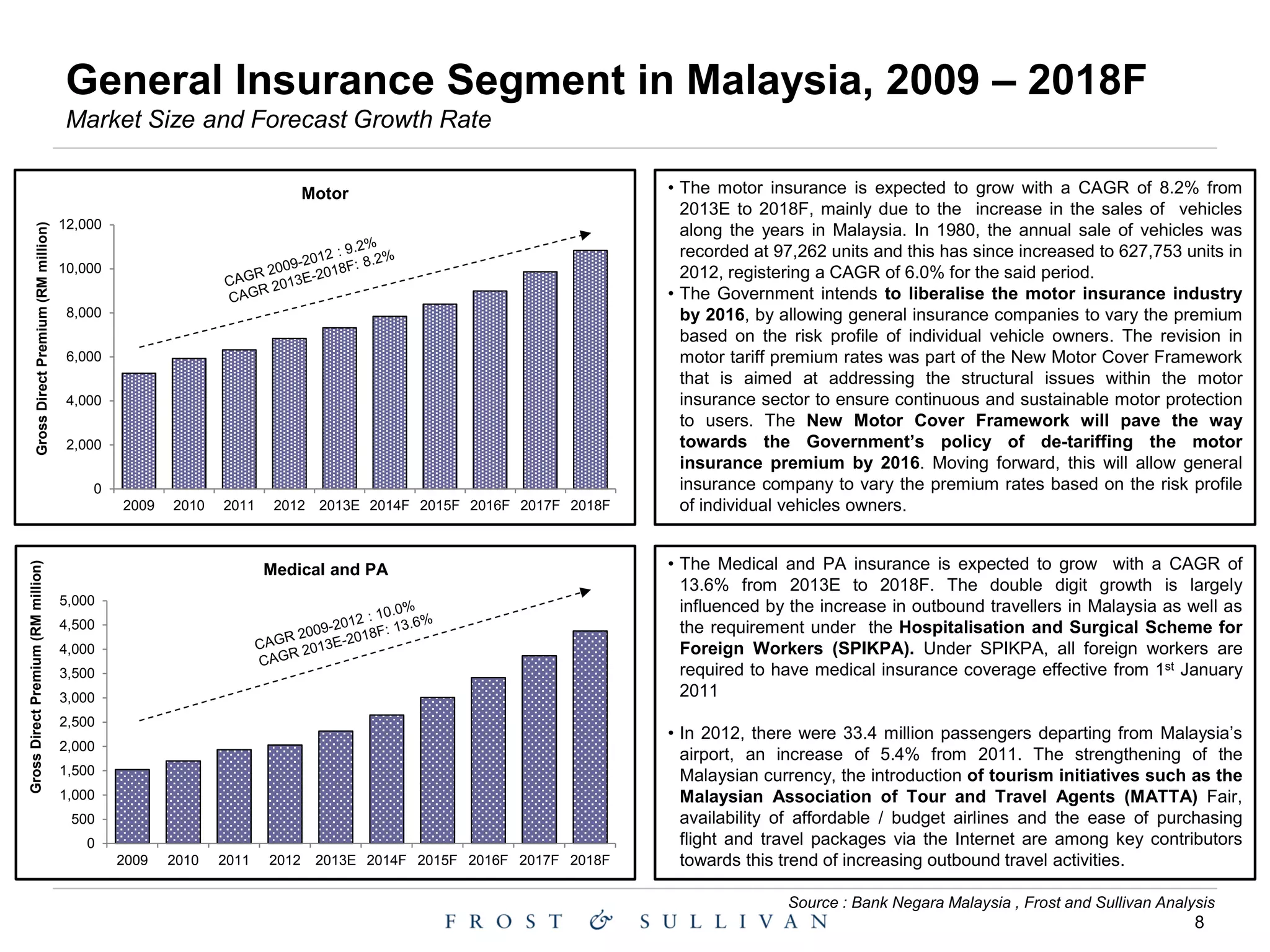

The document provides an overview of Malaysia's financial system and general insurance industry. It discusses the key regulatory bodies that oversee the financial system and categories financial institutions. It then summarizes the different segments of Malaysia's general insurance market, including motor, marine/aviation/transit (MAT), fire, medical/personal accident, and others. The motor segment is the largest, followed by fire. The document forecasts continued growth across all segments through 2018, especially in medical/personal accident, driven by factors like increasing travel and regulatory requirements for foreign worker insurance.