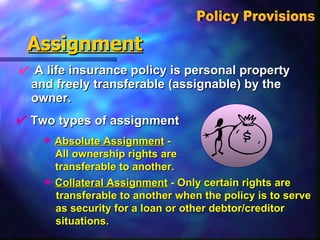

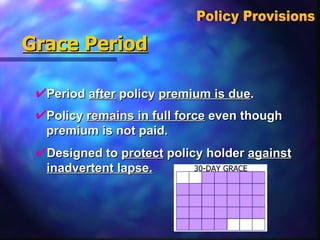

The document provides an overview of various life insurance policy provisions and options. It discusses topics like assignment of policies, grace periods, contestability periods, reinstatement clauses, beneficiary designations, cash surrender values, policy loans, policy riders, participating policies, settlement options, and more. The level of detail in the document is intended to educate insurance agents on the ins and outs of life insurance policies so they can effectively communicate options to clients.