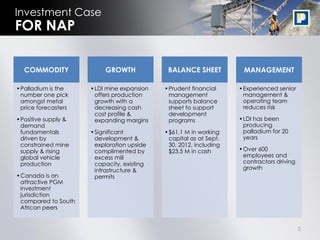

- The presentation provides an investment case for Napier Ventures Inc. (NAP), a palladium mining company, highlighting NAP's commodity growth potential, strong balance sheet, and experienced management team.

- NAP's Lac des Iles mine expansion offers production and cost profile improvements while significant development and exploration upside is complemented by excess mill capacity and infrastructure.

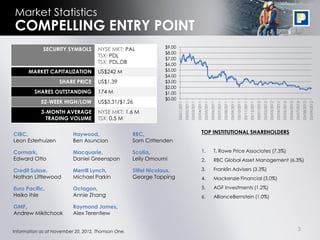

- At a market capitalization of US$242 million and share price of US$1.39, the presentation argues NAP presents a compelling entry point for investment in the palladium mining sector.