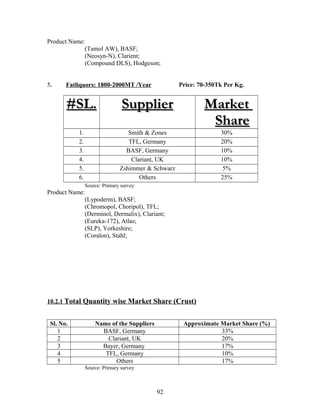

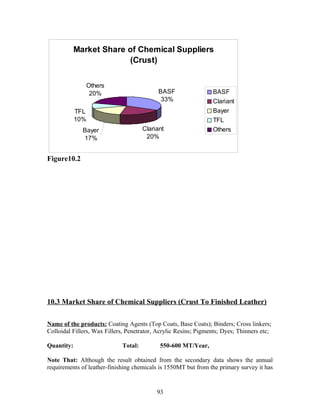

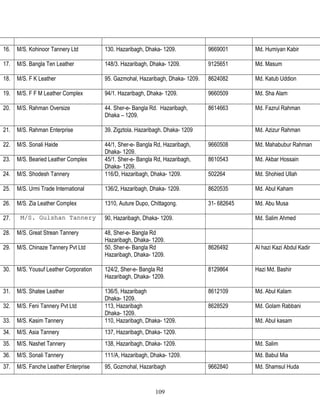

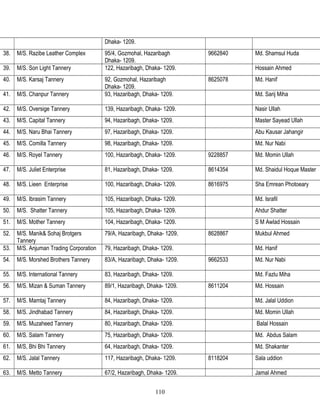

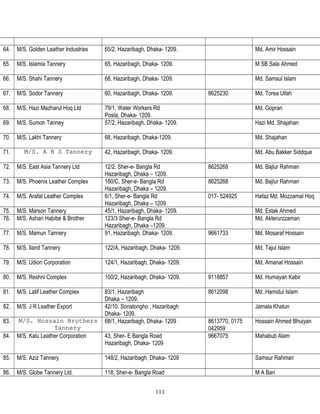

This document provides an overview of the leather industry in Bangladesh and the leather chemical industry. It discusses the history and current state of the leather industry in Bangladesh, production and exports of leather and leather goods. It also analyzes the raw materials used at different stages of leather processing as well as the major players in the leather chemical industry in Bangladesh and their market shares. The document is based on a study conducted by the author during their internship with ACI Trading Limited to understand the current market scenario and future prospects of the leather chemical industry in Bangladesh.