The document discusses the Insurance Regulatory and Development Authority (IRDA) of India. Some key points:

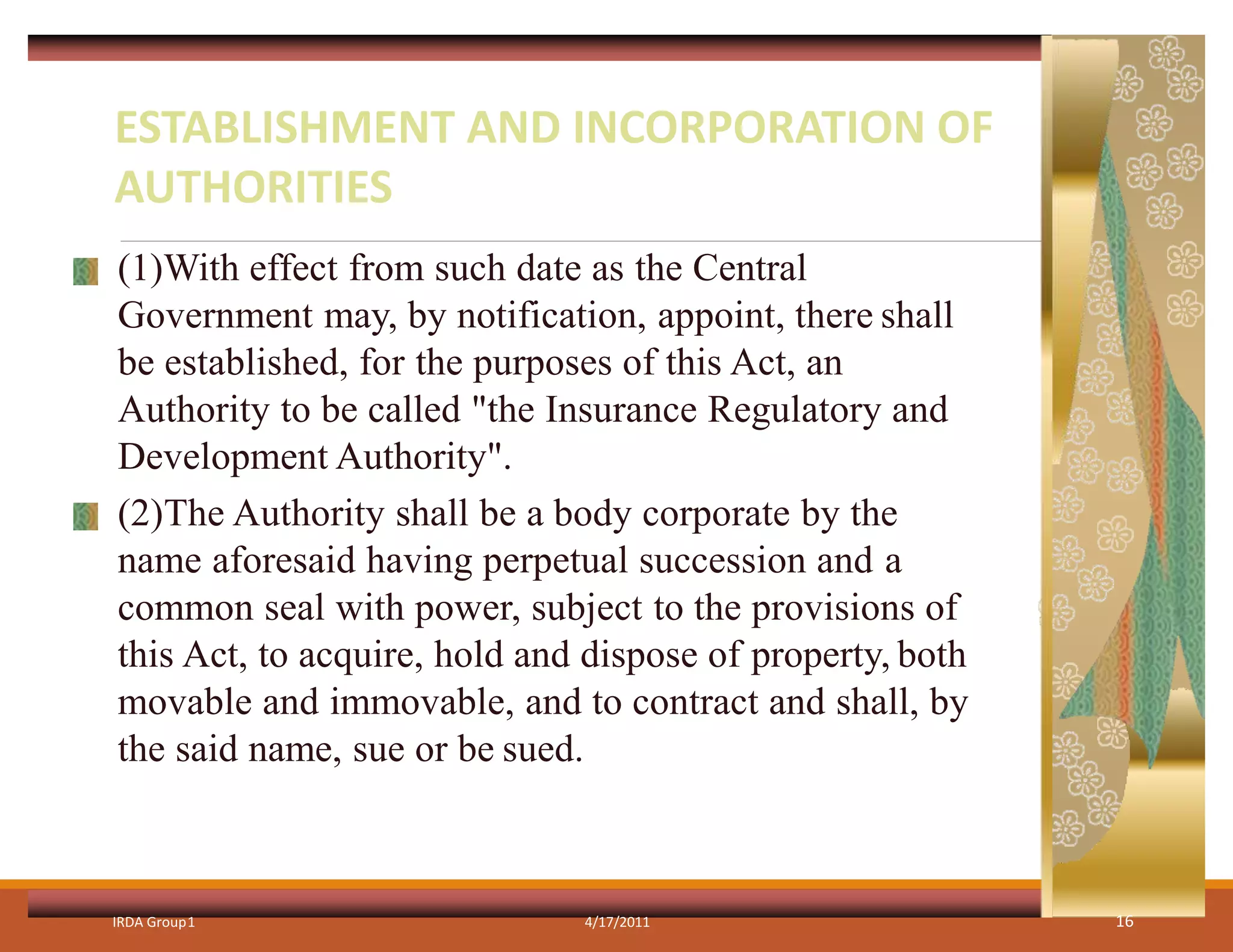

- IRDA is the national regulatory body for India's insurance industry, established by an act of Parliament in 1999.

