India's Index of Eight Core Industries Performance from June to November 2014

•Download as DOCX, PDF•

0 likes•619 views

#India’s Index of #EightCoreIndustries from June to November 2014 stands at 166.20 which is at +6.70% compared to the same period last year. #IndustrialIndex #IndiaIndustrialData #IndiaEconomicData #Coal #CoalProduction #CrudeOil #CrudeOilProduction #NaturalGas #NaturalGasProduction #PetroleumRefinery #PetroleumRefineryProduction #Fertilizers #FertilizersProduction #IndiaFertilizers #ChemicalFertilizers #IndiaSteelProduction #Steel #Cement #CementProduction #IndiaCement #IndiaEletricityGeneration #EnergyProduction #IndiaIndustrialProduction #IndustrialOutput #JhunjhunwalasFinance For more Informative post click : https://www.linkedin.com/company/jhunjhunwalas

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (13)

Similar to India's Index of Eight Core Industries Performance from June to November 2014

Similar to India's Index of Eight Core Industries Performance from June to November 2014 (19)

More from Jhunjhunwalas

More from Jhunjhunwalas (20)

Recently uploaded

Recently uploaded (20)

India's Index of Eight Core Industries Performance from June to November 2014

- 1. India’s Index of Eight Core Industries From June to November 2014

- 45. India’s Index of 8 Core Industry Performance from June to November 2014 #India #Index8CoreIndustry #8CoreIndustryIndex #Coal #CrudeOil #NaturalGas #PetroleumRefinaryProducts #Fertilizers #Steel #Cement #ElectricityGeneration #IndiaIndustrialProduction #IndiaIndustrialIndex For more Informative post click : https://www.linkedin.com/company/jhunjhunwalas

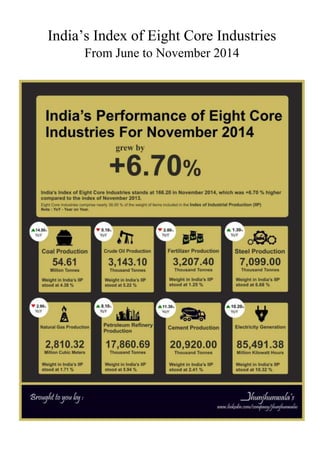

- 46. Press Release : 31st December 2014 Index of Eight Core Industries (Base: 2004-05=100), November, 2014 The summary of the Index of Eight Core Industries (base: 2004-05) is given at the Annexure. The Eight Core Industries comprise nearly 38 % of the weight of items included in the Index of Industrial Production (IIP). The combined Index of Eight Core Industries stands at 166.2 in November, 2014, which was 6.7 % higher compared to the index of November, 2013. Its cumulative growth during April to November, 2014-15 was 4.6 %. Coal Coal production (weight: 4.38 %) increased by 14.5 % in November, 2014 over November, 2013. Its cumulative index during April to November, 2014-15 increased by 9.4 % over corresponding period of previous year. Crude Oil Crude Oil production (weight: 5.22 %) declined by 0.1 % in November, 2014 over November, 2013. The cumulative index of Crude Oil during April to November, 2014-15 declined by 0.8 % over the corresponding period of previous year. Natural Gas The Natural Gas production (weight: 1.71 %) declined by 2.9 % in November, 2014 over November, 2013. Its cumulative index during April to November, 2014-15 declined by 5.3 % over the corresponding period of previous year. Refinery Products (0.93% of Crude Throughput) Petroleum refinery production (weight: 5.94%) increased by 8.1 % in November, 2014 over November, 2013. Its cumulative index during April to November, 2014-15 declined by 0.5 % over the corresponding period of previous year. Fertilizers Fertilizer production (weight: 1.25%) declined by 2.8 % in November, 2014 over November, 2013. Its cumulative index during April to November, 2014-15 declined by 1.3 % over the corresponding period of previous year. Steel (Alloy + Non-Alloy) Steel production (weight: 6.68%) increased by 1.3 % in November, 2014 over November, 2013. Its cumulative index during April to November, 2014-15 also increased by 2.2 % over the corresponding period of previous year. Cement Cement production (weight: 2.41%) increased by 11.3 % in November, 2014 over November, 2013. Its cumulative growth during April to November, 2014-15 was 8.5 % over the corresponding period of previous year.

