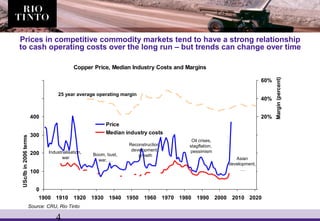

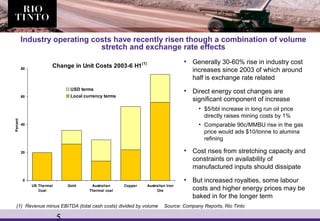

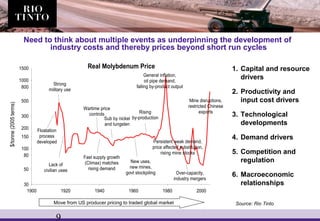

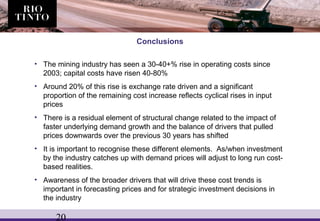

This document discusses long-term trends in costs and prices for the mining industry. It finds that mining costs have increased 30-40% since 2003 due to factors like rising input costs, currency fluctuations, and constraints on expanding supply. This cost increase is partly cyclical but also reflects structural changes from stronger demand growth outpacing productivity gains. Understanding the dynamics between resource availability, demand growth, and industry productivity is important for forecasting future price trends and investment in the mining sector.