Impact SPACS Facts Figures Part 1 .pdf

•

0 likes•81 views

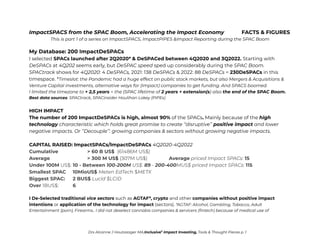

I selected 200 #ImpactSPACs and #DeSPACs from 4Q2020 to 4Q2022. The #SPACBoom. Affordable public equity <10US$ listed on US stockmarkets. Almost 90% holdpromise of postive impact eg #Electrification #Biotech #Sustainability #ESG. I added #PIPEs as a catalyst for impact investing. <60B US$ Almost as much as raised with SPAC IPOs. > 60B US$ I looked at present yields (ignoring maturity), impact themes invbestor presentations, company websites ESG rating & recommendations. Next Thought Piece will be on their Impact reporting: best practive. preferred metrics and more.

Recommended

Recommended

More Related Content

Similar to Impact SPACS Facts Figures Part 1 .pdf

Similar to Impact SPACS Facts Figures Part 1 .pdf (20)

More from Drs Alcanne Houtzaager MA

More from Drs Alcanne Houtzaager MA (20)

Recently uploaded

Recently uploaded (20)

Impact SPACS Facts Figures Part 1 .pdf

- 1. ImpactSPACS from the SPAC Boom, Accelerating the Impact Economy FACTS & FIGURES This is part 1 of a series on ImpactSPACS, ImpactPIPES &Impact Reporting during the SPAC Boom My Database: 200 ImpactDeSPACs I selected SPACs launched after 2Q2020* & DeSPACed between 4Q2020 and 3Q2022. Starting with DeSPACs at 4Q202 seems early, but DeSPAC speed sped up considerably during the SPAC Boom. SPACtrack shows for 4Q2020: 4 DeSPACs, 2021: 138 DeSPACs & 2022: 88 DeSPACs = 230DeSPACs in this timespace. *Timeslot: the Pandemic had a huge effect on public stock markets, but also Mergers & Acquisitions & Venture Capital investments, alternative ways for (Impact) companies to get funding. And SPACS boomed. I limited the timezone to + 2,5 years = the (SPAC lifetime of 2 years + extension(s) also the end of the SPAC Boom. Best data sources: SPACtrack, SPACinsider Houlihan Lokey (PIPEs) HIGH IMPACT The number of 200 ImpactDeSPACs is high, almost 90% of the SPACs. Mainly because of the high technology characteristic which holds great promise to create ‘’disruptive’’ positive impact and lower negative impacts. Or ‘’Decouple’’: growing companies & sectors without growing negative impacts. CAPITAL RAISED: ImpactSPACs/ImpactDeSPACs 4Q2020-4Q2022 Cumulative > 60 B US$ (61486M US$) Average > 300 M US$ (307M US$) Average priced Impact SPACs: 15 Under 100M US$: 10 - Between 100-200M US$: 89 - 200-400MUS$ priced Impact SPACs: 115 Smallest SPAC 10MioUS$ Meten EdTech $METX Biggest SPAC: 2 BUS$ Lucid $LCID Over 1BUS$: 6 I De-Selected traditional vice sectors such as AGTAF*, crypto and other companies without positive impact intentions or application of the technology for impact (sectors). *AGTAF: Alcohol, Gambling, Tobacco, Adult Entertainment (porn), Firearms.. I did not deselect cannabis companies & servicers (fintech) because of medical use of Drs Alcanne J Houtzaager MA,Inclusive2 Impact Investing, Tools & Thought Pieces p. 1

- 2. sometimes diversified suppliers, so including recreational, & purposeful (?) cannabis use. Neither did I deselect Defense suppliers because of the state of the world and actions & threats of autocratic regimes. Nor did I deselect technology serving negative/no net impact sectors as long as they offered sustainability & serving (high) impact sectors e.g. agriculture, security ‘solutions’.’ #Transition & #Mission (without Drift please….) Impact Intended SPACs: New were impact target themes such as ESG/Sustainability, Decarbonization. Already present before the Boom was Electrification: Electric Vehicles 2,4, 6-8 wheels, batteries, charging, storage, metals: mining & recycling. Always a strong presence has Life Science, Health including biotech, medical care & platformtech connecting carergivers & clients. Wow: AI as foundation for new treatments for ADHD, Dementia, Depression,COVID fog…. Many SPAC launchers kept their ‘options open’ naming multiple themes. Of course some themes are combined in one company: electrification requires metals (mining) but combined with recollecting, recycling & reusing is also a Sustainable company. Better care: outcomes, patient satisfaction, at lower cost and larger scale and professionals back up & support definately meets impact intended criteria. Impact Investing CATALYST: Private Investment in Public Equity 200 ImpactSPACs DeSPACed with ImpactPIPEs commitment, to be precise 226 PIPEs, so a few multiple PIPEs. PIPEs make up the complete merger deal amount. PIPEs are made by larger, institutional, investors and based on more information (Lazard) than eg in the merger investor presentation. 4 ImpactSPACs DeSPACed without a PIPE. 5% Best source Houlihan Lokey PIPE report 2020-21 & online search. 220 ImpactPIPE Deals Cumulative < 60BillionUS$ (58017MUS$) Average > 200MioUS$ (207MUS$) Average priced Impact SPACs: 18 Under 100M US$: 58 Between 100-200M US$: 114 Between 201-400MUS$ priced Impact SPACs: 52 Drs Alcanne J Houtzaager MA,Inclusive2 Impact Investing, Tools & Thought Pieces p. 2

