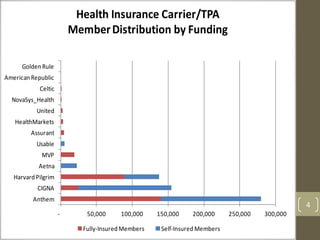

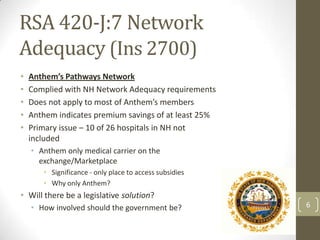

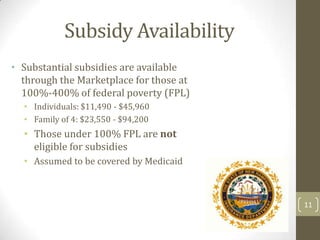

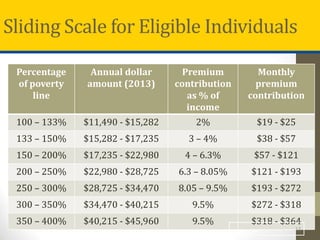

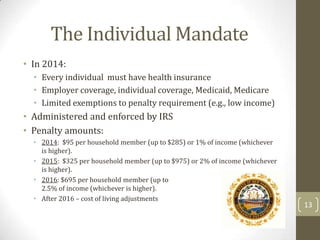

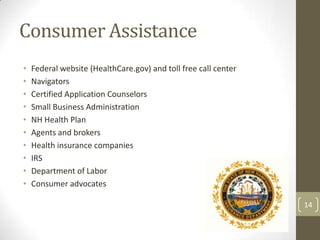

The document discusses the impact of the Affordable Care Act (ACA) on health insurance markets in New Hampshire, highlighting the changes implemented in 2014, including the individual mandate and new insurance rules. It outlines the coverage distribution among various employer sizes, the structure of insurance carriers, and factors influencing competition in the market. Additionally, the document details the subsidies available for individuals and families, emphasizing the importance of enrolling through the marketplace for coverage beginning January 1, 2014.

![PERI-PROSTHETIC FRACTURE NAIL-PLATE CONSTRUCT [NPC].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/drarunkumardrmohamedashrafperiprostheticfrasturenail-plateconstructnpc-260209164459-7e9d15a1-thumbnail.jpg?width=640&height=640&fit=bounds)

![CTEV [ clubfoot] DR ARUN LAL ,DR MOHAMED ASHRAF travancore medical college k...](https://cdn.slidesharecdn.com/ss_thumbnails/ctevclubfootdrarunlaldrmohamedashraftravancoremedicalcollegekollamkeralaindia-260208063247-18fc466c-thumbnail.jpg?width=640&height=640&fit=bounds)