964 as a wholly-owned subsidiary of RBI to provide long-term financing to industry and agriculture. In 1976, ownership was transferred to the Government of India. IDBI has set up important financial institutions like NSE. It continues to raise capital through bonds and shares to fund its developmental activities. However, moving more into commercial banking has led to high NPAs and difficulty maintaining low funding costs.

Bank deposits

This document discusses bank deposits, including the types of deposits, factors that affect deposits, and measures to increase deposits. It also covers pricing deposits, "Know Your Customer" guidelines for opening accounts, deposit insurance, and non-deposit sources of funds for banks.

Deposits

Savings bank deposits are meant for small savers and have restrictions on withdrawals and minimum balance requirements. Current deposits are for business people and allow withdrawals by cheque but no interest. Recurring deposits encourage regular monthly savings over a fixed period by automatically depositing a set amount each month to earn interest. Fixed deposits are repaid after a specific time period but penalties apply for early closure. Proper documentation and verification is required to open any type of bank deposit.

HDFC Bank

HDFC Bank was established in 1994 as a private sector bank. It has grown to become one of the largest banks in India with over 2,000 branches and 5,000 ATMs across the country. The bank offers a wide range of products and services including credit cards, personal loans, home loans, mutual funds, and trade services. It has pursued an aggressive expansion strategy and targets both retail and corporate customers. The bank has received several awards recognizing its strong financial performance and use of technology.

non banking financial institution

This document discusses non-banking financial institutions (NBFIs) in India. It defines NBFIs as financial institutions that provide banking services without a full banking license. It outlines key differences between NBFIs and banks, importance of NBFIs, functions of NBFIs like mobilizing savings and channeling funds, types of NBFIs including insurance companies and mutual funds, regulations NBFIs must follow, guidelines on fair practices, and top performing NBFIs in India like HDFC and Bajaj Finance.

HDFC PPT

HDFC Bank was incorporated in 1994 and is headquartered in Mumbai, India. It is a major private sector bank that offers various banking products and services including loans, credit cards, savings accounts, investments, and insurance. HDFC Bank has expanded rapidly over the years through mergers and acquisitions as well as organically by opening new branches across India. It aims to continue growing its market share and delivering high quality customer service through product innovation and disciplined risk management practices.

HDFC Persentation

This document provides information about HDFC Bank, one of the major players in the Indian banking sector. It discusses HDFC Bank's history and founding in 1977, its profile including services offered such as loans, credit cards, savings accounts, and insurance. The document also outlines HDFC Bank's network of over 2,000 branches and 6,520 ATMs across India, its board of directors, and performs a basic SWOT analysis.

Sbi PPT

This document provides an analysis of opportunity for promotional strategies for State Bank of India. It begins with an overview of SBI as the largest nationalized commercial bank in India. It then defines various banking services including investment banking, retail banking, commercial banking, private banking, and asset management. It identifies SBI's target markets as current and potential customers in rural areas and tier 2/3 cities. The document outlines SBI's communication objectives of increasing awareness, attention, and purchase actions. It notes factors that affect the communication budget such as company strategy, product life cycle stage, and competitive intensity. Finally, it recommends creating communications strategies that match SBI's strategy and focus on opportunities/threats while fitting the company image, and

State Bank Of India

State Bank of India (SBI) is India's largest bank and traces its origins back to 1806. It has focused on reducing staff, computerizing operations, and improving staff attitudes through training programs like "Parivartan". SBI has a centralized organizational structure but some decentralization in loan approvals. It provides training through the State Bank Academy and has implemented new technology like SAP to respond faster to customers and enable innovation.

17689260 summer-project-on-sbi

State Bank of India (SBI) is India's largest bank with over 200 years of history. It has a large network of over 14,000 branches across India and 73 overseas offices. SBI offers a wide range of corporate, commercial, and retail banking services. Some key points about SBI include its large size and market share in India, acquisition of banks in other countries, and recognition as one of the oldest and most established banks in India. The document provides an overview of SBI's history, operations, management, products, and awards.

