Downloaded 25 times

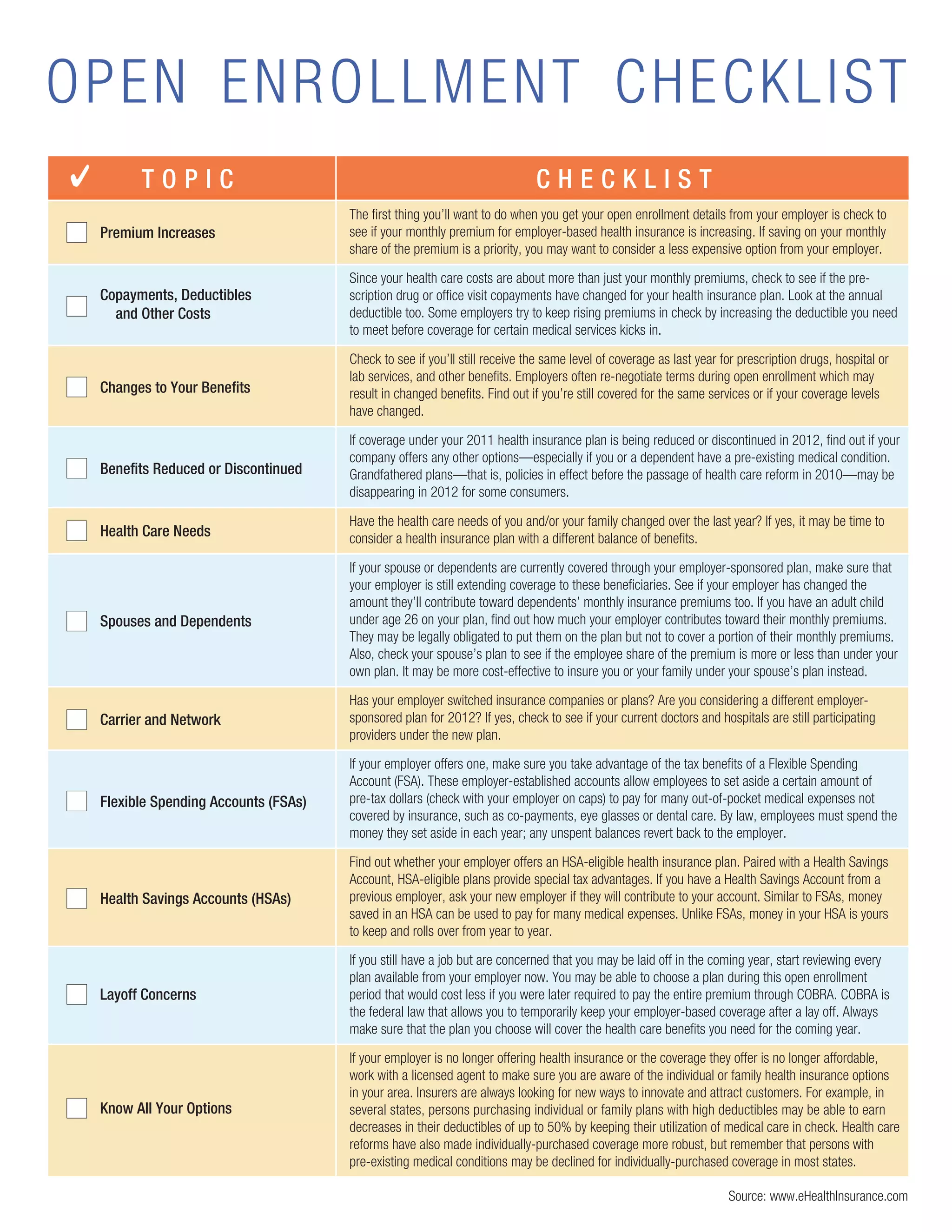

During open enrollment, employees should review their health insurance options carefully, checking for premium increases, changes in deductibles, and coverage levels. It's important to verify if dependents are still covered and to consider costs under a spouse's plan. Those concerned about potential layoffs should evaluate plans that allow for affordable COBRA continuation coverage, while individuals with pre-existing conditions should explore available options in their state.