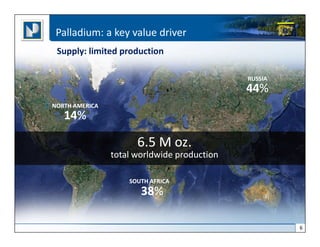

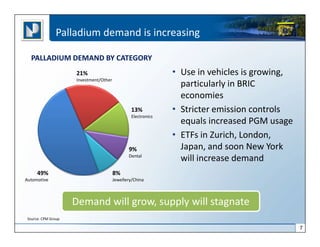

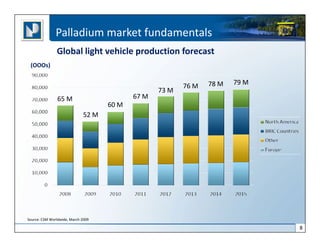

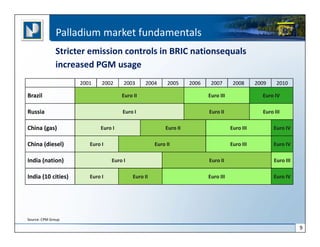

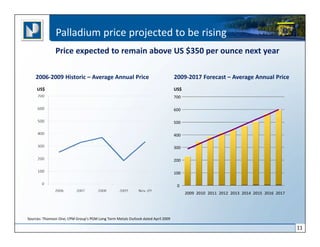

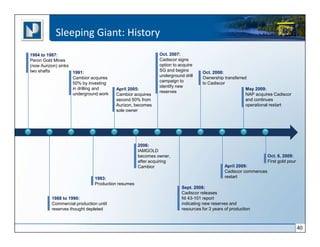

This presentation discusses North American Palladium's plans to capitalize on rising palladium prices by restarting its flagship Lac des Iles palladium mine in Ontario. It has also commenced gold production at its Sleeping Giant mine in Quebec. The company aims to grow its gold production to 250,000 ounces annually through acquisitions. It has over $100 million in cash and no debt on its balance sheet. Palladium demand is expected to increase significantly due to stricter emissions controls, while supply will remain constrained. The palladium price is projected to remain above $350 per ounce through 2017.