Download to read offline

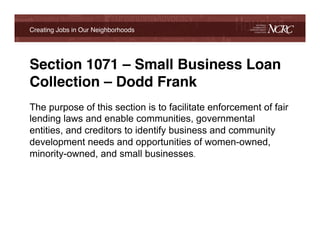

This document discusses the need for enhanced small business loan data collection. Currently, data is limited and does not include important demographic details about small business owners. The Dodd-Frank Act requires expanded data collection through Section 1071 to better identify credit needs, enforce fair lending laws, and help direct resources. The expanded data mandated by Dodd-Frank will include race, gender, business revenue size, loan details, and census tract information, helping analysts better assess if credit needs are being met for various small business owner groups.

![Selecciones voleibol juegos escolares 2011[1]](https://cdn.slidesharecdn.com/ss_thumbnails/seleccionesvoleiboljuegosescolares20111-111021130636-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)