Good Stuff Happens in 1:1 Meetings: Why you need them and how to do them well

Lifting Cost Rig Count Oil1 (2) (4) (2)

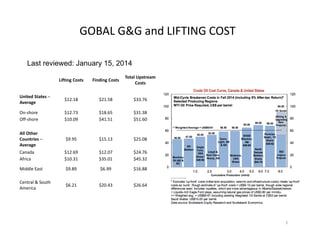

1. Lifting Costs Finding Costs

Total Upstream

Costs

United States –

Average

$12.18 $21.58 $33.76

On‐shore $12.73 $18.65 $31.38

Off‐shore $10.09 $41.51 $51.60

All Other

Countries –

Average

$9.95 $15.13 $25.08

Canada $12.69 $12.07 $24.76

Africa $10.31 $35.01 $45.32

Middle East $9.89 $6.99 $16.88

Central & South

America

$6.21 $20.43 $26.64

GOBAL G&G and LIFTING COST

Last reviewed: January 15, 2014

1

8. Costs

A major factor influencing the cost of extraction is the lifecycle of each type of oil source. Saudi wells last longer. There is more oil to pump within each cavity and so the cost of setting up that

well can be written off over a longer period than the cost of setting up a fracking and horizontal drilling operation. A long‐term producer can also write off the cost of distribution methods

over a longer period. So if a new well can be built alongside existing roads and pipelines, that method will end up cheaper in the long run than fracking in remote and previously unexplored

areas where a new pipeline or railroad infrastructure adds to setup costs.

Staff costs are higher with fracking methods because each drilling site is distant from earlier sites. Any oil extractor has to spend time and money locating staff for each project. Those

employees then need to be transported and housed. If a well lasts for decades, the same accommodation can be used for staff over a longer period than the short‐term nature of each fracking

location. The peripatetic nature of fracking also means that staff will be less likely to settle in one place with their families and therefore demand higher wages to compensate for the

loneliness of working away from home in freezing ‐40F North Dakota winters.

Capacity

Fracking is more expensive than extracting oil by conventional methods. Thus, conventional producers can afford to keep extracting and selling their oil at lower crude index prices than

frackers. So why bother investing in hydraulic fracturing and horizontal drilling? A high oil price offers an incentive to endeavor. American oil exploration and extraction companies would

much rather work in their own country, and in their own language, than have to travel to unstable places and risk hostile cultures in order to make a living. Thus, US oil companies expanded

production in their own county once prices reached a certain level where unconventional methods became economically viable. Financiers and investors had little risk of losing their

investment. The OPEC countries consistently trimmed their output to match world demand, so projections of oil prices and rates of return created a one‐way bet.

American oil producers could just keep increasing capacity infinitely (or so it seemed), because someone else would adjust their output to make room in the market. Prospects looked good for

expansion because cutbacks in OPEC production meant America could just keep taking a larger and larger share of the market.

Circumstances

The Saudis and their cheap‐oil Persian Gulf neighbors suddenly had enough of making room for American expansion. They knew that they had been obliging to other nations, but felt that they

had not been treated with the courtesies that they deserved. Saudi Arabia was particularly angry that America and its Western allies had failed to topple Bashar al‐Assad in Syria and they were

furious with Russia for blocking initial attempts to oust the Syrian president. The sudden return to market of Algeria, Libya and Iraq meant that OPEC began to overproduce. Under normal

circumstances, both this extra production and added capacity from fracking would have prompted the Saudis and their OPEC allies to reduce production to maintain price levels. This year, the

Saudis switched tactics and decided to defend their market share no matter where the price went.

Endgame

A falling oil price punishes Russia and brings economic realities to calculations over whether to invest in further oil exploration. Fortunately, this tactic is not the disaster it might at first seem.

The second part of any price calculation lies with demand for a product. At the same time that oil supply surged, demand for oil dropped. China maintained the illusion of growth over the past

year by over‐ordering raw materials. Now they need to absorb their stocks, which takes a large part of world demand for oil out of the market. Europe's growth is stuttering, removing more

demand. Economists calculate that for every 10% drop in the price of oil, the world's GDP will grow by 0.1%. Evidently, the current falls in oil price will eventually correct the lack of demand in

the market and supply and demand will return to equilibrium.

Pricing

Faced with lack of demand and falling prices, any business has three options: carry on regardless; reduce, or suspend production; or lower costs. Saudi Arabia chose option one. This strategy

relies on others either going out of business, or suspending operations to reduce supply. The Arabian producers can afford to pick that option because they have the lowest production costs

among all oil producers. According to Morgan Stanley Commodity Research, some Middle‐Eastern onshore production can break even at $10 per barrel. Others in that region need around $37

per barrel, with the average breakeven point for onshore wells in the Gulf states at around $27 per barrel. US shale oil doesn't start to pay back until it achieves a price of at least $50 per

barrel. Current production costs vary between that breakeven point and a price of $80 per barrel.

Long Term Effects

The depletion rate of fracked wells is high. Bakken production for any given fracked well declines 45 per cent per year, vs. 5 per cent per year for conventional wells. So after one year the

same well produces 55% of its initial output, after two years that reduces to 30%, and only 17% after 3 years. Producers need to keep drilling in order to stay in production with a steady flow

of oil. This series of wells at different levels of depletion in production by the same company is termed the "drilling treadmill."

Although in established fracking states, such as Texas, it takes only seven days to get permits to start extraction, production in other regions, less used to the process can entail months of

delays from legislators and pressure groups. Environmental restrictions placed on potential sites can pile on costs and make the benefits of extending the method into new locales a pricey

prospect. Unfortunately fracking companies have already exploited the easier, larger reserves. Since on average each new well has a fixed start up cost of around $9 million, regardless of how

much oil it will produce, further expansion of shale oil production will only break even north of the current $76‐$77 level.

When oil sold for $100 per barrel producers gained a margin of $23 per barrel after a cost of $77 per barrel for drilling the existing wells and operating them. That margin provided funding for

the "drilling treadmill" to create more wells. Therefore, although a falling price may not cause an immediate slow down in production, the disincentive of lower returns, longer delays and

uncertain rewards could discourage future development. The loss of a profit on sales means fracking companies no longer have money to keep drilling new wells. This would cause a reduction

in America's capacity to produce oil in the long term.

8