Financial institutions

The document provides an overview of financial institutions in India, including their definition, functions, classifications, and examples. It discusses regulatory institutions like RBI and SEBI, as well as intermediaries like IFCI, ICICI, IDBI, LIC, SIDBI, state financial corporations, and specialized institutions like EXIM Bank. It describes the roles of these institutions, the types of assistance they provide like loans and guarantees, and the process of project appraisal.

IDBI

The document provides an overview of IDBI Bank including:

- IDBI Bank was established in 1964 and was originally fully owned by the government but has since seen decreasing government ownership and an increase in private ownership.

- It has a large network of over 900 branches across India and provides various corporate and retail banking services.

- Some key investments and subsidiaries of IDBI Bank that have helped develop India's financial system are listed.

Introduction to idbi bank

Industrial Development Bank of India (IDBI) was established in 1964 to provide long-term financing to industries. It has since diversified into providing various banking services. IDBI provides loans, deposits, investment services to individuals and businesses. It has over 8,000 employees and 689 branches across India. IDBI plays an important role in the development of industries and financial markets in India by establishing institutions like the National Stock Exchange.

loans and advances in iob

Indian Overseas Bank provides various types of loans and advances to customers. These include secured loans like term loans which are granted against assets and can be paid back over longer periods. They also offer unsecured loans like demand loans which are repayable on demand. The bank aims to meet business needs through flexible financing options like cash credits while ensuring safety of funds through security and assessing borrower creditworthiness. A study of IOB's Ashoknagar branch found that term loans contribute significantly to advances and customers appreciate the bank's service, suggesting they focus on faster loan processing and financial education.

Project on SBI

Project on SBI -

I would like to acknowledge a deep sense of gratitude to Mr. Hitesh Rawat, Senior Manager of State Bank of India at Kalbadevi Road, Mumbai for giving me the opportunity & time to work on this project and given me all vital input which has led to completion of this project. Without their guidance this project would have remained in pipe dream.

I am also thankful to State Bank of India employees, who directly & indirectly extended their co-operation and invaluable support to me

Hdfc Bank

HDFC Bank is one of the major private sector banks in India. It was established in 1994 and is headquartered in Mumbai. The bank has over 5,000 branches and ATMs across India that serve corporate and retail customers. HDFC Bank aims to be a world-class bank through high quality customer service, innovative products, and leveraging new technologies. It has experienced significant growth and received several awards for its performance and services.

Viewers also liked (18)

Recently uploaded

Independent Study - College of Wooster Research (2023-2024) FDI, Culture, Glo...

Independent Study - College of Wooster Research (2023-2024) FDI, Culture, Glo...AntoniaOwensDetwiler

"Does Foreign Direct Investment Negatively Affect Preservation of Culture in the Global South? Case Studies in Thailand and Cambodia."

Do elements of globalization, such as Foreign Direct Investment (FDI), negatively affect the ability of countries in the Global South to preserve their culture? This research aims to answer this question by employing a cross-sectional comparative case study analysis utilizing methods of difference. Thailand and Cambodia are compared as they are in the same region and have a similar culture. The metric of difference between Thailand and Cambodia is their ability to preserve their culture. This ability is operationalized by their respective attitudes towards FDI; Thailand imposes stringent regulations and limitations on FDI while Cambodia does not hesitate to accept most FDI and imposes fewer limitations. The evidence from this study suggests that FDI from globally influential countries with high gross domestic products (GDPs) (e.g. China, U.S.) challenges the ability of countries with lower GDPs (e.g. Cambodia) to protect their culture. Furthermore, the ability, or lack thereof, of the receiving countries to protect their culture is amplified by the existence and implementation of restrictive FDI policies imposed by their governments.

