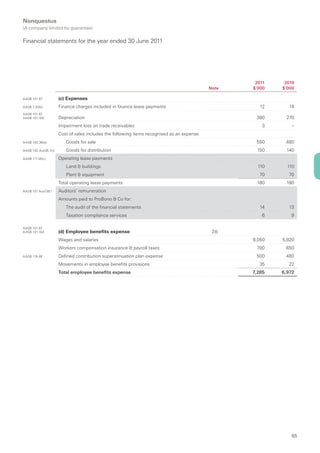

Downloaded 31 times

This document summarizes an annual report published by the Institute of Chartered Accountants in Australia about best practices for not-for-profit annual and financial reporting. The Institute represents over 67,000 Chartered Accountants working in diverse roles around the world. The report discusses the Institute's role in setting high standards, engaging stakeholders, and leveraging its membership in the Global Accounting Alliance. It was informed by findings from the PwC Transparency Awards, which recognize quality and transparency in not-for-profit reporting. The report aims to provide practical guidance to not-for-profits on meeting financial reporting responsibilities and improving organizational performance.