1

Summer traing report

Waysto Increase the Idea Cellular Ltd.

Submitted By :

Nuzahat Afrose

Submitted To :

C.Lal IMS (Shepa)

In partial fullfillment of the requirement of mba

degree of u.p. Technical university, lucknow

Session : 2009-10

EnrolmentNo…………….. RollNo.0918470034

INSTITUTE OF MANAGEMENT SCIENCES

SHEPA

(Nibia, Bachchaon, VRM Bypass, Varanasi-210011)

3

PREFACE

I am highlyobliged to the learners and the guider whose kind blessings energies

me to complete my report. I would specially like to thanks and great regards to

my guide Mr.Saurabh Jaisawal whose kind guidance, motivation made me to

complete this reporton time.

The project is carried out to translate the theoretical knowledge of subject into

practical field work. This project is carried out in partial fulfillment of MBA – 2nd

Semester coursefrom ISMT, Varanasi

Nuzahat Afrose

4.

4

ACKNOWLEDGEMENT

This report bearsthe imprint of many people. Right from the experienced staff of

Idea Cellular Ltd, to the staff of Atal Bihari Vajpayee – Indian Institute of

Information Technology and Management without whose support and guidance I

would have not got the unique opportunity to successfully complete my internship

in this esteemed organization.

I would like to thank Mr. Amaljeet Singh, who allow me to do this project in Idea

Cellular Ltd successfully.

I take this opportunity to express my deep gratitude to all the employees of, Idea,

Gwalior. Also I am indebted for the rich guidance, knowledge and suggestions

provided by my guide, Mr. Yugal Kishore who took sincere efforts and illustrated

the Marketing Concept and channel development in Idea Cellular Ltd, with their

vast knowledge in the field, which helped me in carrying outmy internship.

Last but not least, I also thank all those people whom I met in the industry during

my internship and helped me to accomplish my assignments in the most efficient

and effective manner.

Date: Nuzahat Afrose

Place:

6

INTRODUCTION

As India's leadingGSM Mobile Services operator, IDEA Cellular has licenses to

operate in 11 circles. With a customer base of over 17 million, IDEA Cellular has

operations in Delhi, Maharashtra, Goa, Gujarat, Andhra Pradesh, Madhya

Pradesh, Chattisgarh, Uttaranchal, Haryana, UP-West, Himachal Pradesh and

Kerala. IDEA Cellular's footprint currently covers approximately 45% of India's

population and over 50% of the potential telecom-market.

As a leader in Value Added Services, Innovation is central to IDEA's VAS Factory. It

is the first cellular company to launch music messaging with 'Cellular Jockey',

'Background Tones', 'Group Talk', a voice portal with 'Say IDEA' and a complete

suite of Mobile Email Services.

Idea Cellular is a wireless telephony company operating in various states in India.

It initially started in 1995 as a join venture between the Tatas, Aditya Birla Group

and AT&T by merging Tata Cellular and Birla AT&T Communications.

Initially having a very limited footprint in the GSM arena, the acquisition of

Escotel in 2004 gave Idea a truly pan-India presence covering Maharashtra

(excluding Mumbai), Goa, Gujarat, Andhra Pradesh, Madhya Pradesh, Chattisgarh,

Uttar Pradesh (East and West), Haryana, Kerala, Rajasthan and Delhi (inclusive of

NCR).

The company has its retail outlets under the "Idea n' U" banner. The company has

also been the first to offer flexible tariff plans for prepaid customers. It also offers

GPRS services in urban areas.

7.

7

IDEA Cellular isa publicly listed company, having listed on the

Bombay Stock Exchange (BSE) and the National Stock Exchange (NSE) in

March2007.

IIDEA Cellular is a leading GSM mobile service operator with pan India licenses.

With a customer base of over 44 million in 17 service areas, operations are soon

expected to start in Chennai Metro; Kolkata & West Bengal, North East & Assam,

and J&K.

A frontrunner in introducing revolutionary tariff plans, IDEA Cellular has the

distinction of offering the most customer friendly and competitive Pre Paid

offerings, for the first time in India, in an increasingly segmented market. From

basic voice & Short Message Service (SMS) services to high-end value added

services such as Mobile TV, Games etc - IDEA is seen as an innovative,

customerfocusedbrand.