- 3. >1B US$ ImpactPIPEs: 10 Biggest 2 BUS$ GRAB Holdings (Mobility, Delivery, Finance) $GRAB Smallest 6 MioUS$ Clever Leaves (Med. Canabis) $CVLR >20 ImpactSPACs with 1, or 3: $AEVA & $LFG ImpactPIPEs ImpactSPAC & ImpactPIPE size EQUAL Size ImpactPIPE US$ size = ImpactSPAC US$ size: 4 <2% LARGER Size Impact PIPES US$ size > ImpactSPAC US$ size: 30 13% of 226 PIPEs 12 serial SPAC launchers. 40% of 30 MUCH LARGER sized ImpactPIPE, in Millions US$ or Double x2 than the ImpacSPAC 18 8% (of 226 PIPEs) Of which 12 serial SPAC launchers. 66% of 18 Triple, Quadruple sized ImpactPIPEs 3x (2) & 4x (4) larger than the ImpactSPAC 6 <3% All serial SPAC launchers 100% ImpactPIPES size smaller than ImpactSPAC size make up the rest about 140. Since many DeSPACs did poorly some received further PIPE investments PROFITABLE ImpactDeSPACS (2021 data, Yahoo Finance) 21 ImpactDeSPACS 10% No Dividend payment (YF) yet Listing can be inspired by the ambition to acquirefunds to buy/acquire companies to add marketshare, revenues, e.g. a competitor, supplier, distrubutor or invest in growth: capacity, manufacturing, staff etc… Drs Alcanne J Houtzaager MA,Inclusive2 Impact Investing, Tools & Thought Pieces p. 3

- 4. 130 LOSSMAKING ImpactDeSPACs 37 with little revenues compared to losses (2021 YF) 93 with serious revenues compared to losses (2021 YF) 5 losses about the same amount as revenues CASHBURNERS no Revenues (2021 YF) 35 of which 17 biotech/therapies and 2 other medical services 20 Not yet reporting: recently listed DeSPACS, foreign, in trouble 2 Delisted. Bankrupt, Acquired EXCHANGE RATES of ImpactDeSPACs* 90% of researched SPACs universe Average* <4 US$ (3,60 US$). High 52 weeks >40US$ (41,11 US$) 52 Lows <4 US$ (3,79 US$) WINNERS recent data 34 US$ $MP Material corp Rare earth Mining in California, USA. Rated Severe (Operational) Risk by Sustaialytics. 29 US$ $CERE, Clinical stage therapies for neuroscience diseases 26 US$ $LFG Archaea Energy,a renewable natural gas (RNG) & renewable electricity producer in USA. Rated Medium (Operational) Risk by Sustainalytics. (ESG Research transparent company database, sector reports) BEST PERFORMERS recent data > 10US$ 9 < 9 US$ 4 < 8 US$ 6 MEDIOCRE* < 7 US$ 7 < 6 US$ 5 AVERAGE DeSPAC loss 33%* Harvard Law research into 48 pre Boom DeSPAC IPOs focusing on costs & short term returns A sober look at SPACs (Nov 2020). Klausner, Ohlrogge, Ruan https://corpgov.law.harvard.edu/2020/11/19/a-sober-look-at-spacs/ Drs Alcanne J Houtzaager MA,Inclusive2 Impact Investing, Tools & Thought Pieces p. 4

- 5. OUCH* < 5 US$ 16 < 4 US$ 17 < 3 US$ 37 < 2 US$ 36 < 1 US$ 35 2 DeSPACs Delisted & 1 because it was acquired itself. *These Exchange rates vary in maturity, some ImpactDeSPACs listed late 2020 almost 24 months and some just recently. Present exchange rates have changed ↑&↓ as I dont have access to up to date collected from September to mid November. Noet that penny stock > 5US$ is extra volatile. PREMLIMINARY THOUGHTS As ImpactDeSPACs are 90% of the DeSPAC universe, poor yields are hardly surprising. It would be unnerving to know,conclude that ImpactDeSPACS perform worse than Net negative of Non Impact DeSPAC. Or because (De)SPACs as an investment got a bad wrap. #yield #reputation NOAC Natural order AC seeking a plant based food company just redeemed my shares explaining their reason of which c) is ‘’the volatility in capital markets and in deSPAC transactions, which dissuaded good companies from accessing the markets’. Worse if speculants have targetted the SPAC universe due to its accessible price range and thus destroyed value of Impact Companies or halting, stunting their growth. Missed opportunities for technology advancement in Electrification, LifeScience sector and exciting niche sector success. Especially as most ImpactDeSPAC companies’ websites & Investor Presentations show legacy industry, sector leaders support: backing them as investors, partners, clients etc. Investing in innovation, boosting impact in the supply chain. And Shareholder profiles show large percentages of institutional investors (SimplyWallstreet) The tech crackdown, geopolitical turmoil caused by totalitarian regimes and the War against Ukraine and populist anti Woke/ESG sentiment have not helped stock markets and certainly Growth Stock.. Questions & Comments are Welcome Drs Alcanne J Houtzaager MA,Inclusive2 Impact Investing, Tools & Thought Pieces p. 5

- 6. Next thought Piece I will look at the Impact Ambitions & Reporting of Impact DeSPACs. Some great Best Practice exemplary companies publish Global Impact Reports, tailored (per) Global Goal contributions, great ESG performance & ambitions (reports), SASB sector Material Sustainability issues, prioritised in Materiality Matrices, Carbon Disclosure emissions saved! (E :), SWOTs, Underserved Populations, Market potential… Sometimes a pay off says it all. Tip: Often company website Career pages share their culture of Diversity, Equality & Inclusion with employee blogs/experiences, celebrations… Questions & Comments are Welcome Please connect through https://www.linkedin.com/in/alcannehoutzaager Drs Alcanne J Houtzaager MA,Inclusive2 Impact Investing, Tools & Thought Pieces p. 6