My study abroad in Bali, Indonesia, inspired this research topic as I noticed how globalization is changing the culture of its people. I learned their language and way of life which helped me understand the beauty and importance of cultural preservation. I believe we could all benefit from learning new perspectives as they could help us ideate solutions to contemporary issues and empathize with others.The Impact of Generative AI and 4th Industrial Revolution

This infographic explores the transformative power of Generative AI, a key driver of the 4th Industrial Revolution. Discover how Generative AI is revolutionizing industries, accelerating innovation, and shaping the future of work.

OAT_RI_Ep20 WeighingTheRisks_May24_Trade Wars.pptx

How will new technology fields affect economic trade?

Fabular Frames and the Four Ratio Problem

Digital, interactive art showing the struggle of a society in providing for its present population while also saving planetary resources for future generations. Spread across several frames, the art is actually the rendering of real and speculative data. The stereographic projections change shape in response to prompts and provocations. Visitors interact with the model through speculative statements about how to increase savings across communities, regions, ecosystems and environments. Their fabulations combined with random noise, i.e. factors beyond control, have a dramatic effect on the societal transition. Things get better. Things get worse. The aim is to give visitors a new grasp and feel of the ongoing struggles in democracies around the world.

Stunning art in the small multiples format brings out the spatiotemporal nature of societal transitions, against backdrop issues such as energy, housing, waste, farmland and forest. In each frame we see hopeful and frightful interplays between spending and saving. Problems emerge when one of the two parts of the existential anaglyph rapidly shrinks like Arctic ice, as factors cross thresholds. Ecological wealth and intergenerational equity areFour at stake. Not enough spending could mean economic stress, social unrest and political conflict. Not enough saving and there will be climate breakdown and ‘bankruptcy’. So where does speculative design start and the gambling and betting end? Behind each fabular frame is a four ratio problem. Each ratio reflects the level of sacrifice and self-restraint a society is willing to accept, against promises of prosperity and freedom. Some values seem to stabilise a frame while others cause collapse. Get the ratios right and we can have it all. Get them wrong and things get more desperate.

Independent Study - College of Wooster Research (2023-2024)

"Does Foreign Direct Investment Negatively Affect Preservation of Culture in the Global South? Case Studies in Thailand and Cambodia."

Do elements of globalization, such as Foreign Direct Investment (FDI), negatively affect the ability of countries in the Global South to preserve their culture? This research aims to answer this question by employing a cross-sectional comparative case study analysis utilizing methods of difference. Thailand and Cambodia are compared as they are in the same region and have a similar culture. The metric of difference between Thailand and Cambodia is their ability to preserve their culture. This ability is operationalized by their respective attitudes towards FDI; Thailand imposes stringent regulations and limitations on FDI while Cambodia does not hesitate to accept most FDI and imposes fewer limitations. The evidence from this study suggests that FDI from globally influential countries with high gross domestic products (GDPs) (e.g. China, U.S.) challenges the ability of countries with lower GDPs (e.g. Cambodia) to protect their culture. Furthermore, the ability, or lack thereof, of the receiving countries to protect their culture is amplified by the existence and implementation of restrictive FDI policies imposed by their governments.

My study abroad in Bali, Indonesia, inspired this research topic as I noticed how globalization is changing the culture of its people. I learned their language and way of life which helped me understand the beauty and importance of cultural preservation. I believe we could all benefit from learning new perspectives as they could help us ideate solutions to contemporary issues and empathize with others.

TEST BANK Principles of cost accounting 17th edition edward j vanderbeck mari...

TEST BANK Principles of cost accounting 17th edition edward j vanderbeck maria r mitchell.docx

TEST BANK Principles of cost accounting 17th edition edward j vanderbeck maria r mitchell.docx

TEST BANK Principles of cost accounting 17th edition edward j vanderbeck maria r mitchell.docx

South Dakota State University degree offer diploma Transcript

办理美国SDSU毕业证书制作南达科他州立大学假文凭定制Q微168899991做SDSU留信网教留服认证海牙认证改SDSU成绩单GPA做SDSU假学位证假文凭高仿毕业证GRE代考如何申请南达科他州立大学South Dakota State University degree offer diploma Transcript

Bridging the gap: Online job postings, survey data and the assessment of job ...