IDEA 'Women's Card' caters to the special needs of women on

the move, and 'Youth Card' covers the emerging youth segment. IDEA 'My Gang' -

the widely popular community user group product recently bagged the

prestigious 'Golden Peacock Award 2008' under the Most Innovative Product

category at the "19th World Congress on Total Quality".

A brand known for many firsts, IDEA was the first to launch

GPRS and EDGE in India. IDEA has partnered with Research in Motion (RIM) to

offer Blackberry services on its network. IDEA 'Net Setter'- Plug & Play, EDGE

enabled USB Data Card offers affordable data connectivity with faster speed and

consistency.

8.

8

IDEA offers seamlesscoverage to roaming customers traveling to any part of

the country, as well as to international traveling customers across over 200

countries. IDEA Cellular has partnership with over 400 operators worldwide to

ensurethat customers arealways connected while on the move, across theglobe.

IDEA has received several national and international recognitions for its path-

breaking innovations in mobile telephony products & services. It won the GSM

Association Award for "Best Billing and Customer Care Solution" for 2 consecutive

years. It was awarded "Mobile Operator of the Year Award - India" for 2007 and

2008 at the Annual Asian Mobile News Awards.

9.

9

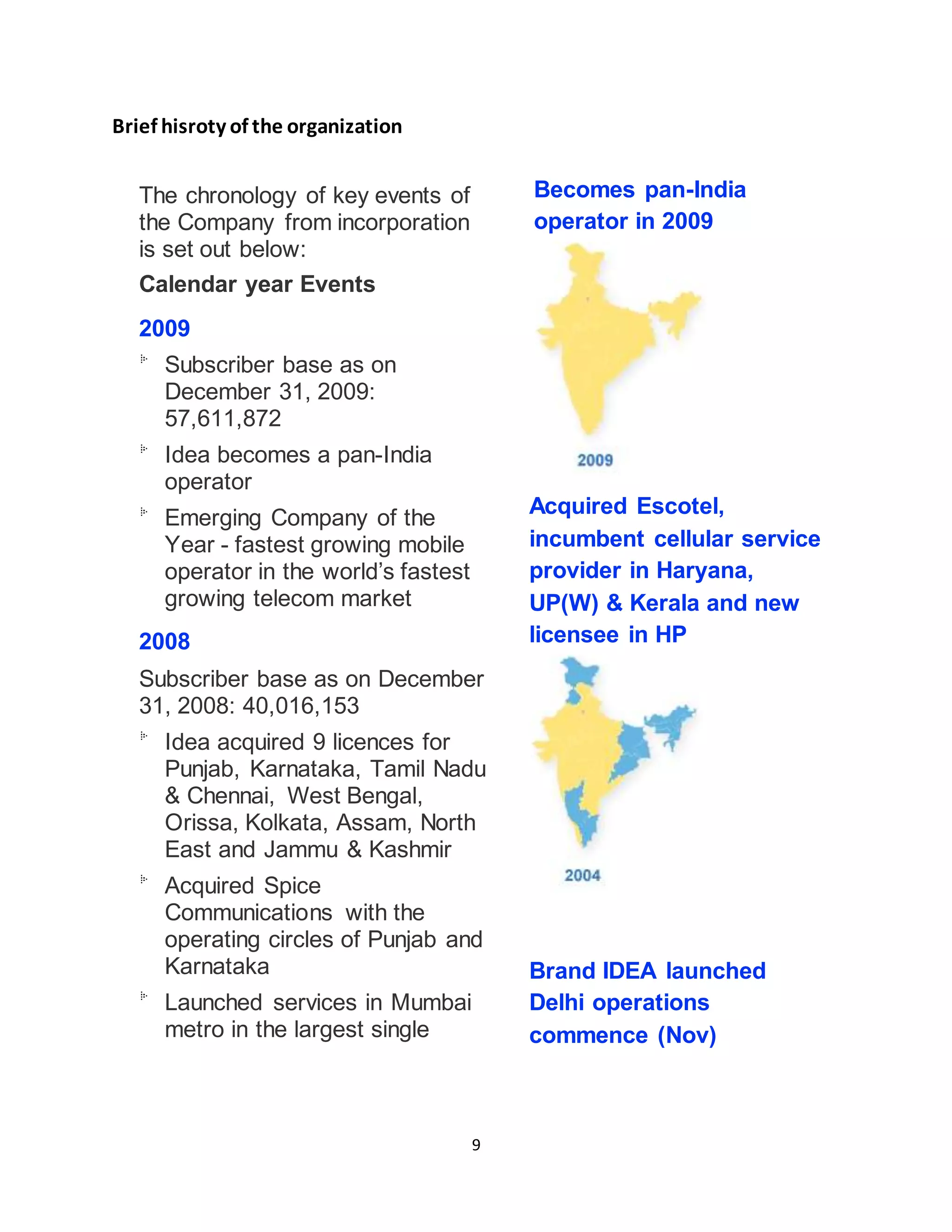

Brief hisroty ofthe organization

The chronology of key events of

the Company from incorporation

is set out below:

