[ARCHIVE] Infographic of the Aviva Real Retirement Report Summer 2012

•

0 likes•568 views

1. The document discusses finances for over-55s in the UK, including typical incomes, savings, debts, and home values. 2. Most over-55s rely on an employer pension (39%) and state pension (62%) for income, and have median savings of £15,756. Common debts include mortgages, personal loans, credit cards, and overdrafts. 3. The document recommends that people over 55 take the lead in getting financial advice as many employers provide little support for retirement planning. It also suggests considering reducing hours or working longer to ease the financial transition to retirement.

More Related Content

What's hot

What's hot (19)

More from Aviva plc

More from Aviva plc (20)

Recently uploaded

Recently uploaded (20)

[ARCHIVE] Infographic of the Aviva Real Retirement Report Summer 2012

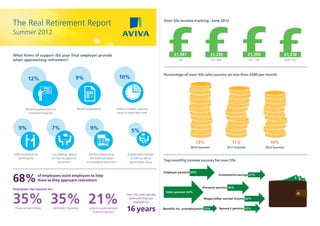

- 1. Finances of the Report The Real Retirement Over-55s income tracking - June 2012 typical modern Summer 2012 family What forms of support did your final employer provide £1,361 £1,359 £1,390 £1,318 when approaching retirement? All 55 – 64s 65 – 74s Over 75s Percentage of over-55s who survive on less than £500 per month 12% 9% 10% Workshops/Seminars on Benefit statements Ability to reduce working retirement finances hours or work flexi-time 9% 7% 9% 5% 12% 11% 10% 2010 Summer 2011 Summer 2012 Summer Offer to extend my Counselling / advice Written literature on A dedicated member working life on how to adjust to the financial issues of staff to talk to retirement surrounding retirement about these issues Top monthly income sources for over 55s Employer pension 39% 68% of employees want employers to help Investments/savings 27% £ £ them as they approach retirement £ Employees’ top requests are: Personal pension 34% 35% 35% 21% State pension 62% Over-55s have typically been with their last Wages/other earned income 32% employer for financial workshops retirement literature a list of recommended financial advisers 16 years Benefits inc. unemployment 17% Spouse’s pension 22%

- 2. Typical savings pots of the over-55s - June 2012 Debt by type of formal borrowing Hire Purchase Personal Loans Credit £2,802 Cards £26,085 £6,544 £3,470 £15,756 £12,998 £9,373 Storecards All over 55s 55-64 65-74 Over 75 Doorstep Overdraft lenders £766 Debt of those with a mortgage £846 £1,564 £223,958 £395,098 £208,398 £191,518 £87,500 £82,292 So what does this tell us? £70,000 £51,786 1. Take the lead in securing advice – With 64% of employers offering no additional or tailored support East London East Midlands West Midlands for employees approaching retirement, you can’t just rely on your workplace for help planning your later life finances. 2. Consider part-tirement – Some employers are happy to offer you assistance with planning your exit from £167,411 £178,779 £191,827 £316,827 work so consider whether you might want to work part-time or work beyond the traditional retirement age. 3. Look at the wider implications of stopping work – While retiring will mean a drop in income for most people, there are other implications. Will you lose your private medical insurance and therefore do you need £77,500 £47,794 £43,056 £78,040 to take out a private policy? North East North West Scotland South East 4. What borrowing do you have? – Entering retirement with significant debts, even if you have assets, is not ideal. Consider how you can use your assets to reduce your debts and therefore your monthly outgoings. £281,327 £191,389 £165,402 £236,474 In a rapidly changing world it makes sense to make the most of your retirement; to understand what you have, £70,000 £37,500 £45,833 £63,555 the options available and ensure you maximise your assets. South West Wales Yorkshire UK To find out how Aviva can help House Price Mortgage visit www.aviva.co.uk/retirement 106000692 07/2012 © Aviva plc