- 47. Electricity Electricity generation (weight: 10.32%) increased by 10.2 % in November, 2014 over the period of November, 2013 and it registered a cumulative growth of 10.4 % during April to November, 2014-15 over the corresponding period of previous year. Note 1: Data are provisional. Revision has been made based on revised data obtained for corresponding month of previous year in respect of Coal, Crude Oil, Natural Gas, Refinery Product, Steel and Electricity. Accordingly, indices for the month November, 2013 have been revised. Note 2: Release of the index for December, 2014 will be on Monday, 02 February, 2015. Performance of Eight Core Industries , Yearly Index & Growth Rate Base Year: 2004-05=100 , (Weight in IIP: 37.90 %) Annexure INDEX Sector Weight 2009- 10 2010- 11 2011- 12 2012- 13 2013- 14 Apr- Nov 13- 14 Apr- Nov 14- 15 Coal 4.379 140 139.7 141.5 148.1 149.4 133.8 146.3 Crude Oil 5.216 99.1 111 112.1 111.4 111.2 111.1 110.2 Natural Gas 1.708 149.5 164.4 149.7 128.1 111.5 111.9 106 Refinery Products 5.939 125.9 129.7 133.7 172.5 175.1 174.4 173.5 Fertilizers 1.254 103.4 103.4 103.8 100.2 101.8 102.1 100.8 Steel 6.684 139.3 157.7 174 181.1 197.4 195.2 199.5 Cement 2.406 157.1 164.2 175.2 188.7 194.3 185.8 201.6 Electricity 10.316 130.8 138.1 149.3 155.3 164.3 163.2 180.3 Overall Index 37.903 129.9 138.4 145.3 154.7 160.3 157.1 164.4 #Refinery Products’ yearly growth rates of 2012-13 are not comparable with other years on account of inclusion of RIL (SEZ) production data since April, 2012.

- 48. Performance of Eight Core Industries, Monthly Index & Growth Rate Base Year: 2004-05=100, (Weight in IIP: 37.90 %) INDEX Sector Coal Crude Oil Natural Gas Refinery Products Fertilizers Steel Cement Electricity Overall Index Weight 4.379 5.216 1.708 5.939 1.254 6.684 2.406 10.316 37.903 Nov-13 152 111.1 109.4 167.7 107.4 193.3 171.4 158.5 155.7 Dec-13 170.1 115 113.4 175.9 110.2 199 203.3 168.1 165.6 Jan-14 178.7 115.1 116.1 176.9 104.2 201.2 215 169.8 168.2 Feb-14 165.1 103.5 104.2 169.6 97.9 192.5 200.2 155.1 156.7 Mar-14 208.3 112.1 108.8 183.8 92.1 214.2 226.2 172.9 175.4 Apr-14 140.5 109.6 104.7 165.8 87.4 192.8 217.5 176.9 160.9 May-14 145.2 111.6 111.2 171.6 100.5 214.3 216.4 183.2 168.7 Jun-14 139.2 110.4 109.4 173.3 99.5 196.1 209.7 181.5 163.9 Jul-14 134.9 111.1 103.5 170.8 102.5 200.4 206.9 182.8 163.9 Aug-14 138.6 106.8 103.1 175.1 105.7 209.3 187.7 183.6 165.1 Sep-14 140.1 107.5 102.6 169.7 101.1 197.4 198 175.3 160.6 Oct-14 158.2 113.6 107.2 180.5 105.1 189.8 185.9 184.1 165.9 Nov-14 174 111 106.2 181.3 104.4 195.8 190.8 174.6 166.2 GROWTH RATE (in %) Sector Coal Crude Oil Natural Gas Refinery Products Fertilizers Steel Cement Electricity Overall Index Weight 4.379 5.216 1.708 5.939 1.254 6.684 2.406 10.316 37.903 Nov-13 3.3 1.2 -11.2 -5.2 0.6 10.1 3.9 6.3 3.2 Dec-13 -0.6 1.6 -9.9 -1.7 4.1 3.1 1.1 6.7 2.1 Jan-14 -0.7 3 -5.2 -4.5 1.2 3.4 1.5 5.7 1.6 Feb-14 0.1 1.9 -4.4 3.2 -0.7 4.8 2.3 10.4 4.5 Mar-14 0.7 -1.6 -9.3 2.8 -6.1 5.4 0 5.4 2.5 Apr-14 3.3 -0.1 -7.7 -2.2 11.1 3.1 6.7 11.2 4.2 May-14 5.5 -0.3 -2.2 -2.3 17.6 -2 8.7 6.3 2.3 Jun-14 8.1 0.1 -1.7 1.2 -1 4.2 13.6 15.7 7.3 Jul-14 6.2 -1 -9 -5.5 -4.2 -3.4 16.5 11.2 2.7 Aug-14 13.4 -4.9 -8.3 -4.3 -4.3 9.1 10.3 12.6 5.8 Sep-14 7.2 -1.1 -6.2 -2.5 -11.6 4 3.2 3.8 1.9 Oct-14 16.2 1 -4.2 4.2 -7 2.3 -1 13.2 6.3 Nov-14 14.5 -0.1 -2.9 8.1 -2.8 1.3 11.3 10.2 6.7