Calendar year Events

2009

Subscriber base as on

December 31, 2009:

57,611,872

Idea becomes a pan-India

operator

Emerging Company of the

Year - fastest growing mobile

operator in the world’s fastest

growing telecom market

2008

Subscriber base as on December

31, 2008: 40,016,153

Idea acquired 9 licences for

Punjab, Karnataka, Tamil Nadu

& Chennai, West Bengal,

Orissa, Kolkata, Assam, North

East and Jammu & Kashmir

Acquired Spice

Communications with the

operating circles of Punjab and

Karnataka

Launched services in Mumbai

metro in the largest single

Becomes pan-India

operator in 2009

Acquired Escotel,

incumbent cellular service

provider in Haryana,

UP(W) & Kerala and new

licensee in HP

Brand IDEA launched

Delhi operations

commence (Nov)

10.

10

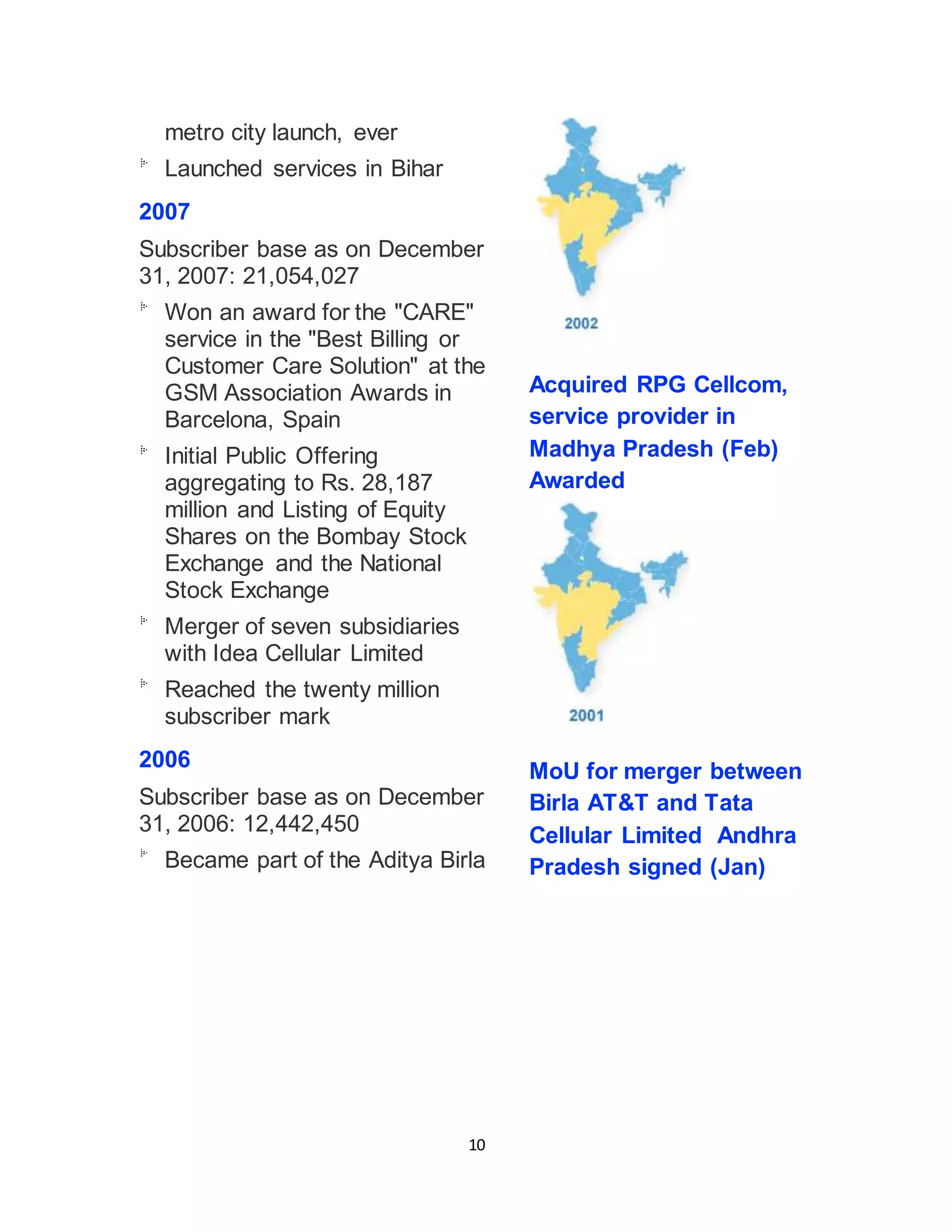

metro city launch,ever

Launched services in Bihar

2007

Subscriber base as on December

31, 2007: 21,054,027

Won an award for the "CARE"

service in the "Best Billing or

Customer Care Solution" at the

GSM Association Awards in

Barcelona, Spain

Initial Public Offering

aggregating to Rs. 28,187

million and Listing of Equity

Shares on the Bombay Stock

Exchange and the National

Stock Exchange

Merger of seven subsidiaries

with Idea Cellular Limited

Reached the twenty million

subscriber mark

2006

Subscriber base as on December

31, 2006: 12,442,450

Became part of the Aditya Birla

Acquired RPG Cellcom,

service provider in

Madhya Pradesh (Feb)

Awarded

MoU for merger between

Birla AT&T and Tata

Cellular Limited Andhra

Pradesh signed (Jan)

11.

11

Group subsequent tothe TATA

Group transferring its entire

shareholding in the Company

to the Aditya Birla Group

Acquired Escorts

Telecommunications Limited

(subsequently renamed as

Idea Telecommunications

Limited)

Restructuring of debt

Launch of the New Circles

Reached the 10 million

subscriber mark

Received Letter of Intent from

the DoT for a new UAS

License for the Mumbai Circle.

Received Letter of Intent from

the DoT for a new UAS

License for the Bihar Circle

through Aditya Birla Telecom

Limited. ABNL, the parent of