Bridging the gap: Online job postings, survey data and the assessment of job ...Labour Market Information Council | Conseil de l’information sur le marché du travail

OJP data from firms like Vicinity Jobs have emerged as a complement to traditional sources of labour demand data, such as the Job Vacancy and Wages Survey (JVWS). Ibrahim Abuallail, PhD Candidate, University of Ottawa, presented research relating to bias in OJPs and a proposed approach to effectively adjust OJP data to complement existing official data (such as from the JVWS) and improve the measurement of labour demand.Dr. Alyce Su Cover Story - China's Investment Leader

In World Expo 2010 Shanghai – the most visited Expo in the World History

https://www.britannica.com/event/Expo-Shanghai-2010

China’s official organizer of the Expo, CCPIT (China Council for the Promotion of International Trade https://en.ccpit.org/) has chosen Dr. Alyce Su as the Cover Person with Cover Story, in the Expo’s official magazine distributed throughout the Expo, showcasing China’s New Generation of Leaders to the World.

一比一原版宾夕法尼亚大学毕业证(UPenn毕业证书)学历如何办理

挂科购买【微信号:176555708】【挂科购买(UPenn毕业证书)】【微信号:176555708】《成绩单、外壳、offer、真实留信官方学历认证(永久存档/真实可查)》采用学校原版纸张、特殊工艺完全按照原版一比一制作(包括:隐形水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠,文字图案浮雕,激光镭射,紫外荧光,温感,复印防伪)行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备,十五年致力于帮助留学生解决难题,业务范围有加拿大、英国、澳洲、韩国、美国、新加坡,新西兰等学历材料,包您满意。

【我们承诺采用的是学校原版纸张(纸质、底色、纹路)我们拥有全套进口原装设备,特殊工艺都是采用不同机器制作,仿真度基本可以达到100%,所有工艺效果都可提前给客户展示,不满意可以根据客户要求进行调整,直到满意为止!】

【业务选择办理准则】

一、工作未确定,回国需先给父母、亲戚朋友看下文凭的情况,办理一份就读学校的毕业证【微信号:176555708】文凭即可

二、回国进私企、外企、自己做生意的情况,这些单位是不查询毕业证真伪的,而且国内没有渠道去查询国外文凭的真假,也不需要提供真实教育部认证。鉴于此,办理一份毕业证【微信号:176555708】即可

三、进国企,银行,事业单位,考公务员等等,这些单位是必需要提供真实教育部认证的,办理教育部认证所需资料众多且烦琐,所有材料您都必须提供原件,我们凭借丰富的经验,快捷的绿色通道帮您快速整合材料,让您少走弯路。

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

留信网服务项目:

1、留学生专业人才库服务(留信分析)

2、国(境)学习人员提供就业推荐信服务

3、留学人员区块链存储服务

【关于价格问题(保证一手价格)】

我们所定的价格是非常合理的,而且我们现在做得单子大多数都是代理和回头客户介绍的所以一般现在有新的单子 我给客户的都是第一手的代理价格,因为我想坦诚对待大家 不想跟大家在价格方面浪费时间

对于老客户或者被老客户介绍过来的朋友,我们都会适当给一些优惠。

选择实体注册公司办理,更放心,更安全!我们的承诺:客户在留信官方认证查询网站查询到认证通过结果后付款,不成功不收费!

