Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Similar to IMO 2020

Similar to IMO 2020 (20)

Recently uploaded

Recently uploaded (20)

IMO 2020

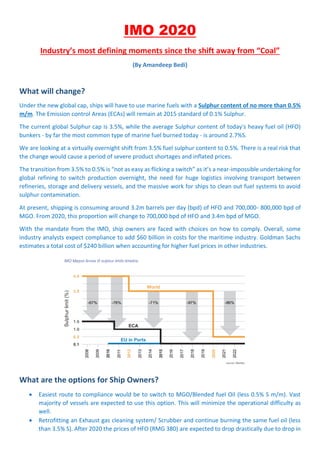

- 1. IMO 2020 Industry’s most defining moments since the shift away from “Coal” (By Amandeep Bedi) What will change? Under the new global cap, ships will have to use marine fuels with a Sulphur content of no more than 0.5% m/m. The Emission control Areas (ECAs) will remain at 2015 standard of 0.1% Sulphur. The current global Sulphur cap is 3.5%, while the average Sulphur content of today's heavy fuel oil (HFO) bunkers - by far the most common type of marine fuel burned today - is around 2.7%S. We are looking at a virtually overnight shift from 3.5% fuel sulphur content to 0.5%. There is a real risk that the change would cause a period of severe product shortages and inflated prices. The transition from 3.5% to 0.5% is “not as easy as flicking a switch” as it’s a near-impossible undertaking for global refining to switch production overnight, the need for huge logistics involving transport between refineries, storage and delivery vessels, and the massive work for ships to clean out fuel systems to avoid sulphur contamination. At present, shipping is consuming around 3.2m barrels per day (bpd) of HFO and 700,000- 800,000 bpd of MGO. From 2020, this proportion will change to 700,000 bpd of HFO and 3.4m bpd of MGO. With the mandate from the IMO, ship owners are faced with choices on how to comply. Overall, some industry analysts expect compliance to add $60 billion in costs for the maritime industry. Goldman Sachs estimates a total cost of $240 billion when accounting for higher fuel prices in other industries. What are the options for Ship Owners? Easiest route to compliance would be to switch to MGO/Blended fuel Oil (less 0.5% S m/m). Vast majority of vessels are expected to use this option. This will minimize the operational difficulty as well. Retrofitting an Exhaust gas cleaning system/ Scrubber and continue burning the same fuel oil (less than 3.5% S). After 2020 the prices of HFO (RMG 380) are expected to drop drastically due to drop in

- 2. demand, thus installing a Scrubber might prove to be cost effective in a long run. As per a recent survey around 19% of ship Owners worldwide will consider this option. LNG Propulsion (New Build/Retrofit) – Ship Owners can opt to modify the propulsion systems to run on LNG fuel, though this will mainly depend upon the trading area of the vessel as LNG Bunkers are not available worldwide at the moment but the infrastructure is growing rapidly. The LNG option in itself is facing a ‘chicken and egg’ situation. There is a need for demand to increase in order to generate greater supply, but the same is true vice versa. LNG as bunker fuel continues to face issues such as the need for increased and dedicated storage space, a gap in supply chain logistics, and requirements for costly modifications to existing port infrastructure. Additional costs to carry out LNG bunkering include delivery of the clean gas to the import terminal, breakbulk charges, the need for shuttle vessels delivering to LNG bunker tankers, and the fee of bunker tanker delivering LNG fuel ship-to-ship. Moreover, there is the unforeseen factor of fossil fuel prices, which have now fallen and making the economic business case for LNG less attractive Switch to Liquefied Petroleum Gas (LPG) is also surely a very attractive proposition for the LPG vessels as it will improve their tradability. Worldwide scrubber installation progress:

