CONTENTS

• Indian economy

•History of the Indian economy

• Indian economy after independence

• Economy after the changes in 1991

• Future of the Indian economy

• Challenges to the growth of the Indian

economy

• conclusion

3.

INDIAN ECONOMY

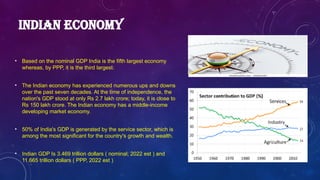

• Basedon the nominal GDP India is the fifth largest economy

whereas, by PPP, it is the third largest.

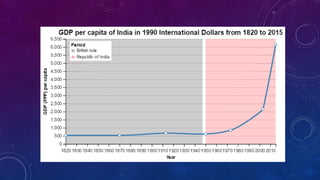

• The Indian economy has experienced numerous ups and downs

over the past seven decades. At the time of independence, the

nation's GDP stood at only Rs 2.7 lakh crore; today, it is close to

Rs 150 lakh crore. The Indian economy has a middle-income

developing market economy.

• 50% of India's GDP is generated by the service sector, which is

among the most significant for the country's growth and wealth.

• Indian GDP Is 3.469 trillion dollars ( nominal; 2022 est ) and

11.665 trillion dollars ( PPP, 2022 est )

4.

HISTORY OF THEINDIAN ECONOMY ( PRE COLONIAL)

• India's economic history can be characterized as spanning from the Indus valley civilization until 1700

AD.

• Indian economy at this time was very advanced. With the rest of the world, it has excellent trade

relations.

• When India gained its independence in 1947, its GDP had fallen to 2% from its peak of 25% to 35%

between the years of one AD and 1000 AD.

5.

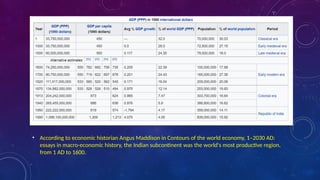

• According toeconomic historian Angus Maddison in Contours of the world economy, 1–2030 AD:

essays in macro-economic history, the Indian subcontinent was the world's most productive region,

from 1 AD to 1600.

6.

INDIAN ECONOMY AFTERINDEPENDENCE ( POST-COLONIAL )

• India’s economic policy after independence was

influenced by the colonial experience.

• The Industrial Policy Resolution of 1948 proposed a

mixed economy.

• India set up the Planning Commission in 1950 in

order to oversee the entire range of planning,

including resource allocation, implementation, and

appraisal of five-year plans.

• From the 50s to the 91, several industries, and

companies were nationalized by the government.

• License raj system and excessive state control

resulted in slow economic growth in the post-

colonial timeline.

8.

THE ECONOMIC REFORMSOF 1991

• Economic liberalisation in India was initiated in 1991 by Prime Minister P.

V. Narasimha Rao and his then-Finance Minister Dr. Manmohan Singh.

• The reforms did away with the Licence Raj, reduced tariffs and interest

rates and ended many public monopolies, allowing automatic approval of

foreign direct investment in many sectors.

• By the turn of the 21st century, India had progressed towards a free-

market economy, with a substantial reduction in state control of the

economy and increased financial liberalisation.

9.

FUTURE OF THEINDIAN ECONOMY

• India is already the fastest-growing economy in the world, having

clocked 5.5% average gross domestic product growth over the

past decade.

• India may become the third-largest economy by 2030 overtaking

Japan and Germany. S&P’s forecast is based on the projection

that India's annual nominal gross domestic product growth will

average 6.3% through 2030.

• In a recent Morgan Stanley Research blue paper, analysts from

various sectors examine how this new phase of economic

development may result in a number of startling changes,

including increasing credit availability, increasing India's share of

global manufacturing, promoting the growth of new businesses,

enhancing quality of life, and causing a huge rise in consumer

spending in the years to come.

• Over this time, shares of international exports may also double,

and the Bombay Stock Exchange may have 11% annual growth,

resulting in a market valuation of $10 trillion in the next ten

years.

10.

CHALLENGES TO THEGROWTH OF INDIAN

ECONOMY

• Low level of national income and per capita income.

• Vast inequalities in wealth and income.

• The predominance of agriculture.

• Tremendous population pressure.

• Massive unemployment.