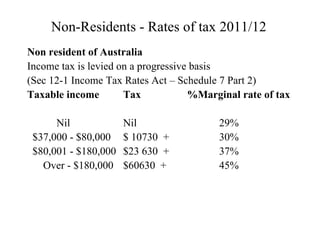

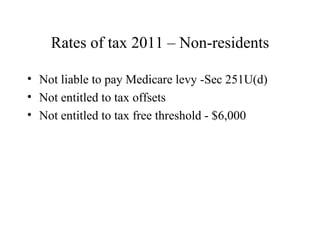

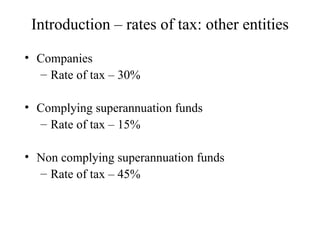

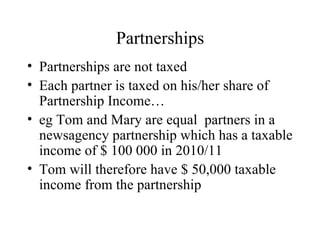

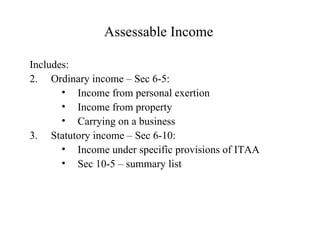

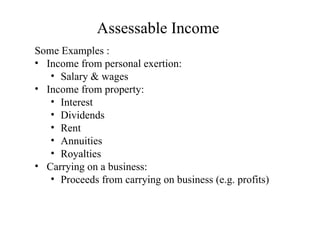

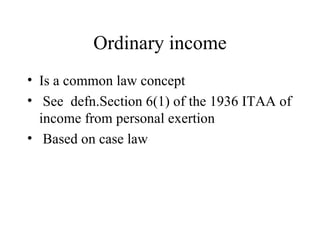

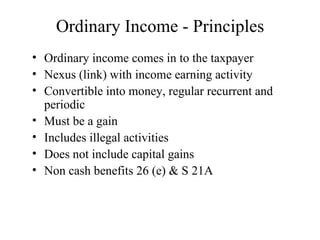

This document provides an overview and introduction to income tax concepts for the 2012 tax year. It covers topics such as taxation policy, authority in taxation law, tax reform, an overview of the Australian tax system, income tax rates for residents and non-residents, Medicare levy, tax offsets and rebates, taxable income calculation, and taxation of other entities like companies, trusts and partnerships.