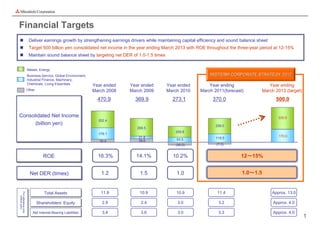

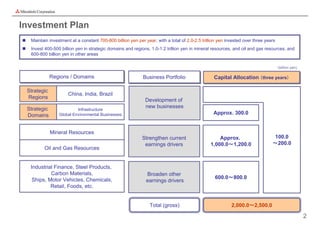

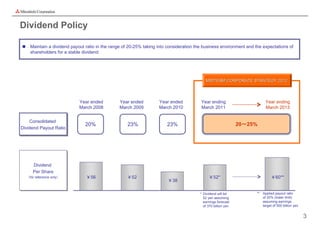

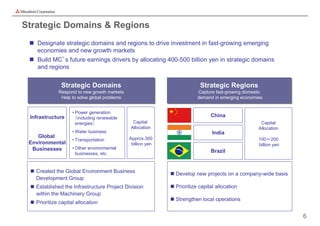

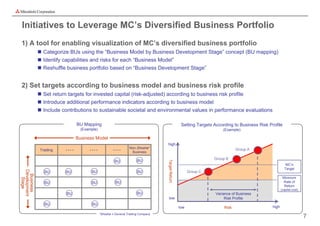

Mitsubishi Corporation outlines its midterm corporate strategy for 2012-2013. The strategy aims to strengthen existing businesses and develop new growth areas to deliver sustainable corporate value. Key elements include investing in strategic regions and domains like China, India, Brazil, and environmental businesses; cultivating new earnings drivers through its diverse portfolio; and solidifying the business portfolio with initiatives like a new management committee. Financial targets include 500 billion yen in net income by March 2013 and maintaining a sound balance sheet.