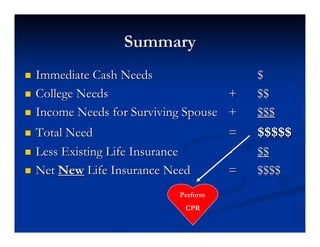

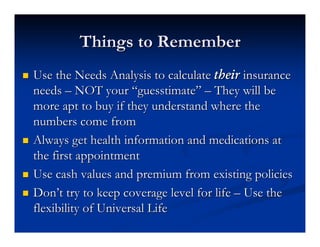

This document provides guidance on conducting a life insurance needs analysis for clients to determine the appropriate level of coverage. It outlines steps for gathering existing policy and beneficiary information, assessing immediate cash needs like debts and expenses, college funding needs over 18 years, and income needs for a surviving spouse. The needs analysis calculates totals that are then compared to existing coverage to determine the net new life insurance needed. It emphasizes using the needs analysis results, rather than estimates, to demonstrate coverage needs to clients and increase the likelihood of a sale.

![Financial Justification1 (4)[2]](https://cdn.slidesharecdn.com/ss_thumbnails/financialjustification142-123726082358-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)