1比1复刻(ksu毕业证书)美国堪萨斯州立大学毕业证本科文凭证书原版一模一样

原版定制【微信:bwp0011】《(ksu毕业证书)美国堪萨斯州立大学毕业证本科文凭证书》【微信:bwp0011】成绩单 、雅思、外壳、留信学历认证永久存档查询,采用学校原版纸张、特殊工艺完全按照原版一比一制作(包括:隐形水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠,文字图案浮雕,激光镭射,紫外荧光,温感,复印防伪)行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备,十五年致力于帮助留学生解决难题,业务范围有加拿大、英国、澳洲、韩国、美国、新加坡,新西兰等学历材料,包您满意。

【业务选择办理准则】

一、工作未确定,回国需先给父母、亲戚朋友看下文凭的情况,办理一份就读学校的毕业证【微信bwp0011】文凭即可

二、回国进私企、外企、自己做生意的情况,这些单位是不查询毕业证真伪的,而且国内没有渠道去查询国外文凭的真假,也不需要提供真实教育部认证。鉴于此,办理一份毕业证【微信bwp0011】即可

三、进国企,银行,事业单位,考公务员等等,这些单位是必需要提供真实教育部认证的,办理教育部认证所需资料众多且烦琐,所有材料您都必须提供原件,我们凭借丰富的经验,快捷的绿色通道帮您快速整合材料,让您少走弯路。

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

【关于价格问题(保证一手价格)】

我们所定的价格是非常合理的,而且我们现在做得单子大多数都是代理和回头客户介绍的所以一般现在有新的单子 我给客户的都是第一手的代理价格,因为我想坦诚对待大家 不想跟大家在价格方面浪费时间

对于老客户或者被老客户介绍过来的朋友,我们都会适当给一些优惠。

TechnoXander Confirmation of Payee Product Pack 1.pdf

Confirmation of Payee (CoP) is a vital security measure adopted by financial institutions and payment service providers. Its core purpose is to confirm that the recipient’s name matches the information provided by the sender during a banking transaction, ensuring that funds are transferred to the correct payment account.

Confirmation of Payee was built to tackle the increasing numbers of APP Fraud and in the landscape of UK banking, the spectre of APP fraud looms large. In 2022, over £1.2 billion was stolen by fraudsters through authorised and unauthorised fraud, equivalent to more than £2,300 every minute. This statistic emphasises the urgent need for robust security measures like CoP. While over £1.2 billion was stolen through fraud in 2022, there was an eight per cent reduction compared to 2021 which highlights the positive outcomes obtained from the implementation of Confirmation of Payee. The number of fraud cases across the UK also decreased by four per cent to nearly three million cases during the same period; latest statistics from UK Finance.

In essence, Confirmation of Payee plays a pivotal role in digital banking, guaranteeing the flawless execution of banking transactions. It stands as a guardian against fraud and misallocation, demonstrating the commitment of financial institutions to safeguard their clients’ assets. The next time you engage in a banking transaction, remember the invaluable role of CoP in ensuring the security of your financial interests.

For more details, you can visit https://technoxander.com.

一比一原版(cwu毕业证书)美国中央华盛顿大学毕业证如何办理

原版一模一样【微信:741003700 】【(cwu毕业证书)美国中央华盛顿大学毕业证成绩单】【微信:741003700 】学位证,留信认证(真实可查,永久存档)原件一模一样纸张工艺/offer、雅思、外壳等材料/诚信可靠,可直接看成品样本,帮您解决无法毕业带来的各种难题!外壳,原版制作,诚信可靠,可直接看成品样本。行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备。十五年致力于帮助留学生解决难题,包您满意。

本公司拥有海外各大学样板无数,能完美还原。

1:1完美还原海外各大学毕业材料上的工艺:水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠。文字图案浮雕、激光镭射、紫外荧光、温感、复印防伪等防伪工艺。材料咨询办理、认证咨询办理请加学历顾问Q/微741003700

【主营项目】

一.毕业证【q微741003700】成绩单、使馆认证、教育部认证、雅思托福成绩单、学生卡等!

