INSURANCE MONEY CONFERENCE2009 Η ασφαλιστική αγορά απέναντι στις προκλήσεις του νέου θεσμικού πλαισίου εποπτείας και τις προσδοκίες των καταναλωτών Ιωάννης Βασιλάτος Γεώργιος Μαμουλάκης Αντώνιος Καλλιβωκάς Αθήνα, 25 Νοεμβρίου 200 9

Η ασφαλιστική αγοράαπέναντι στις προκλήσεις του νέου θεσμικού πλαισίου εποπτείας και τις προσδοκίες των καταναλωτών

6.

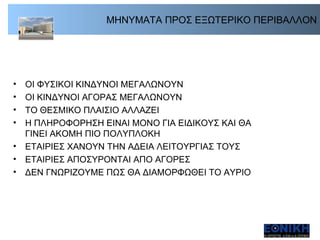

ΜΗΝΥΜΑΤΑ ΠΡΟΣ ΕΞΩΤΕΡΙΚΟΠΕΡΙΒΑΛΛΟΝ ΟΙ ΦΥΣΙΚΟΙ ΚΙΝΔΥΝΟΙ ΜΕΓΑΛΩΝΟΥΝ ΟΙ ΚΙΝΔΥΝΟΙ ΑΓΟΡΑΣ ΜΕΓΑΛΩΝΟΥΝ ΤΟ ΘΕΣΜΙΚΟ ΠΛΑΙΣΙΟ ΑΛΛΑΖΕΙ Η ΠΛΗΡΟΦΟΡΗΣΗ ΕΙΝΑΙ ΜΟΝΟ ΓΙΑ ΕΙΔΙΚΟΥΣ ΚΑΙ ΘΑ ΓΙΝΕΙ ΑΚΟΜΗ ΠΙΟ ΠΟΛΥΠΛΟΚΗ ΕΤΑΙΡΙΕΣ ΧΑΝΟΥΝ ΤΗΝ ΑΔΕΙΑ ΛΕΙΤΟΥΡΓΙΑΣ ΤΟΥΣ ΕΤΑΙΡΙΕΣ ΑΠΟΣΥΡΟΝΤΑΙ ΑΠΟ ΑΓΟΡΕΣ ΔΕΝ ΓΝΩΡΙΖΟΥΜΕ ΠΩΣ ΘΑ ΔΙΑΜΟΡΦΩΘΕΙ ΤΟ ΑΥΡΙΟ

7.

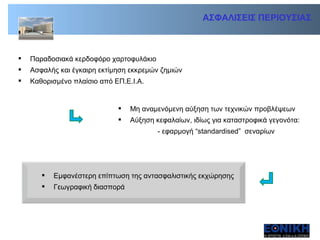

ΑΣΦΑΛΙΣΕΙΣ ΠΕΡΙΟΥΣΙΑΣ Παραδοσιακάκερδοφόρο χαρτοφυλάκιο Ασφαλής και έγκαιρη εκτίμηση εκκρεμών ζημιών Καθορισμένο πλαίσιο από ΕΠ.Ε.Ι.Α . Μη αναμενόμενη αύξηση των τεχνικών προβλέψεων Αύξηση κεφαλαίων , ιδίως για καταστροφικά γεγονότα : - εφαρμογή “standardised” σεναρίων Εμφανέστερη επίπτωση της αντασφαλιστικής εκχώρησης Γεωγραφική διασπορά

8.