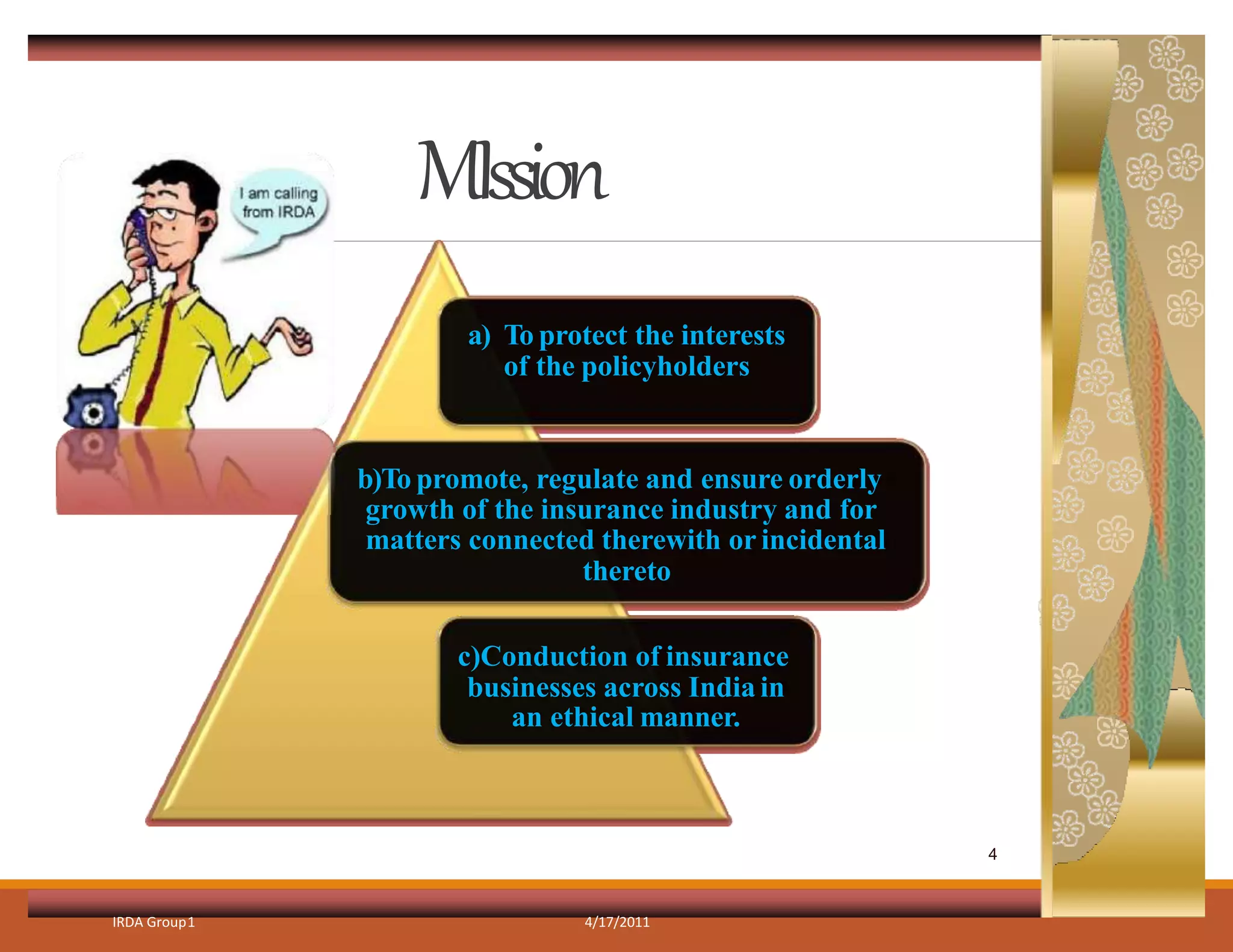

- Its mission is to protect policyholders' interests, promote and regulate the orderly growth of the insurance industry, and ensure insurance businesses operate ethically.