二.真实使馆公证(即留学回国人员证明,不成功不收费)

三.真实教育部学历学位认证(教育部存档!教育部留服网站永久可查)

四.办理各国各大学文凭(一对一专业服务,可全程监控跟踪进度)

如果您处于以下几种情况:

◇在校期间,因各种原因未能顺利毕业……拿不到官方毕业证【q/微741003700】

◇面对父母的压力,希望尽快拿到;

◇不清楚认证流程以及材料该如何准备;

◇回国时间很长,忘记办理;

◇回国马上就要找工作,办给用人单位看;

◇企事业单位必须要求办理的

◇需要报考公务员、购买免税车、落转户口

◇申请留学生创业基金

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

办理(cwu毕业证书)美国中央华盛顿大学毕业证【微信:741003700 】外观非常简单,由纸质材料制成,上面印有校徽、校名、毕业生姓名、专业等信息。

办理(cwu毕业证书)美国中央华盛顿大学毕业证【微信:741003700 】格式相对统一,各专业都有相应的模板。通常包括以下部分:

校徽:象征着学校的荣誉和传承。

校名:学校英文全称

授予学位:本部分将注明获得的具体学位名称。

毕业生姓名:这是最重要的信息之一,标志着该证书是由特定人员获得的。

颁发日期:这是毕业正式生效的时间,也代表着毕业生学业的结束。

其他信息:根据不同的专业和学位,可能会有一些特定的信息或章节。

办理(cwu毕业证书)美国中央华盛顿大学毕业证【微信:741003700 】价值很高,需要妥善保管。一般来说,应放置在安全、干燥、防潮的地方,避免长时间暴露在阳光下。如需使用,最好使用复印件而不是原件,以免丢失。

综上所述,办理(cwu毕业证书)美国中央华盛顿大学毕业证【微信:741003700 】是证明身份和学历的高价值文件。外观简单庄重,格式统一,包括重要的个人信息和发布日期。对持有人来说,妥善保管是非常重要的。

falcon-invoice-discounting-a-premier-investment-platform-for-superior-returns...

falcon-invoice-discounting-a-premier-investment-platform-for-superior-returns...Falcon Invoice Discounting

Falcon stands out as a top-tier P2P Invoice Discounting platform in India, bridging esteemed blue-chip companies and eager investors. Our goal is to transform the investment landscape in India by establishing a comprehensive destination for borrowers and investors with diverse profiles and needs, all while minimizing risk. What sets Falcon apart is the elimination of intermediaries such as commercial banks and depository institutions, allowing investors to enjoy higher yields.Tdasx: In-Depth Analysis of Cryptocurrency Giveaway Scams and Security Strate...

Tdasx: In-Depth Analysis of Cryptocurrency Giveaway Scams and Security Strategies

一比一原版(RMIT毕业证)皇家墨尔本理工大学毕业证如何办理

RMIT硕士学位证成绩单【微信95270640】《皇家墨尔本理工大学毕业证书》《QQ微信95270640》学位证书电子版:在线制作皇家墨尔本理工大学毕业证成绩单GPA修改(制作RMIT毕业证成绩单RMIT文凭证书样本)、皇家墨尔本理工大学毕业证书与成绩单样本图片、《RMIT学历证书学位证书》、皇家墨尔本理工大学毕业证案例毕业证书制作軟體、在线制作加拿大硕士学历证书真实可查.

【本科硕士】皇家墨尔本理工大学皇家墨尔本理工大学本科学位证成绩单(GPA修改);学历认证(教育部认证);大学Offer录取通知书留信认证使馆认证;雅思语言证书等高仿类证书。

办理流程:

1客户提供办理皇家墨尔本理工大学皇家墨尔本理工大学本科学位证成绩单信息:姓名生日专业学位毕业时间等(如信息不确定可以咨询顾问:我们有专业老师帮你查询);

2开始安排制作毕业证成绩单电子图;

3毕业证成绩单电子版做好以后发送给您确认;