- 49. Press Release : 1st December 2014 Index of Eight Core Industries (Base: 2004-05=100), October, 2014 The summary of the Index of Eight Core Industries (base: 2004-05) is given at the Annexure. The Eight Core Industries comprise nearly 38 % of the weight of items included in the Index of Industrial Production (IIP). The combined Index of Eight Core Industries stands at 165.9 in October, 2014, which was 6.3 % higher compared to the index of October, 2013. Its cumulative growth during April to October, 2014-15 was 4.3 %. Coal Coal production (weight: 4.38 %) increased by 16.2 % in October, 2014 over October, 2013. Its cumulative index during April to October, 2014-15 increased by 8.5 % over corresponding period of previous year. Crude Oil Crude Oil production (weight: 5.22 %) increased by 1.0 % in October, 2014 over October, 2013. The cumulative index of Crude Oil during April to October, 2014-15 declined by 0.9 % over the corresponding period of previous year. Natural Gas The Natural Gas production (weight: 1.71 %) declined by 4.2 % in October, 2014 over October, 2013. Its cumulative index during April to October, 2014-15 declined by 5.6 % over the corresponding period of previous year. Petroleum Refinery Products (0.93% of Crude Throughput)[1] Petroleum refinery production (weight: 5.94%) increased by 4.2 % in October, 2014 over October, 2013. Its cumulative index during April to October, 2014-15 declined by 1.7 % over the corresponding period of previous year.

- 50. Fertilizers Fertilizer production (weight: 1.25%) declined by 7.0 % in October, 2014 over October, 2013. Its cumulative index during April to October, 2014-15 declined by 1.1 % over the corresponding period of previous year. Steel (Alloy + Non-Alloy) Steel production (weight: 6.68%) increased by 2.3 % in October, 2014 over October, 2013. Its cumulative index during April to October, 2014-15 also increased by 2.3 % over the corresponding period of previous year. Cement Cement production (weight: 2.41%) declined by 1.0 % in October, 2014 over October, 2013. Its cumulative growth during April to October, 2014-15 was 8.1 % over the corresponding period of previous year. Electricity Electricity generation (weight: 10.32%) increased by 13.2 % in October, 2014 over the period of October, 2013 and it registered a cumulative growth of 10.5 % during April to October, 2014-15 over the corresponding period of previous year. Note: Data are provisional. Revision has been made based on revised data obtained for corresponding month of previous year in respect of Coal, Crude Oil, Natural Gas, Refinery Product, Steel, Cement and Electricity.

- 51. Performance of Eight Core Industries Yearly Index & Growth Rate Base Year: 2004-05=100 (Weight in IIP: 37.90 %) INDEX Sector Weight 2009-10 2010-11 2011-12 2012-13 2013-14 Apr-Oct 13-14 Apr-Oct 14-15 Coal 4.379 140.0 139.7 141.5 148.1 149.3 131.2 142.4 Crude Oil 5.216 99.1 111.0 112.1 111.4 111.2 111.1 110.1 Natural Gas 1.708 149.5 164.4 149.7 128.1 111.5 112.3 106.0 Refinery Products 5.939 125.9 129.7 133.7 172.5 175.1 175.3 172.4 Fertilizers 1.254 103.4 103.4 103.8 100.2 101.8 101.4 100.3 Steel 6.684 139.3 157.7 174.0 181.1 196.5 195.5 200.0 Cement 2.406 157.1 164.2 175.2 188.7 194.3 187.9 203.1 Electricity 10.316 130.8 138.1 149.3 155.3 164.3 163.9 181.1 Overall Index 37.903 129.9 138.4 145.3 154.7 160.1 157.3 164.2 GROWTH RATE (in %) Sector Weight 2009-10 2010-11 2011-12 2012-13 2013-14 Apr-Oct 13-14 Apr-Oct 14-15 Coal 4.379 8.1 -0.2 1.3 4.6 0.8 1.3 8.5 Crude Oil 5.216 0.5 11.9 1.0 -0.6 -0.2 -1.2 -0.9 Natural Gas 1.708 44.6 10.0 -8.9 -14.5 -13.0 -16.1 -5.6 Refinery Products 5.939 -0.4 3.0 3.1 29.0# 1.6 3.5 -1.7 Fertilizers 1.254 12.7 0.0 0.4 -3.4 1.5 2.7 -1.1 Steel 6.684 6.0 13.2 10.3 4.1 8.5 11.9 2.3 Cement 2.406 10.5 4.5 6.7 7.7 3.0 4.0 8.1 Electricity 10.316 6.2 5.6 8.1 4.0 5.8 5.1 10.5 Overall Index 37.903 6.6 6.6 5.0 6.5 3.5 4.2 4.3