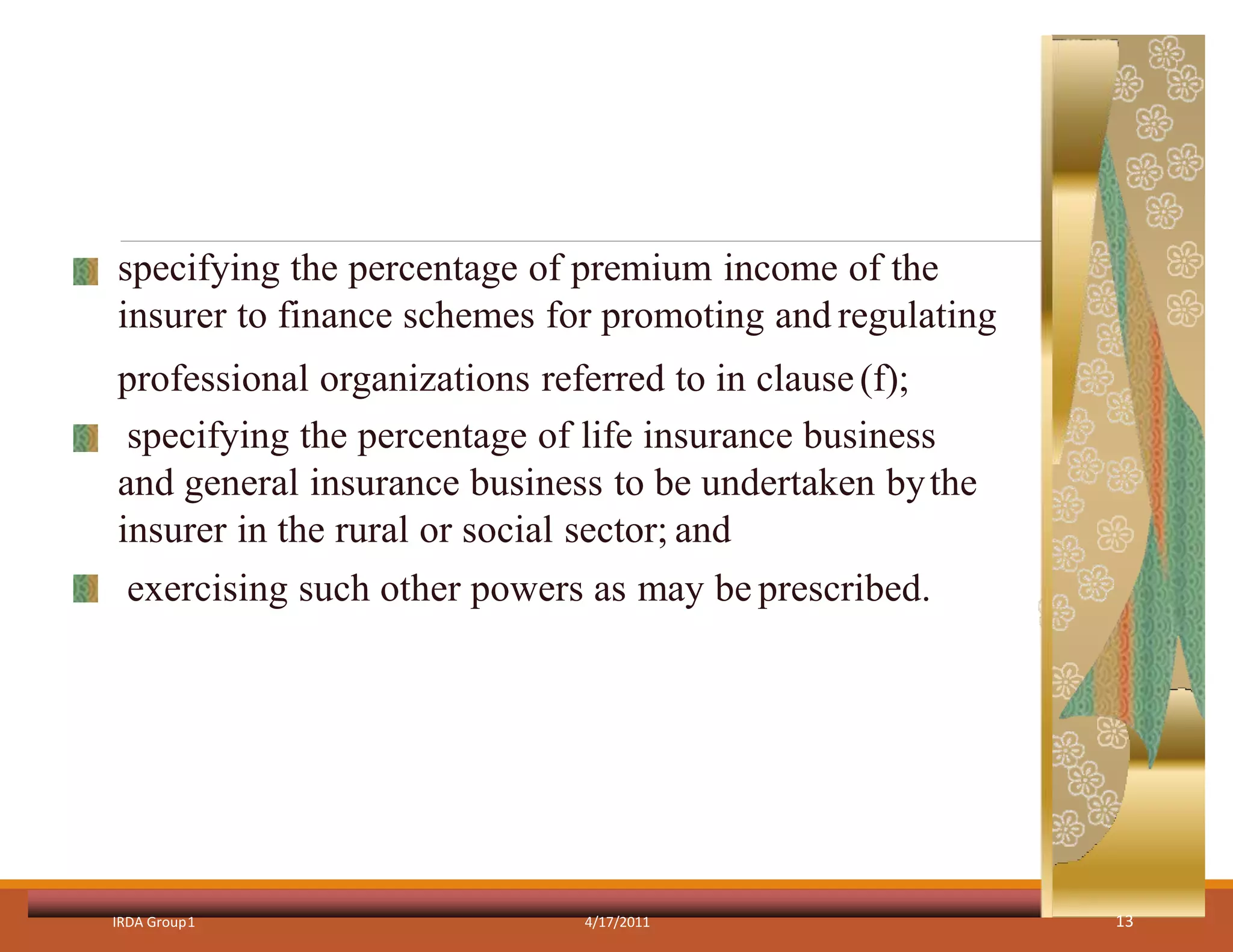

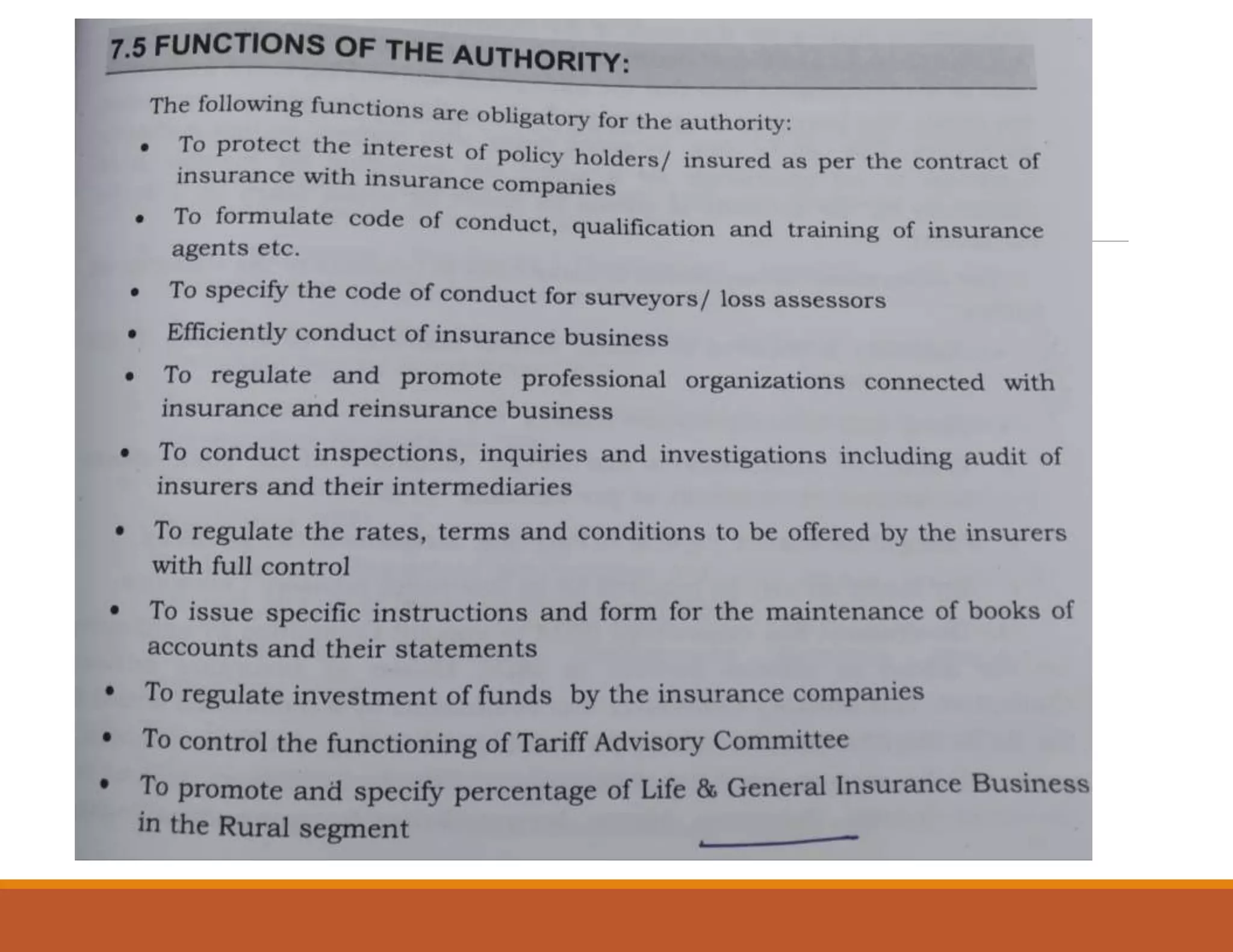

- IRDA has duties like protecting policyholders, promoting the industry's growth, enforcing high standards, and ensuring proper conduct in financial markets dealing with insurance.

