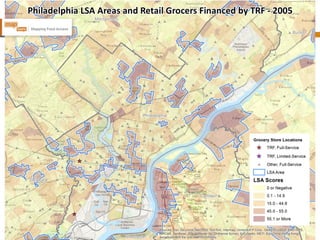

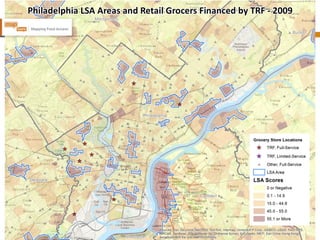

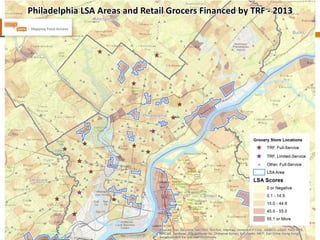

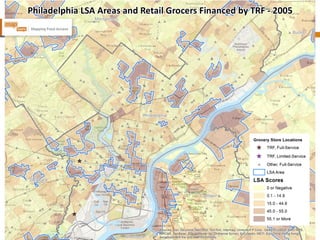

This document discusses TRF's use of spatial data and analysis to inform their supermarket financing initiatives. It provides background on TRF, describes their work related to limited supermarket access areas and healthy food financing, and outlines various analyses they conduct including leakage analysis, market structure analysis, and impact assessments. Key points include identifying areas lacking supermarket access, quantifying potential market viability, examining economic barriers to supermarket development, and measuring the economic impacts of new supermarket development.