Aditya Birla Telecom Limited,

pursuant to a letter dated

November 22, 2006, agreed to

transfer its entire shareholding

in Aditya Birla Telecom Limited

to the Company for the

consideration of Rs. 100

million.

2005

Subscriber base as on December

31, 2005: 6,473,962

Reached the five million

Birla AT&T commence

Cellular operations

Maharashtra & Gujarat

12.

12

subscriber mark

Turned ProfitPositive

Won an Award for the "Bill

Flash" service at GSM

Association Awards in

Barcelona, Spain

Sponsored the International

Indian Film Academy Awards

2004

Completed debt restructuring

for the then existing debt

facilities and additional funding

for the Delhi Circle.

Acquired Escotel Mobile

Communications Limited

(subsequently renamed as

Idea Mobile Communications

Limited)

Reached the four million

subscriber mark

First operator in India to

commercially launch EDGE

services 2005

2003

Reached the two million

subscriber mark

2002

Changed name to Idea Cellular

Limited and launched "Idea"

brand name

Commenced commercial

13.

13

operations in DelhiCircle

Reached the one million

subscriber mark

2001

Acquired RPG Cellular Limited

and consequently the license

for the Madhya Pradesh

(including Chattisgarh) Circle

Changed name to Birla Tata

AT&T Limited

Obtained license for providing

GSM-based services in the

Delhi Circle following the fourth

operator GSM license bidding

process

2000

Merged with Tata Cellular

Limited, thereby acquiring

original license for the Andhra

Pradesh Circle

1999

Migrated to revenues share

license fee regime under New

Telecommunications Policy

("NTP")

1997

Commenced operations in the

Gujarat and Maharashtra

Circles

1996

14.

14

Changed name toBirla AT&T

Communications Limited

following joint venture between

Grasim Industries and AT&T

Corporation

1995

Incorporated as Birla

Communications Limited

Obtained licenses for providing

GSM-based services in the

Gujarat and Maharashtra

Circles following the original

GSM license bidding process.

Vision

It goes without saying that the brand vision of idea mirrors the company’s vision.

