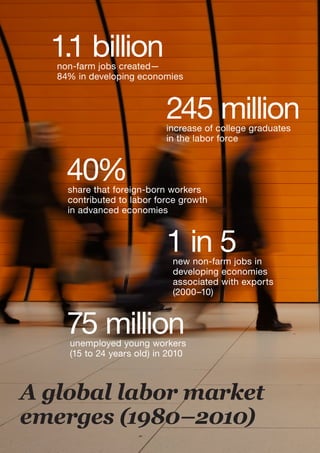

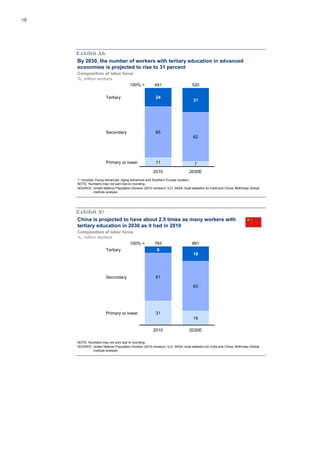

The McKinsey Global Institute's June 2012 report analyzes the evolving global labor market, predicting a global labor force of 3.5 billion by 2030 and significant skill gaps, particularly a shortage of high-skill workers and a surplus of low-skill workers. It highlights challenges such as youth unemployment and calls for urgent educational and training initiatives to mitigate these imbalances. The report emphasizes the need for a concerted effort to address the growing disparity between labor supply and demand, which could lead to increased poverty and inequality.

![5G Explained! A High Level Overview [Introduction]](https://cdn.slidesharecdn.com/ss_thumbnails/5gexplainedahighleveloverview-260119165306-cc137a3e-thumbnail.jpg?width=640&height=640&fit=bounds)