- 52. #Refinery Products’ yearly growth rates of 2012-13 are not comparable with other years on account of inclusion of RIL (SEZ) production data since April, 2012. Performance of Eight Core Industries Monthly Index & Growth Rate Base Year: 2004-05=100 (Weight in IIP: 37.90 %) Sector Coal Crude Oil Natural Gas Refinery Products Fertilizers Steel Cement Electricity Overall Index Weight 4.379 5.216 1.708 5.939 1.254 6.684 2.406 10.316 37.903 Oct-13 -3.5 -0.6 -13.5 -5 4.1 5.8 0.9 1.3 -0.1 Nov-13 2.3 1.1 -11.3 -5 0.6 3.9 4.2 5.9 1.7 Dec-13 -0.6 1.6 -9.9 -1.7 4.1 3.1 1.1 6.7 2.1 Jan-14 -0.7 3 -5.2 -4.5 1.2 3.4 1.5 5.7 1.6 Feb-14 0.1 1.9 -4.4 3.2 -0.7 4.8 2.3 10.4 4.5 Mar-14 0.7 -1.6 -9.3 2.8 -6.1 5.4 0 5.4 2.5 Sector Coal Crude Oil Natural Gas Refinery Products Fertilizers Steel Cement Electricity Overall Index Weight 4.379 5.216 1.708 5.939 1.254 6.684 2.406 10.316 37.903 Oct-13 136.1 112.5 112 173.1 113 185.6 187.9 162.5 156 Nov-13 150.5 110.9 109.3 168.1 107.4 182.5 172 157.8 153.5 Dec-13 170.1 115 113.4 175.9 110.2 199 203.3 168.1 165.6 Jan-14 178.7 115.1 116.1 176.9 104.2 201.2 215 169.8 168.2 Feb-14 165.1 103.5 104.2 169.6 97.9 192.5 200.2 155.1 156.7 Mar-14 208.3 112.1 108.8 183.8 92.1 214.2 226.2 172.9 175.4 Apr-14 140.5 109.6 104.7 165.8 87.4 192.8 217.5 176.9 160.9 May-14 145.2 111.6 111.2 171.6 100.5 214.3 216.4 183.2 168.7 Jun-14 139.2 110.4 109.4 173.3 99.5 196.1 209.7 181.5 163.9 Jul-14 134.9 111.1 103.5 170.8 102.5 200.4 206.9 182.8 163.9 Aug-14 138.6 106.8 103.1 175.1 105.7 209.3 187.7 183.6 165.1 Sep-14 140.1 107.5 102.6 169.7 101.1 197.4 198 175.3 160.6 Oct-14 158.2 113.6 107.2 180.5 105.1 189.8 185.9 184.1 165.9

- 53. Apr-14 3.3 -0.1 -7.7 -2.2 11.1 3.1 6.7 11.2 4.2 May-14 5.5 -0.3 -2.2 -2.3 17.6 -2 8.7 6.3 2.3 Jun-14 8.1 0.1 -1.7 1.2 -1 4.2 13.6 15.7 7.3 Jul-14 6.2 -1 -9 -5.5 -4.2 -3.4 16.5 11.2 2.7 Aug-14 13.4 -4.9 -8.3 -4.3 -4.3 9.1 10.3 12.6 5.8 Sep-14 7.2 -1.1 -6.2 -2.5 -11.6 4 3.2 3.8 1.9 Oct-14 16.2 1 -4.2 4.2 -7 2.3 -1 13.2 6.3 Index of Eight Core Industries (Base: 2004-05=100), September, 2014 The summary of the Index of Eight Core Industries (base: 2004-05) is given at the Annexure. Dated : 31-October, 2014 17:00 IST The Eight Core Industries comprise nearly 38% of the weight of items included in the Index of Industrial Production (IIP). The combined Index of Eight Core Industries stands at 160.6 in September, 2014, which was 1.9 % higher compared to the index of September, 2013. Its cumulative growth during April to September, 2014-15 was 4.0 %. Coal Coal production (weight: 4.38 %) increased by 7.2 % in September, 2014 over September, 2013. Its cumulative index during April to September, 2014-15 increased by 7.2 % over corresponding period of previous year. Crude Oil Crude Oil production (weight: 5.22 %) declined by 1.1 % in September, 2014 over September, 2013. The cumulative index of Crude Oil during April to September, 2014-15 declined by 1.2 % over the corresponding period of previous year. Natural Gas The Natural Gas production (weight: 1.71 %) declined by 6.2 % in September, 2014 over September, 2013. Its cumulative index during April to September, 2014-15 declined by 5.9 % over the corresponding period of previous year.

