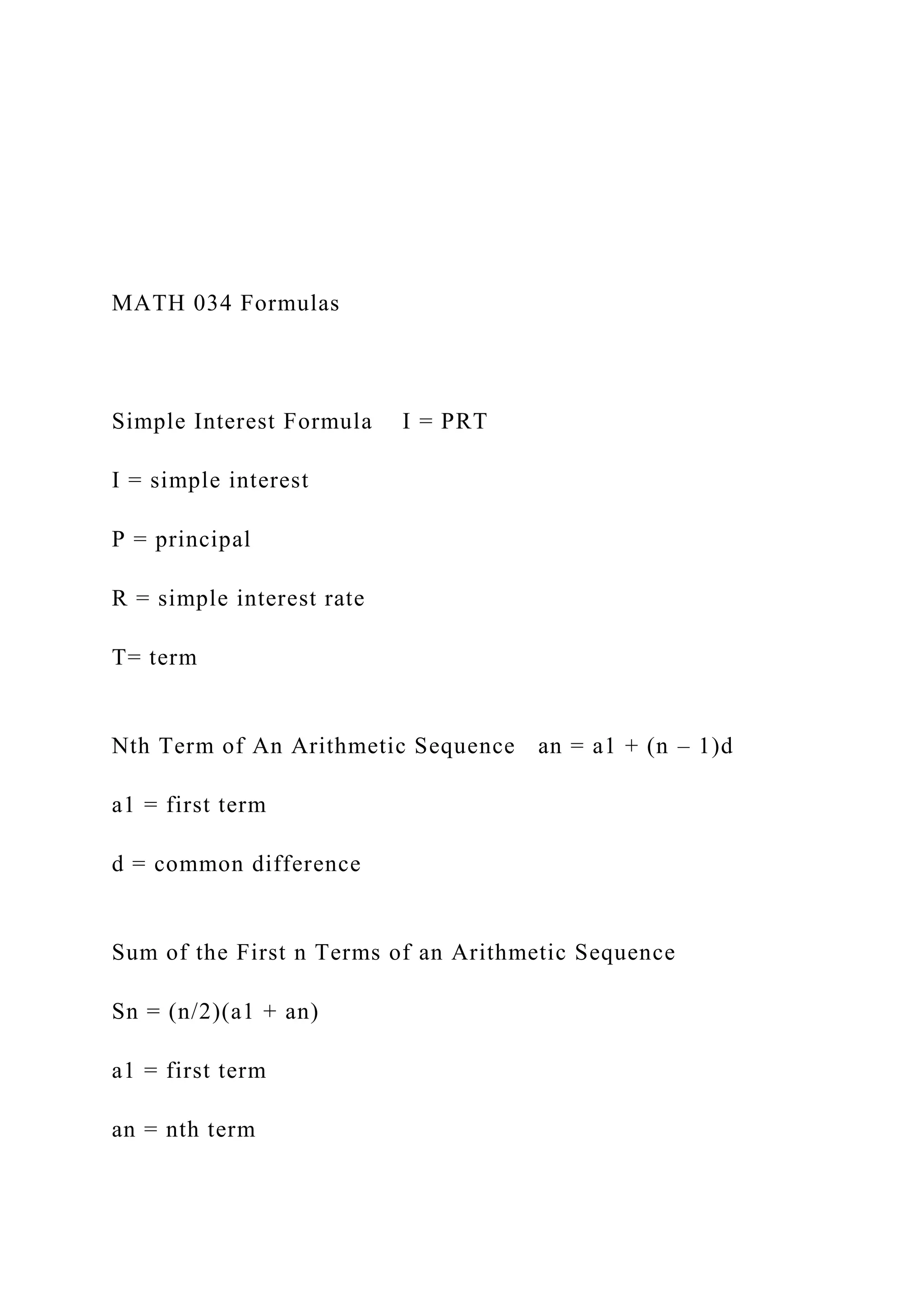

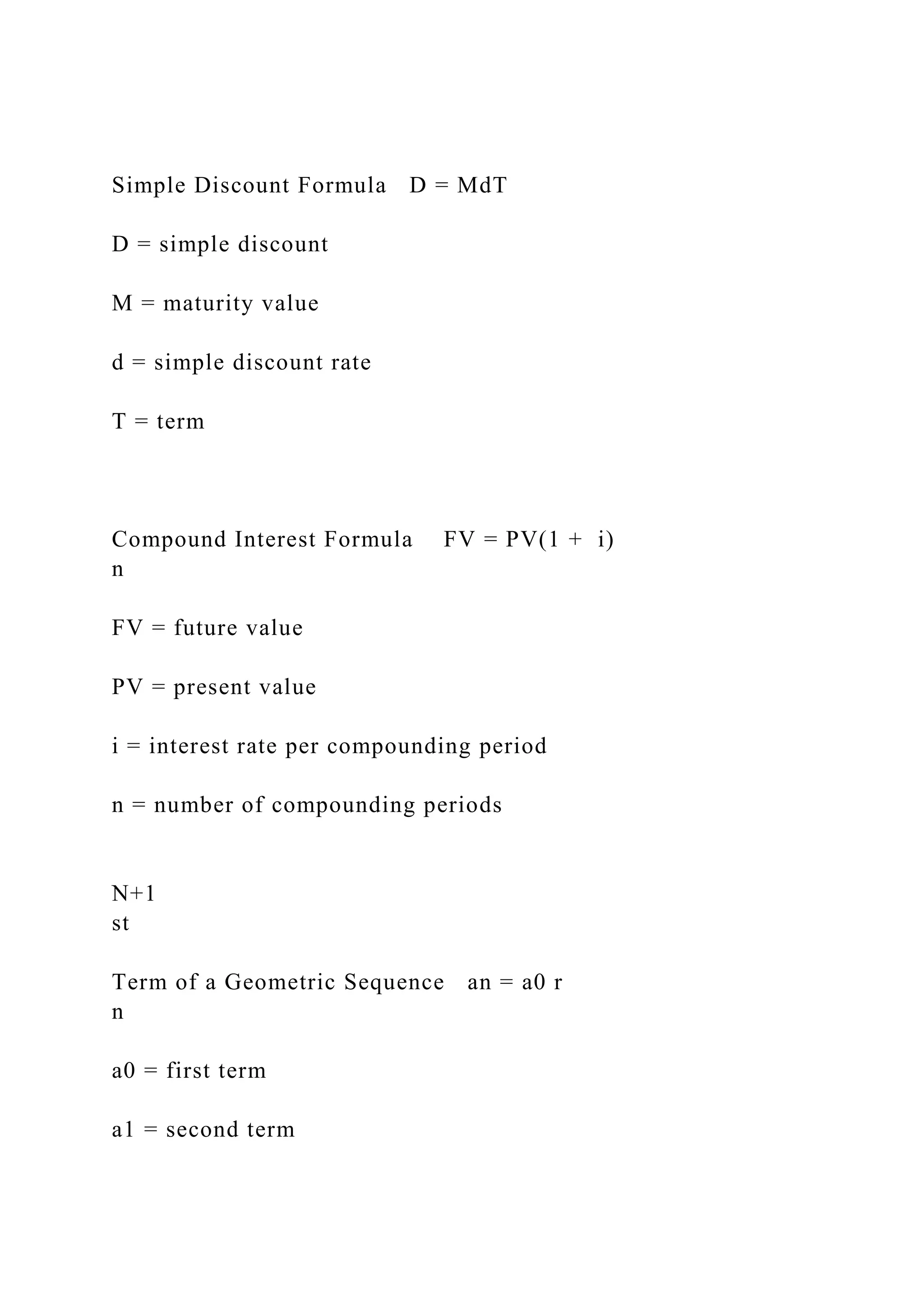

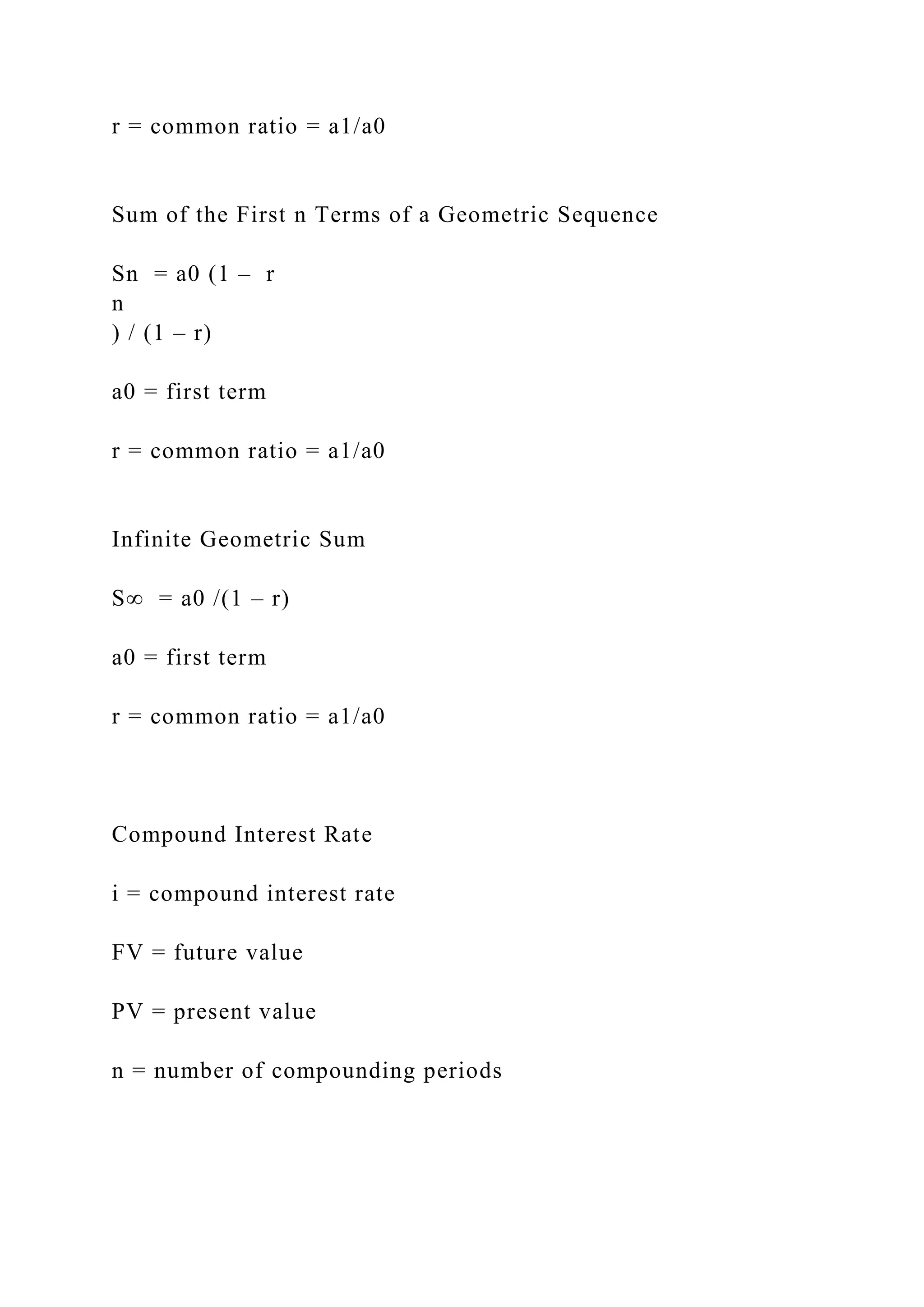