The brand mission statement is...... To be the most customer-focused mobile

service brand, continuously innovating to help liberate our customers from the

shackles of time & space.

Mission

The India footprint Idea

Anywhere connectivity - bringing India closer.

The Technology Advantage Idea

Tomorrow's technology to enrich today.

The Customer Focus Idea

Make a single interaction a lasting relationship.

15.

15

The Employee FocusIdea

Nurture the roots that nurture our ideas.

Objectives

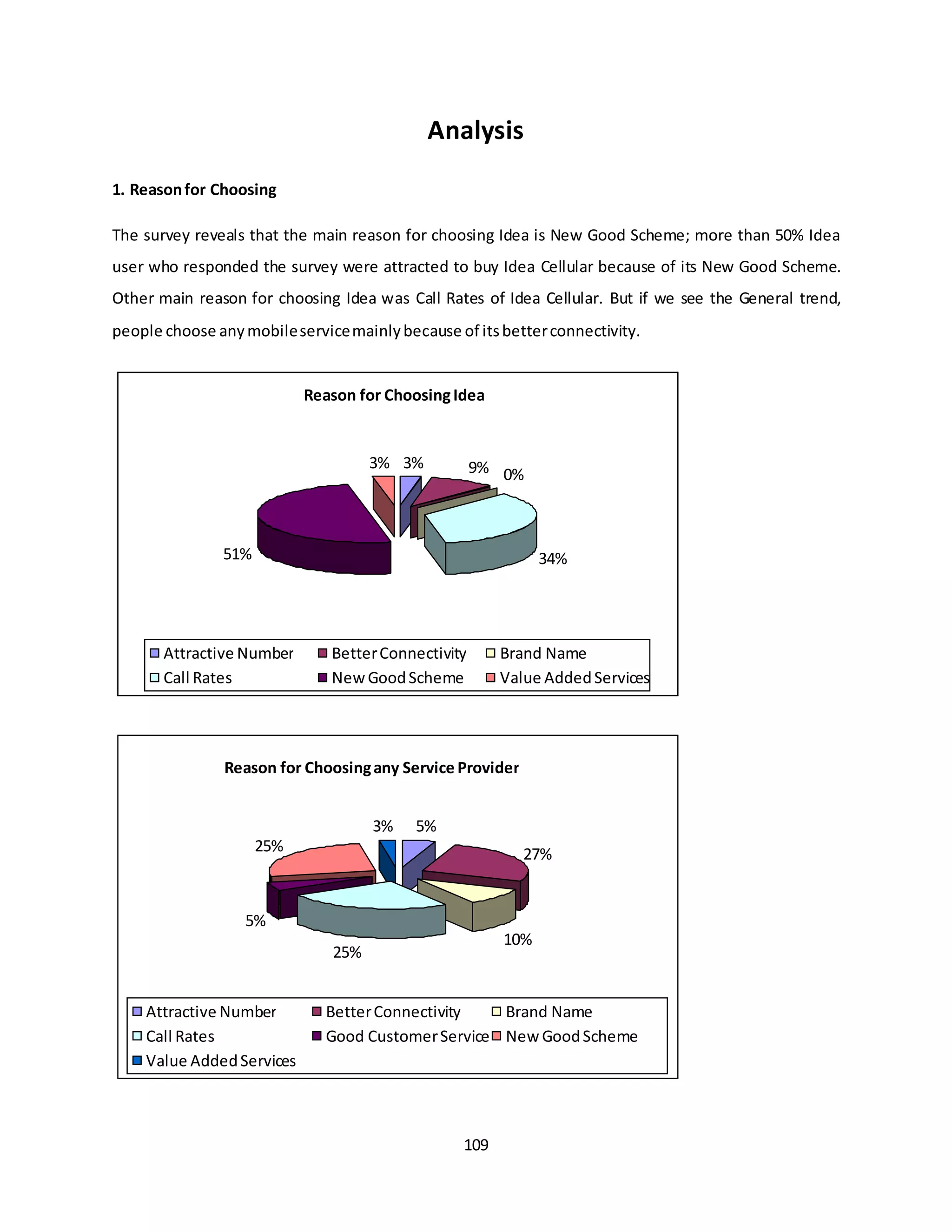

The summer internship done with Idea Cellular Objective was to find the ways of increasing the ARPU

(Average Revenue PerUser) forthe company.