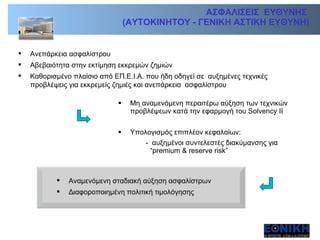

ΑΣΦΑΛΙΣΕΙΣ ΕΥΘΥΝΗΣ (ΑΥΤΟΚΙΝΗΤΟΥ - ΓΕΝΙΚΗ ΑΣΤΙΚΗ ΕΥΘΥΝΗ) Ανεπάρκεια ασφαλίστρου Αβεβαιότητα στην εκτίμηση εκκρεμών ζημιών Καθορισμένο πλαίσιο από ΕΠ . Ε . Ι . Α . που ήδη οδηγεί σε αυξημένες τεχνικές προβλέψεις για εκκρεμείς ζημιές και ανεπάρκεια ασφαλίστρου Μη αναμενόμενη περαιτέρω αύξηση των τεχνικών προβλέψεων κατά την εφαρμογή του Solvency II Υπολογισμός επιπλέον κεφαλαίων : - αυξημένοι συντελεστές διακύμανσης για “premium & reserve risk” Αναμενόμενη σταδιακή αύξηση ασφαλίστρων Διαφοροποιημένη πολιτική τιμολόγησης

9.

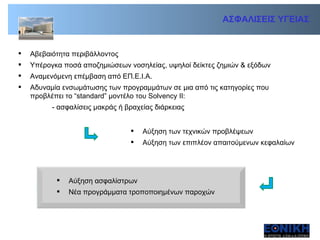

ΑΣΦΑΛΙΣΕΙΣ ΥΓΕΙΑΣ Αβεβαιότηταπεριβάλλοντος Υπέρογκα ποσά αποζημιώσεων νοσηλείας, υψηλοί δείκτες ζημιών & εξόδων Αναμενόμενη επέμβαση από ΕΠ.Ε.Ι.Α . Αδυναμία ενσωμάτωσης των προγραμμάτων σε μια από τις κατηγορίες που προβλέπει το “standard” μοντέλο του Solvency II: - ασφαλίσεις μακράς ή βραχείας διάρκειας Αύξηση των τεχνικών προβλέψεων Αύξηση των επιπλέον απαιτούμενων κεφαλαίων Αύξηση ασφαλίστρων Νέα προγράμματα τροποποιημένων παροχών

10.

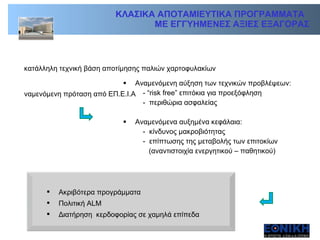

ΚΛΑΣΙΚΑ ΑΠΟΤΑΜΙΕΥΤΙΚΑ ΠΡΟΓΡΑΜΜΑΤΑ ΜΕ ΕΓΓΥΗΜΕΝΕΣ ΑΞΙΕΣ ΕΞΑΓΟΡΑΣ Ακατάλληλη τεχνική βάση αποτίμησης παλιών χαρτοφυλακίων Αναμενόμενη πρόταση από ΕΠ . Ε . Ι . Α Αναμενόμενη αύξηση των τεχνικών προβλέψεων : - “risk free” επιτόκια για προεξόφληση - περιθώρια ασφαλείας Αναμενόμενα αυξημένα κεφάλαια : - κίνδυνος μακροβιότητας - επίπτωσης της μεταβολής των επιτοκίων ( αναντιστοιχία ενεργητικού – παθητικού) Ακριβότερα προγράμματα Πολιτική ALM Διατήρηση κερδοφορίας σε χαμηλά επίπεδα

11.

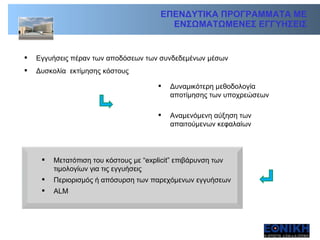

ΕΠΕΝΔΥΤΙΚΑ ΠΡΟΓΡΑΜΜΑΤΑ ΜΕ ΕΝΣΩΜΑΤΩΜΕΝΕΣ ΕΓΓΥΗΣΕΙΣ Εγγυήσεις πέραν των αποδόσεων των συνδεδεμένων μέσων Δυσκολία εκτίμησης κόστους Δυναμικότερη μεθοδολογία αποτίμησης των υποχρεώσεων Αναμενόμενη αύξηση των απαιτούμενων κεφαλαίων Μετατόπιση του κόστους με “explicit” επιβάρυνση των τιμολογίων για τις εγγυήσεις Περιορισμός ή απόσυρση των παρεχόμενων εγγυήσεων ALM

12.

