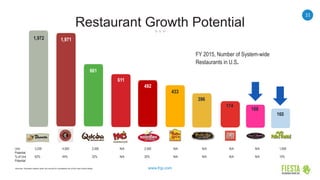

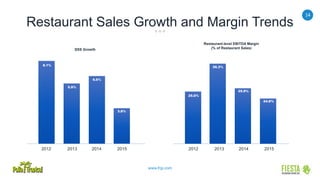

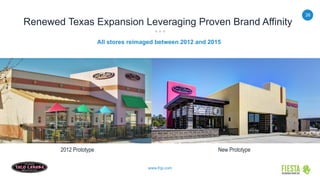

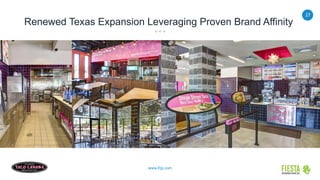

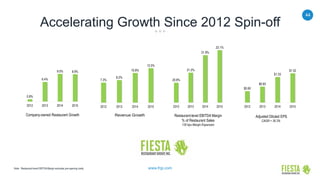

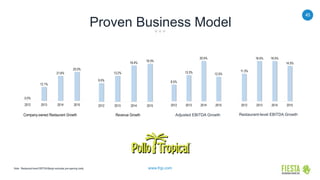

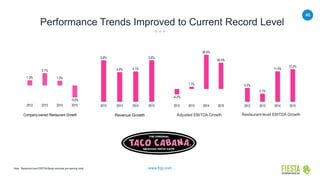

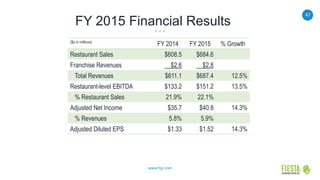

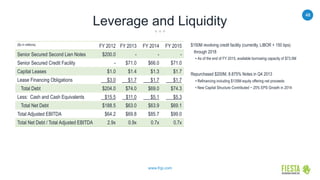

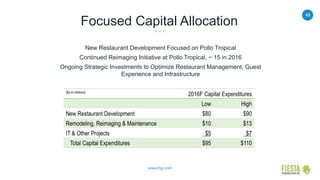

This document provides an overview of Fiesta Restaurant Group and its two brands, Pollo Tropical and Taco Cabana. It discusses Fiesta's growth strategies, including accelerating development of both brands and eventually separating the brands into independent companies. Financial information is presented showing strong sales and profit growth across both brands in recent years, with opportunities for further growth through new restaurant development and increased marketing investments.