The objective of the summer project was to understand the customer preferences while choosing a

telecomservice provider.

Othermainobjective of the projectwastostudythe trendsinthe International Telecommarket.

16.

16

STRATETEGYFOR IDEA CELLULAR

TheIdea Cellular Limited falls in the “question mark” quadrant of BCG matrix and

in the High attractive and Strong Competitive strength category as per the GE

Matrix. Thus they need to formulate some strategies to try capturing some market

share, growing and building their brand image as well as brand value.

Marketpenetration

The company enters where the products and the market already exists. IDEA being

a question mark that means it is competing in a high growth market but with a

relatively low share compare to its competitors. Market penetration can be done by

attracting competitor’s customers that implies increase in market share. The

strategy that IDEA can adapt under market penetration is to attract non-users and

convince to use their product more often. They are different market penetration

strategies like cutting price, increase in promotion, and creating innovative

distribution tactics. The target should be in such a way that IDEA sales volume

relative to its competitors should be high as expressed in percentage. IDEA’s

present market share is about 12%, and competitors like airtel, Vodafone, and bsnl

have a market share of about 31, 23, and 19 percent respectively. Though telecom

industry is growing rapidly every year, there is always a little increment in the

percentage of sales for IDEA. To overcome this problem and to occupy the

competitor’s position we recommend following strategies.

Increasing the mobile circles which are at present are only 11, so there is

always a need to expand its services.

Target the rural segment in India which is expected to grow by 15% every

year

17.

17

Launch differenttypes of packages as per the requirements for different

segments of the customers

Provide more high end services like GPRS, mobile internet services

Collaboration with different service providers on global basis to provide

better facility to customers on roaming.

Tracing out the search patterns which are left untapped by the competitors to

reveal new markets.

Backward Integration – In July 2008 Swedish equipment supplier entered into a

contract to provide technology “Ericsson Mobile organizer” to Idea cellular

enabling its subscribers to serve email facility on its cell phones.

Forward Integration – Company operate approximately 589 Idea” n “U and other

showrooms which supplement the distribution channels and provide customer

service.

Horizontal Integration: Idea acquired the Modi family’s stake of 40.8% in spice

which ultimately in a way increased the market share of Idea. This can be seen as

horizontal integration

Strategic Alliance

1) Product alliance

Idea should form product alliance with a company that has a strong brand

image and carry a promotion for one another. E.g. Acer in collaboration with

Ferrari launched Acer Ferrari laptops which are catering to high end niche

segment having high specifications and high price.

18.

18

2) PromotionalAlliance:

Idea shouldform promotional alliances in collaboration with big movie

houses or big retail brands to promote their products. Recently SONY Viao

had a promotional alliance with “James Bond” latest movie “Casino

Royale”.

19.

19

Organizationstructure &management

Board ofDirectors -

Mr. Kumar Mangalam Birla (Chairman)

Smt. Rajashree Birla

Mr. Sanjeev Aga (Managing Director)

Mr. Arun Thiagarajan

Ms. Tarjani Vakil

Mr. Mohan Gyani

Mr. Gian Prakash Gupta

Mr. R.C. Bhargava

Mr. P. Murari

Mr. Biswajit A. Subramanian

Dr. Rakesh Jain

Mr. Juan Villalonga Navarro

Dr. Hansa Wijayasuriya (Alternate to Mr. Juan Villalonga Navarro)

Management Team -

Corporate Leadership Team

Mr. Sanjeev Aga, Managing Director

Mr. Akshaya Moondra, Chief Financial Officer

Mr. Anil K. Tandan, Chief Technology Officer

Mr. Prakash K. Paranjape, Chief Information Officer

Mr. Pradeep Shrivastava, Chief Marketing Officer

Mr. Navanit Narayan, Chief Service Delivery Officer

Mr. Vinay K. Razdan, Chief Human Resource Officer

Mr. Rajat K. Mukarji, Chief Corporate Affairs Officer

Mr. Rajesh K. Srivastava, Chief Materials & Procurement Officer

Mr. Ambrish Jain, Director - Operations

Mr. Himanshu Kapania, Director - Operations

Circle Heads

20.

