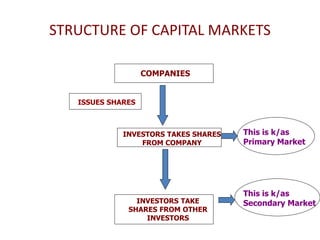

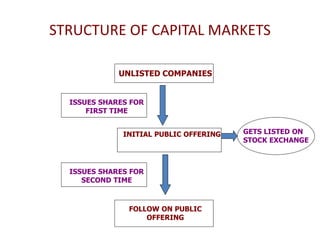

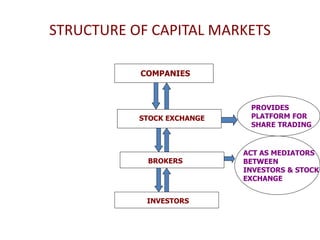

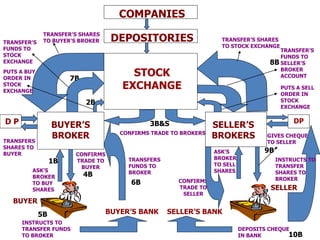

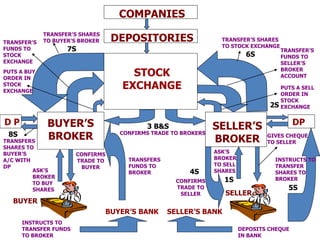

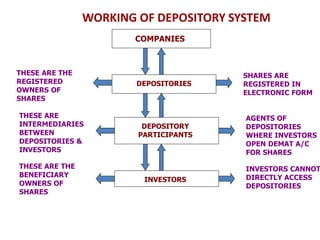

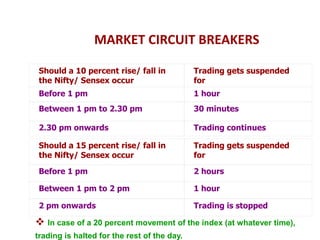

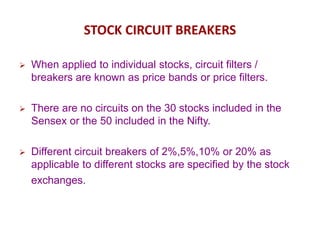

The document outlines the structure and functioning of capital markets, including primary and secondary markets, and the roles of various intermediaries such as brokers, depositories, and regulatory bodies like SEBI. It explains different types of public offerings, such as initial public offerings (IPOs) and rights issues, along with their procedures, benefits, and drawbacks for investors. Additionally, it covers market regulations, circuit breakers, and the process for trading in stocks.