4毕业证成绩单电子版您确认信息无误之后安排制作成品;

5成品做好拍照或者视频给您确认;

6快递给客户(国内顺丰国外DHLUPS等快读邮寄)

真实网上可查的证明材料

1教育部学历学位认证留服官网真实存档可查永久存档。

2留学回国人员证明(使馆认证)使馆网站真实存档可查。

我们对海外大学及学院的毕业证成绩单所使用的材料尺寸大小防伪结构(包括:皇家墨尔本理工大学皇家墨尔本理工大学本科学位证成绩单隐形水印阴影底纹钢印LOGO烫金烫银LOGO烫金烫银复合重叠。文字图案浮雕激光镭射紫外荧光温感复印防伪)都有原版本文凭对照。质量得到了广大海外客户群体的认可同时和海外学校留学中介做到与时俱进及时掌握各大院校的(毕业证成绩单资格证结业证录取通知书在读证明等相关材料)的版本更新信息能够在第一时间掌握最新的海外学历文凭的样版尺寸大小纸张材质防伪技术等等并在第一时间收集到原版实物以求达到客户的需求。

本公司还可以按照客户原版印刷制作且能够达到客户理想的要求。有需要办理证件的客户请联系我们在线客服中心微信:95270640 或咨询在线父亲的家很狭小除了一张单人床和一张小方桌几乎没有多余的空间山娃一下子就联想起学校的男小便处山娃很想笑却怎么也笑不出来山娃很迷惑父亲的家除了一扇小铁门连窗户也没有墓穴一般阴森森有些骇人父亲的城也便成了山娃的城父亲的家也便成了山娃的家父亲让山娃呆在屋里做作业看电视最多只能在门口透透气不能跟陌生人搭腔更不能乱跑一怕迷路二怕拐子拐人山娃很惊惧去年村里的田鸡就因为跟父亲进城一不小心被人拐跑了至今不见踪影害不

Seeman_Fiintouch_LLP_Newsletter_Jun_2024.pdf

The Impact of the 2024 Indian

Election Beyond Borders

01. Investment Gyan

02. Market Update

03. Inspiration investment story

Accounting Information Systems (AIS).pptx

An accounting information system (AIS) refers to tools and systems designed for the collection and display of accounting information so accountants and executives can make informed decisions.

Recently uploaded (20)

Independent Study - College of Wooster Research (2023-2024) FDI, Culture, Glo...

Independent Study - College of Wooster Research (2023-2024) FDI, Culture, Glo...

The Impact of Generative AI and 4th Industrial Revolution

The Impact of Generative AI and 4th Industrial Revolution

OAT_RI_Ep20 WeighingTheRisks_May24_Trade Wars.pptx

OAT_RI_Ep20 WeighingTheRisks_May24_Trade Wars.pptx

Independent Study - College of Wooster Research (2023-2024)

Independent Study - College of Wooster Research (2023-2024)

TEST BANK Principles of cost accounting 17th edition edward j vanderbeck mari...

TEST BANK Principles of cost accounting 17th edition edward j vanderbeck mari...

South Dakota State University degree offer diploma Transcript

South Dakota State University degree offer diploma Transcript

Bridging the gap: Online job postings, survey data and the assessment of job ...

Bridging the gap: Online job postings, survey data and the assessment of job ...

Dr. Alyce Su Cover Story - China's Investment Leader

Dr. Alyce Su Cover Story - China's Investment Leader

TechnoXander Confirmation of Payee Product Pack 1.pdf

TechnoXander Confirmation of Payee Product Pack 1.pdf

falcon-invoice-discounting-a-premier-investment-platform-for-superior-returns...

falcon-invoice-discounting-a-premier-investment-platform-for-superior-returns...

Tdasx: In-Depth Analysis of Cryptocurrency Giveaway Scams and Security Strate...

Tdasx: In-Depth Analysis of Cryptocurrency Giveaway Scams and Security Strate...