20

Mr. Iyer SubbaramanS., Chief Operating Officer, Andhra Pradesh

Mr. Rajendra Chourasia, Chief Operating Officer, Madhya

Pradesh & Chattisgarh

Mr. Virad Kaul, Chief Operating Officer, Uttar Pradesh (West),

Delhi & Haryana

Mr. T. G. B. Ramakrishna, Chief Operating Officer, Kerala

Mr. Sashi Shankar, Chief Operating Officer, Mumbai

Mr. P.Lakshminarayana, Chief Operating Officer, Maharashtra &

Goa

Mr. Naozer Firoze Aibara, Chief Operating Officer, Uttar Pradesh

(East)

Mr. Sunil Kataria, Senior Vice President - Operations, Rajasthan

Mr. Arul Bright, Senior Vice President - Operations, Gujarat

Mr. M. D. Prasad, Senior Vice President - Operations, Bihar

Mr. M. Srinivas, Senior Vice President - Operations, Tamil Nadu &

Chennai

Mr. Siva Ganapathi, Chief Operating Officer, Karnataka

Mr. Anish Roy, Chief Operating Officer, Punjab, J&K and

Himachal Pradesh

Mr. Aloke Malik, Chief Operating Officer, East (Kolkata, Rest of

Bengal, Orissa & NESA)

21.

21

Idea Cellular Limited

AnAditya Birla Group Company

Quarterly Report

Fourth Quarter ended March 31, 2009

A D I T Y A B I R L A G R O U P

istered Office: Suman Tower, Plot No. 18, Sector 11, Gandhinagar 382011, India

the Corporate Office: 5 Floor, Windsor, Off C.S.T. Road, Near Vidya Nagari,

Kalina Santacruz (East), Mumbai 400 098, India

22.

22

Supplemental Disclosures

Unless statedotherwise, the financial data in this report is derived from our

unaudited / audited consolidated financial statements prepared in accordance with

Indian GAAP. Our financial year ends on March 31 of each year, so all references

to a particular financial year are to the twelve months ending March 31 of that

year. In this report, any discrepancies in any table between the total and the sums

of the amounts listed are due to rounding-off. There are significant differences

between Indian GAAP, IFRS, and U.S. GAAP; accordingly, the degree to which

the Indian GAAP financial statements will provide meaningful information is

dependent on the reader’s level of familiarity with Indian accounting practices.

Any reliance by persons not familiar with Indian accounting practices on the

financial information presented in this report should accordingly be limited. We

have not attempted to explain those differences or quantify their impact on the

financial data included herein.

Unless stated otherwise, industry data used throughout this report has been

obtained from industry publications. Industry publications generally state that the

information contained in those publications has been obtained from sources

believed to be reliable but that their accuracy and completeness are not guaranteed

and their reliability cannot be assured. Although we believe that industry data used

in this report is reliable, it has not been independently verified. Actual results may

differ materially from those suggested by the forward-looking statements due to

risks or uncertainties associated with our expectations with respect to, but not

limited to, our ability to successfully implement our strategy, our growth and

expansion, technological changes, our exposure to market risks, general economic

and political conditions in India which have an impact on our business activities or