- 54. Petroleum Refinery Products (0.93% of Crude Throughput)[1] Petroleum refinery production (weight: 5.94%) declined by 2.5 % in September, 2014 over September, 2013. Its cumulative index during April to September, 2014-15 declined by 2.6 % over the corresponding period of previous year. India’s Index of #8CoreIndustry Performance from June to October 2014 #India #Index8CoreIndustry #8CoreIndustryIndex #Coal #CrudeOil #NaturalGas #PetroleumRefinaryProducts #Fertilizers #Steel #Cement #ElectricityGeneration #IndiaIndustrialProduction #IndiaIndustrialIndex For more Informative post click : https://www.linkedin.com/company/jhunjhunwalas

- 55. Fertilizers Fertilizer production (weight: 1.25%) declined by 11.6 % in September, 2014 over September, 2013. While, it registered no growth during April to September, 2014-15 over the corresponding period of previous year. Steel (Alloy + Non-Alloy) Steel production (weight: 6.68%) increased by 4.0 % in September, 2014 over September, 2013. Its cumulative index during April to September, 2014-15 increased by 2.3 % over the corresponding period of previous year. Cement Cement production (weight: 2.41%) increased by 3.2 % in September, 2014 over September, 2013. Its cumulative growth during April to September, 2014-15 was 9.7 % over the corresponding period of previous year. Electricity Electricity generation (weight: 10.32%) increased by 3.8 % in September, 2014 over the period of September, 2013 and it registered a cumulative growth of 10.0 % during April to September, 2014-15 over the corresponding period of previous year. Note: Data are provisional. Revision has been made based on revised data obtained for corresponding month of previous year in respect of Coal, Crude Oil, Natural Gas, Refinery Product, Steel and Electricity.

- 56. The summary of the Index of Eight Core Industries (base: 2004-05) is given at the Annexure. Date : 30th August 2014 The Eight Core Industries comprise nearly 38% of the weight of items included in the Index of Industrial Production (IIP). The combined Index of Eight Core Industries stands at 165.1 in August, 2014, which was 5.8 % higher compared to the index of August, 2013. Its cumulative growth during April to August, 2014-15 was 4.4 %. 1. Coal Coal production (weight: 4.38 %) increased by 13.4 % in August, 2014 over August, 2013. Its cumulative index during April to August, 2014-15 increased by 7.2 % over corresponding period of previous year. 2. Crude Oil Crude Oil production (weight: 5.22 %) declined by 4.9 % in August, 2014 over August, 2013. The cumulative index of Crude Oil during April to August, 2014-15 declined by 1.2 % over the corresponding period of previous year. 3. Natural Gas The Natural Gas production (weight: 1.71 %) declined by 8.3 % in August, 2014 over August, 2013. Its cumulative index during April to August, 2014-15 declined by 5.8 % over the corresponding period of previous year. 4. Petroleum Refinery Products (0.93% of Crude Throughput) Petroleum refinery production (weight: 5.94%) declined by 4.3 % in August, 2014 over August, 2013. Its cumulative index during April to August, 2014-15 declined by 2.7 % over the corresponding period of previous year. 5. Fertilizers Fertilizer production (weight: 1.25%) declined by 4.3 % in August, 2014 over August, 2013. While, it registered a cumulative growth of 2.8 % during April to August, 2014-15 over the corresponding period of previous year. 6. Steel (Alloy + Non-Alloy)

- 57. Steel production (weight: 6.68%) increased by 9.1 % in August, 2014 over August, 2013. Its cumulative index during April to August, 2014-15 increased by 2.0 % over the corresponding period of previous year. 7. Cement Cement production (weight: 2.41%) increased by 10.3 % in August, 2014 over August, 2013. Its cumulative growth during April to August, 2014-15 was 11.0 % over the corresponding period of previous year. 8. Electricity Electricity generation (weight: 10.32%) increased by 12.6 % in August, 2014 over the period of August, 2013 and it registered a cumulative growth of 11.3 % during April to August, 2014-15 over the corresponding period of previous year. Note: Data are provisional. Revision has been made based on revised data obtained for corresponding month of previous year in respect of Coal, Crude Oil, Natural Gas, Refinery Product, Steel and Electricity