Download to read offline

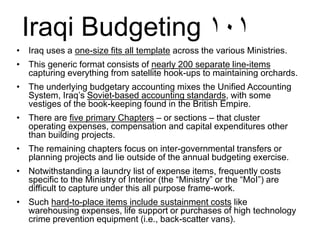

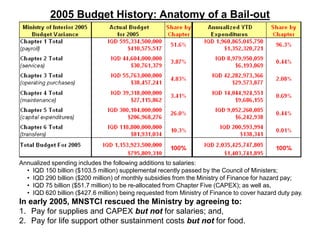

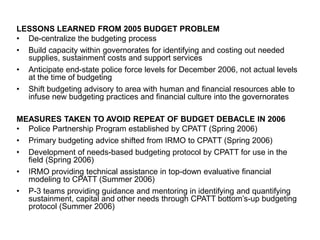

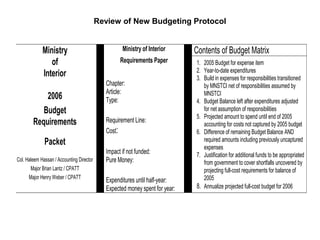

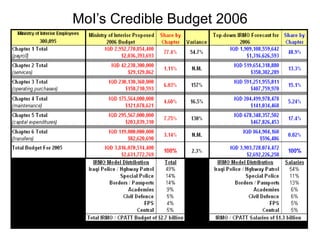

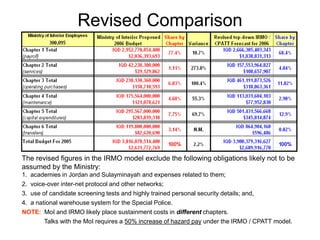

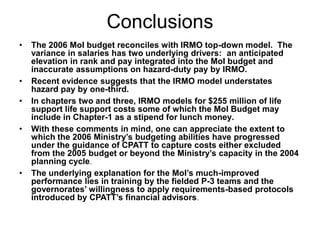

The document discusses issues with Iraq's 2005 budget for the Ministry of Interior and improvements made for the 2006 budget. The 2005 budget lacked credibility due to inaccurate personnel numbers and failure to account for changes made by the Coalition. There was an absence of communication between budget advisors and the field. The budget failed to capture new expenses for decentralized operations. Lessons from 2005 included the need to decentralize budgeting, build capacity in provinces, anticipate future force levels, and shift advising to entities able to introduce new budgeting practices. Measures for 2006 included new budgeting protocols and guidance from the Coalition Police Partnership Program. The 2006 budget reconciled with revised models and captured costs excluded previously. Improved

![Ameri credit research_report_winter_2003[1] (1)](https://cdn.slidesharecdn.com/ss_thumbnails/americreditresearchreportwinter200311-150810183337-lva1-app6892-thumbnail.jpg?width=640&height=640&fit=bounds)