- 3. The predicted number of installations was about 3800 vessels by 31-May-2018 but that wasn’t achieved. As per the latest stats 983 vessels are retro - fitted with Scrubbers and 1561 vessels have it on order. What are the challenges? Worldwide availability of MGO/Blended fuel Oil (less 0.5% S m/m). Due to higher cost of Low Sulphur fuel Charterers/Ship Owners will need higher levels of credit, and suppliers will need a similar increase in liquidity if they wish to continue to deal with the same volume of bunkers they do today. Long delivery time for Scrubber equipment due to high demand, should the ship Owners consider this option. Scrubbers systems are fairly new in the market and once retrofitted will definitely pose some technical difficulties during initial years of operation. They are not easy equipment to operate as most people will making them, so we need to make sure we understand the technology first. Finally, different fuels mean different lubes; the buyers and suppliers of these products will also see an associated - and equally unclear - shift in their supply and demand picture. Short Vs Long term Challenges (Global Sulphur cap Vs Greenhouse gases Reduction) Options for LPG vessels (e.g VLGC): 1. If Scrubber option is considered: Approx USD 3~3.5m / vessel. Offhire charges additional. 2. If no modifications is considered: These vessel’s consume about 56 MT of fuel / day (ME, AEs and Boiler). Bunker prices HFO Prices Ex Rotterdam (USD 432/ MT) and MGO (USD 652/MT). Additional fuel cost / day to operate on MGO – USD 12320. (This way the cost of Scrubber installation can be recovered within 300 sailing days of the vessel). Considering present markets with rock bottom freights an additional “Million dollar burden” is definitely not welcomed by any Ship Owners but it will be very soon that the charterers might start looking in for vessels fitted with Scrubbers and might be ready to offer better freights for them. As predicted by market experts after the switch to Low Sulphur Bunkers the increased fuel cost would initially be passed on to the consumers as the freights will go up in order to cover up for the additional transportation cost but it will settle down eventually as more options will be available in the market.

- 4. Immediate actions from Ship Owners/Ship Managers Ship Owners/ Managers should start preparing their vessels for long term ops on Gas oil. Following can be considered: Check how to reduce the steam producing capacity of the EGB. Some VLGCs are fitted with “run dry” type of EGB’s so it’s easier to plug tubes and reduce capacity. Plan to be discussed with Makers and Class. Prepare to isolate the steam coils in the F. O tanks (Bunker/settling service). Get the lubricity improving products on board (Octamar/Amergy XLS/etc). Buy the tank cleaning chemicals and place them on board. Cost to be discussed with Owners. Prepare for each ship a sequence of tank change overs and discuss the plan with charterers. A riding team might have to be placed on board for tank cleaning. Main Engine / DGs / Boilers – Operating procedures need to be changed and approved. Overhaul all ME fuel Pumps in 2019 and renew the seals. Supply an additional set of spare plunger/barrels as the availability of spares might become difficult at a later stage. Review the minimum spares list for the Main, auxiliary machinery and the fuel system and supply the required spares. 2 Stroke - Prepare to change over to Low TBN cylinder oil and check with the manufacturer in how far they can be mixed and the proportion of the mix required with crankcase oil to come to the right TBN. Start checking the High TBN stock on board. The 4 Stroke system oil also might have to be changed to a lower TBN same to be checked with LO Suppliers and list of ports with availability of this LO. For vessels on World-wide tramping, fitting a MGO cooler to be discussed with Owners. A review on worldwide availability of 0.5%S m/m fuel in 2020 has been done by MEPC70 and they are confident that sufficient fuel is available to make this change real, the new rules come into force in just under 15 months’ time. References: 1. EGCSA (Exhaust gas cleaning systems association) 2. DNV GL – Insight at Posidonia. 3. IMO Sulphur 2020. 4. Sea trade Maritime news – The 2020 IMO fuel Sulphur Regulation. 5. Oil & Gas Journal – IMO 2020 – The next big thing. 6. Ship & Bunker (Shipandbunker.com). 7. ExxonMobil – Voyage Newsletter.