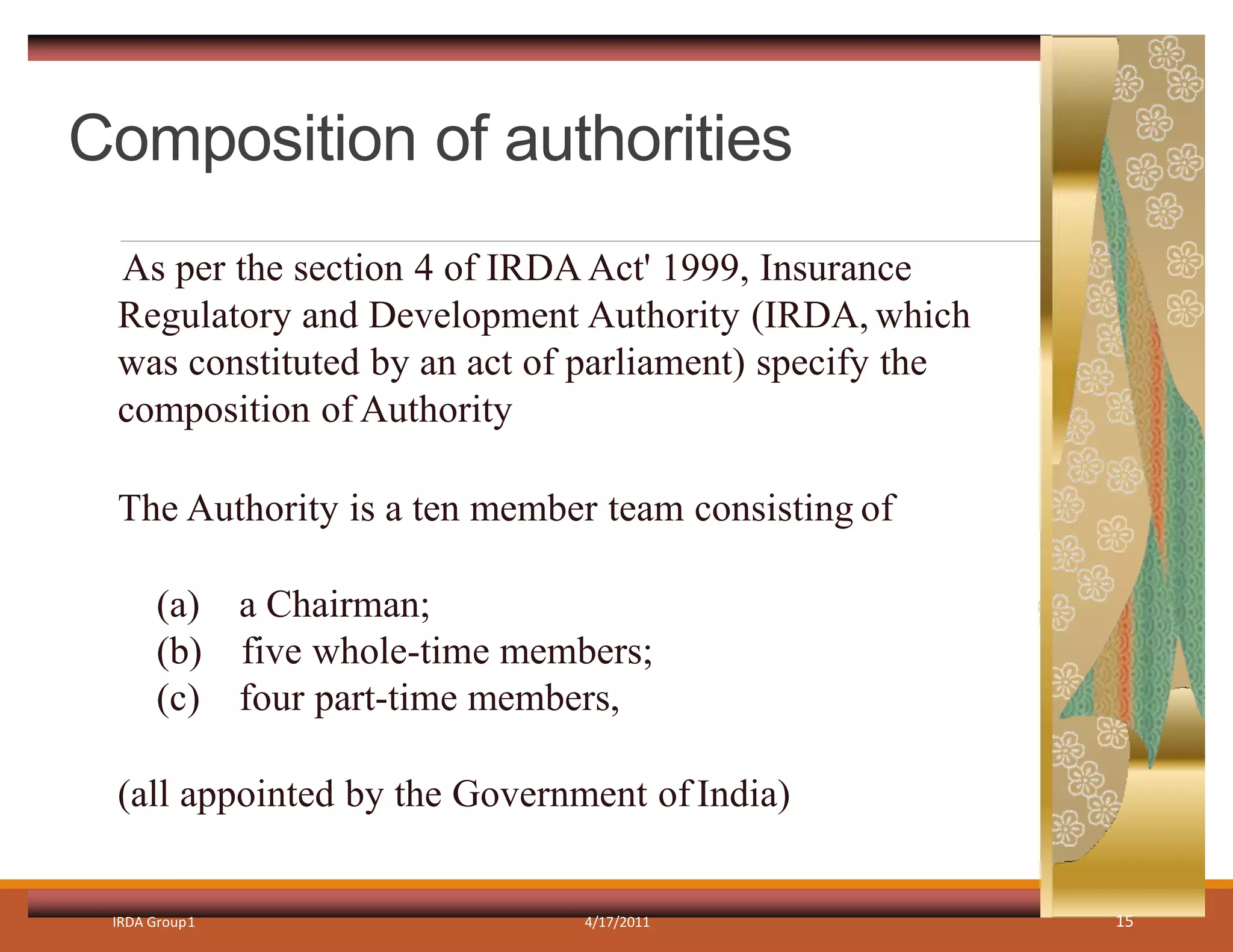

- It is composed of 10 members - a Chairman, 5 whole-time members, and 4 part-time members, all appointed by the Indian government.

![IRDA [Insurance Regulatory and Development Authority]](https://cdn.slidesharecdn.com/ss_thumbnails/ibegropu07-171025144708-thumbnail.jpg?width=640&height=640&fit=bounds)