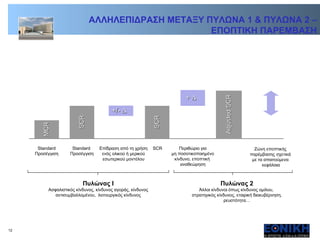

SCR MCR AdjustedSCR + +/- Standard Προσέγγιση Standard Προσέγγιση Επίδραση από τη χρήση ενός ολικού ή μερικού εσωτερικού μοντέλου SCR Περιθώριο για μη ποσοτικοποιημένο κίνδυνο, εποπτική αναθεώρηση Ζώνη εποπτικής παρέμβασης σχετικά με τα απαιτούμενα κεφάλαια Πυλώνας I Ασφαλιστικός κίνδυνος, κίνδυνος αγοράς, κίνδυνος αντισυμβαλλομένου, λειτουργικός κίνδυνος Πυλώνας 2 Άλλοι κίνδυνοι όπως κίνδυνος ομίλου, στρατηγικός κίνδυνος, εταιρική διακυβέρνηση , ρευστότητα … SCR ΑΛΛΗΛΕΠΙΔΡΑΣΗ ΜΕΤΑΞΥ ΠΥΛΩΝΑ 1 & ΠΥΛΩΝΑ 2 – ΕΠΟΠΤΙΚΗ ΠΑΡΕΜΒΑΣΗ

13.

Εποπτική επισκόπηση (SRP ) : Έλεγχος και επισκόπηση των συμμορφωτικών διαδικασιών, της εταιρικής διακυβέρνησης, της διαχείρισης και του επιπέδου των κινδύνων Εταιρική οργάνωση, Πλαίσιο Διαχείρισης Κινδύνων, Fit & Pr ο per, Outsourcing, ORSA, Αναλογιστική, Εσωτερικός Έλεγχος Επιπρόσθετα κεφάλαια ; Πλεονέκτημα θα έχουν οι εταιρίες οι οποίες δεν περιμένουν την Εποπτική Αρχή να απαιτήσει, αλλά έχουν ήδη ενσωματώσει (Π ΙΙ), και μπορούν να αποδείξουν (Π ΙΙΙ) τον όρο κίνδυνο Στην εταιρική στρατηγική ( business plan, διαμόρφωση χαρτοφυλακίου, είσοδος/έξοδος από αγορές, …) Σε όλη την ιεραρχία της εταιρίας Στη στοχοθέτηση, αξιολόγηση και αμοιβή Βλ. CP 58 (Supervisory Reporting and Public Disclosure Requirements) Βλ. CP 33 (System of Governance) ΠΟΙΟΤΙΚΕΣ ΑΠΑΙΤΗΣΕΙΣ ΒΑΣΕΙ ΤΟΥ ΠΥΛΩΝΑ ΙΙ & ΙΙΙ

14.

2 0 10 ΚΑΤΑΓΡΑΦΗ – ΥΠΟΛΟΓΙΣΜΟΣ – ΔΙΑΧΕΙΡΙΣΗ ΚΙΝΔΥΝΩΝ ΜΕΛΕΤΕΣ ΕΠΙΠΤΩΣΕΩΝ QIS 4 KAI QIS 5 AME ΣΗ ΕΝΑΡΞΗ ΑΝΑΛΥΤΙΚΟΥ ΔΙΑΛΟΓΟΥ ΜΕ ΕΠ.Ε.Ι.Α. ΣΥΛΛΟΓΗ ΣΤΟΙΧΕΙΩΝ – ΑΛΛΑΓΗ ΣΥΣΤΗΜΑΤΩΝ ΙΤ ΚΑΙ ΜΙ S ΕΠΙΛΟΓΗ ΕΝΑΛΛΑΚΤΙΚΩΝ ΣΤΑ ΠΛΑΙΣΙΑ ΤΟΥ SOLVENCY II ΕΠΑΝΑΠΡΟΣΔΙΟΡΙΣΜΟΣ ΣΤΡΑΤΗΓΙΚΗΣ ΔΙΑΧΕΙΡΙΣΗ ΑΛΛΑΓΗΣ – ΑΠΟΡΡΟΦΗΣΗ ΣΟΚ ΜΕΤΑΒΑΣΗΣ Η ασφαλιστική αγορά απέναντι στις προκλήσεις του νέου θεσμικού πλαισίου εποπτείας και τις προσδοκίες των καταναλωτών

15.

