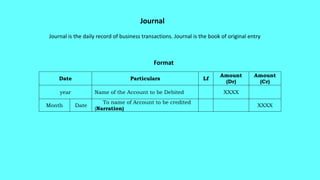

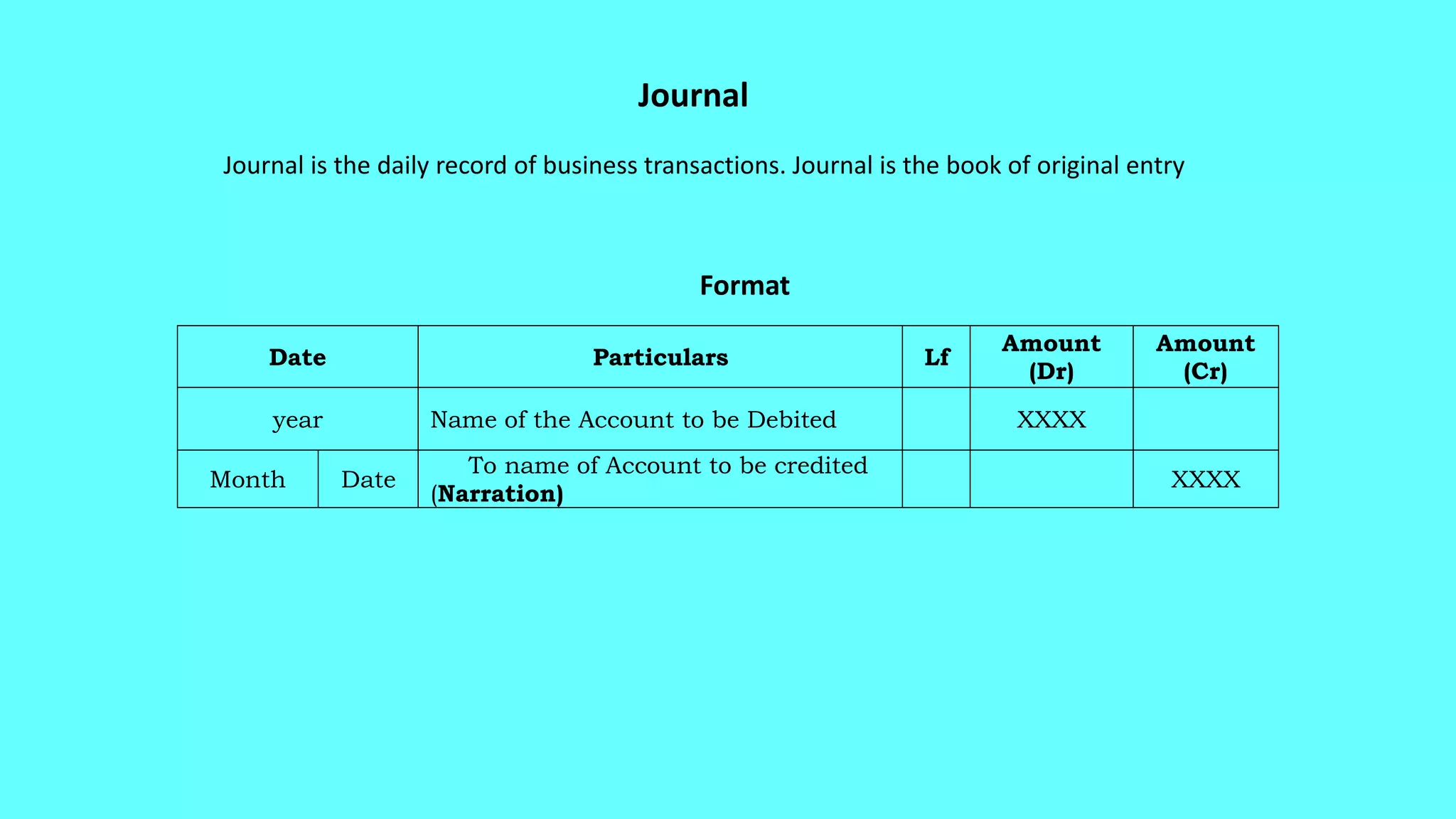

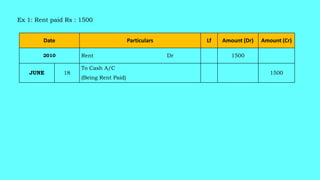

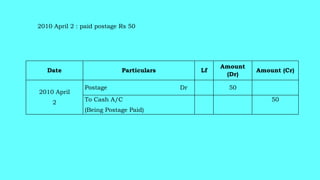

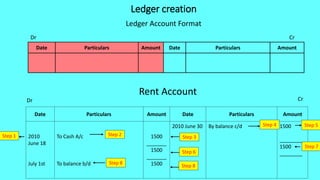

The document describes the format and purpose of a journal. A journal is used to record business transactions and is the book of original entry. It contains details of debits and credits including date, account name, amount, and narrative. Transactions are recorded in the journal by date in debit and credit columns. The journal entries are then posted or transferred to individual accounts in the ledger to track balances for each account.