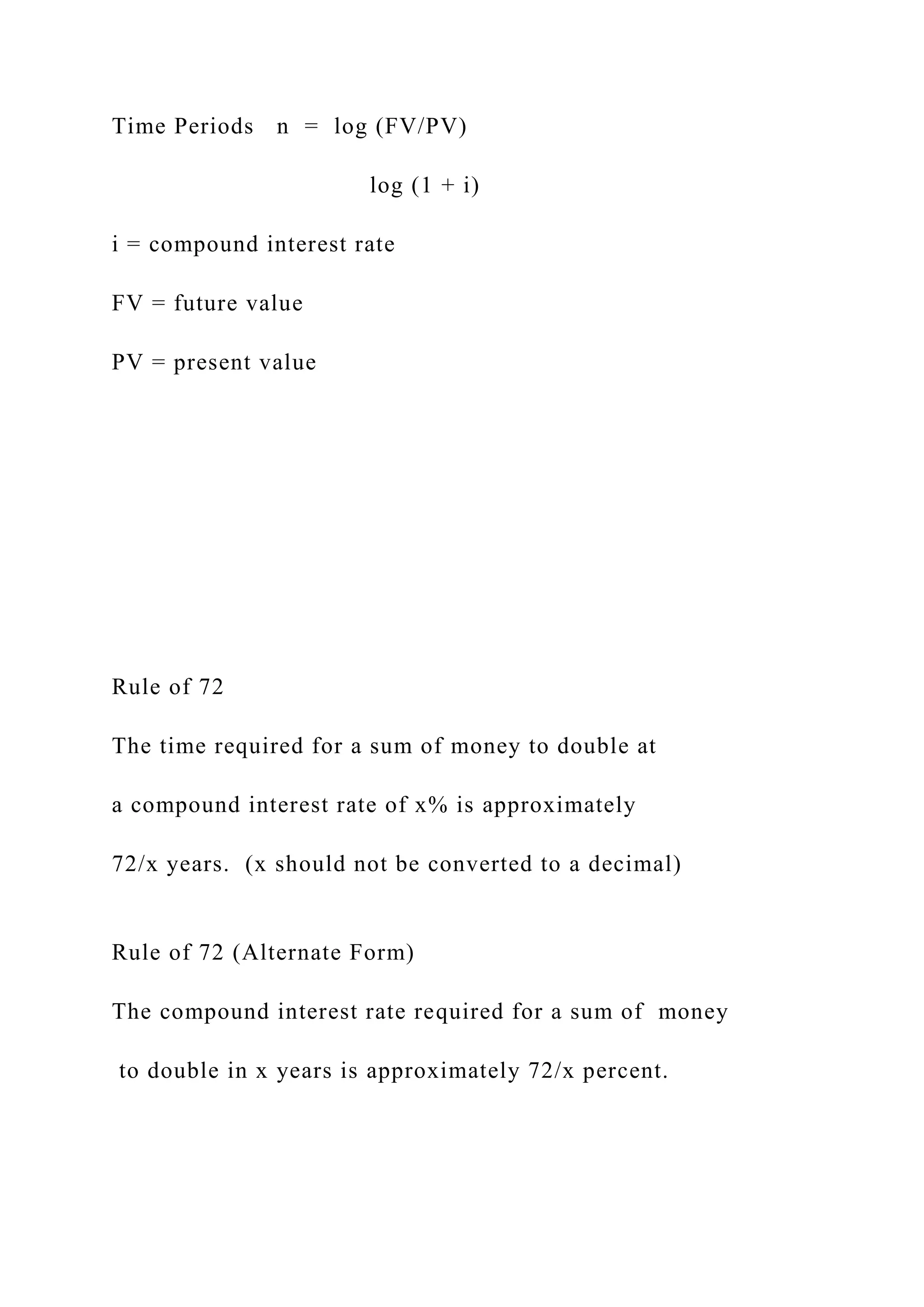

The document outlines various financial formulas related to interest, annuities, dividends, taxes, and depreciation. Key formulas include simple and compound interest calculations, present and future value of annuities, sales and income tax calculations, and methods for determining profit margins. It also features rules for evaluating investments such as the Rule of 72 and compound annual growth rates.