2011 - 2012ΘΑ ΑΛΛΑΞΟΥΝ ΤΑ ΠΡΟΣΦΕΡΟΜΕΝΑ ΠΡΟΪΟΝΤΑ ΘΑ ΑΥΞΗΘΟΥΝ ΟΙ ΣΥΓΧΩΝΕΥΣΕΙΣ Ή / ΚΑΙ ΟΙ ΠΤΩΧΕΥΣΕΙΣ Ο ΑΝΤΑΓΩΝΙΣΜΟΣ ΣΤΗΝ ΕΛΛΗΝΙΚΗ ΑΓΟΡΑ ΘΑ ΔΙΑΦΟΡΟΠΟΙΗΘΕΙ ΘΑ ΑΥΞΗΘΕΙ Η ΔΙΑΦΑΝΕΙΑ ΘΑ ΑΥΞΗΘΟΥΝ ΟΙ ΑΝΑΓΚΕΣ ΣΕ ΚΕΦΑΛΑΙΑ ΘΑ ΥΠΑΡΧΟΥΝ ΔΙΑΘΕΣΙΜΟΙ ΕΠΕΝΔΥΤΕΣ; ΘΑ ΥΠΑΡΧΟΥΝ ΔΙΑΘΕΣΙΜΟΙ ΠΕΛΑΤΕΣ; Η ασφαλιστική αγορά απέναντι στις προκλήσεις του νέου θεσμικού πλαισίου εποπτείας και τις προσδοκίες των καταναλωτών

16.

Η ασφαλιστική αγοράαπέναντι στις προκλήσεις του νέου θεσμικού πλαισίου εποπτείας και τις προσδοκίες των καταναλωτών

17.

Σας Ευχαριστούμε! ΓεώργιοςΜαμουλάκης Διευθυντής Αναλογιστικής Τηλ. 210-9099596 Fax 210-9099 569 [email_address] Ιωάννης Βασιλάτος Αναπλ. Γεν. Διευθυντής & CFO Τηλ. 210-9099 433 Fax 210-9099473 [email_address] Αντώνιος Καλλιβωκάς Αναπλ. Διευθυντής & CRO Τηλ. 210-9099489 Fax 210-9099 569 [email_address] Εθνική Ασφαλιστική Λ. Συγγρού 103 -105 117 45 Αθήνα Η ασφαλιστική αγορά απέναντι στις προκλήσεις του νέου θεσμικού πλαισίου εποπτείας και τις προσδοκίες των καταναλωτών Αθήνα, 25 Νοεμβρίου 200 9

![Σας Ευχαριστούμε! Γεώργιος Μαμουλάκης Διευθυντής Αναλογιστικής Τηλ. 210-9099596 Fax 210-9099 569 [email_address] Ιωάννης Βασιλάτος Αναπλ. Γεν. Διευθυντής & CFO Τηλ. 210-9099 433 Fax 210-9099473 [email_address] Αντώνιος Καλλιβωκάς Αναπλ. Διευθυντής & CRO Τηλ. 210-9099489 Fax 210-9099 569 [email_address] Εθνική Ασφαλιστική Λ. Συγγρού 103 -105 117 45 Αθήνα Η ασφαλιστική αγορά απέναντι στις προκλήσεις του νέου θεσμικού πλαισίου εποπτείας και τις προσδοκίες των καταναλωτών Αθήνα, 25 Νοεμβρίου 200 9](https://image.slidesharecdn.com/08moneyconf20091125-091210055502-phpapp02/85/Money-Conf-20091125-17-320.jpg)