investments, the monetary and interest policies of India, inflation, deflation,

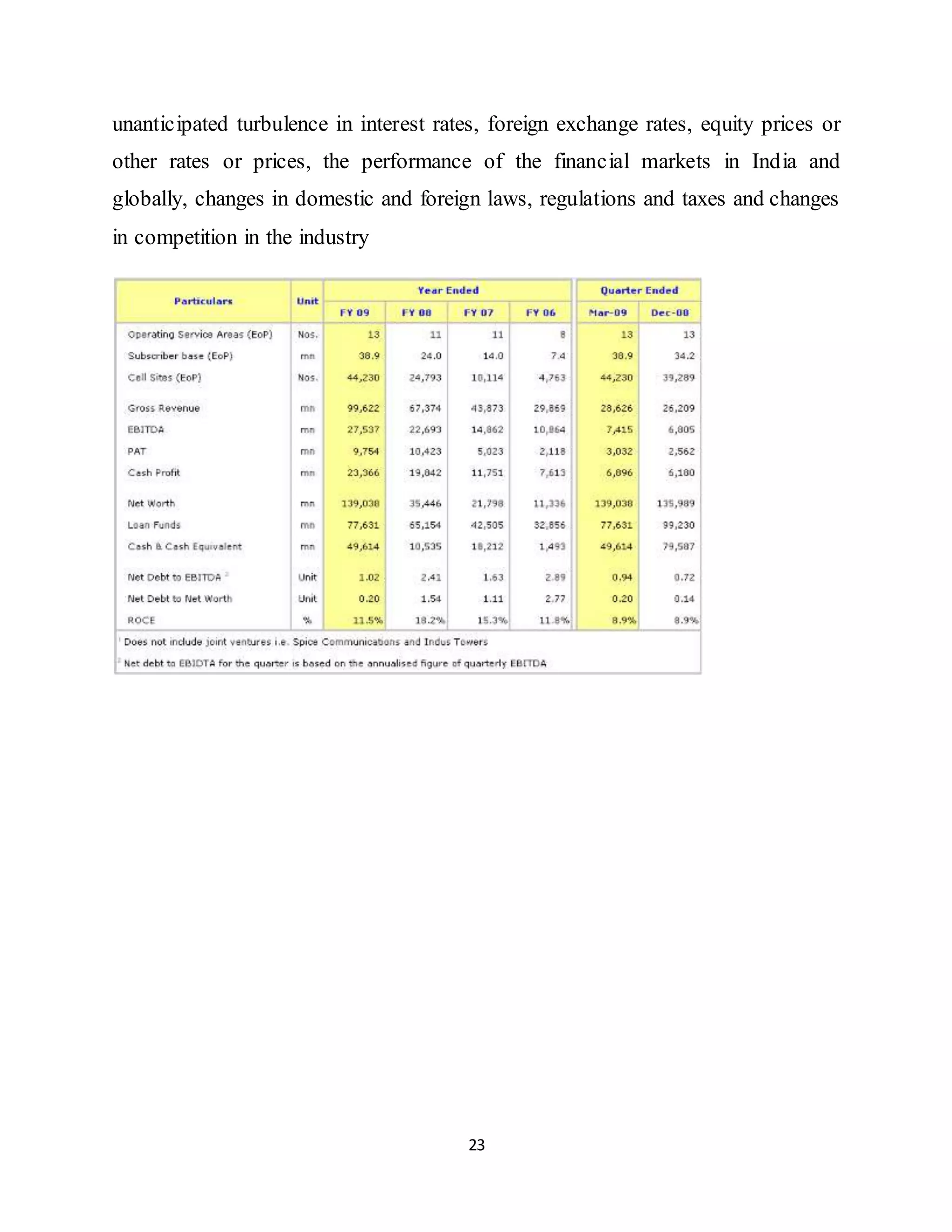

23.

23

unanticipated turbulence ininterest rates, foreign exchange rates, equity prices or

other rates or prices, the performance of the financial markets in India and

globally, changes in domestic and foreign laws, regulations and taxes and changes

in competition in the industry

24.

24

2. Company Overview

IdeaCellular Limited (“Idea”) is a leading mobile services operator in India, with ~

39 mn subscribers as on March‘09. Idea has a subscriber market share of 19.5% in

its 8 established service areas, and 14.5% in its 13 operating service areas. After

inclusion of Spice Communications, Brand !dea has 43.02 mn subscribers,

corresponding to a 11.0% national market share.

A. Promoter Group

Idea is part of the Aditya Birla Group, India's first truly multinational group. The

Group has businesses in sectors ranging from metals, garments, cement, fertilisers,

life insurance and financial services among others. Over 50% of the Group’s

revenues are derived from overseas operations. The group operates in 25 countries,

and is anchored by an extraordinary force of over 125,000 employees belonging to

25 nationalities. The current Group holding of 49.13% in Idea is made up of;

Aditya Birla Nuvo Ltd. 27.02%

Birla TMT Holdings Pvt. Ltd. 9.15%

Hindalco Industries Ltd. 7.37%

Grasim Industries Ltd. 5.52%

IGH Holdings Pvt. Ltd. 0.08%

Total 49.13%

25.

25

B. Key Shareholders

AXIATAGroup Berhad, previously TM International Berhad, through its

affiliates has 14.99% shareholding in Idea Cellular, and a 49.0% holding in Spice

Communications. With the proposed merger of Spice Communications into Idea

Cellular, the Axiata Group holding in Idea Cellular would increase to around 20%.

The Group, is one of the largest Asian telecommunication companies, focused in

high growth low penetration emerging markets. AXIATA has a controlling

interest in Malaysia, Indonesia, Sri Lanka, Bangladesh and Cambodia with

significant strategic stakes in India and Singapore. India and Indonesia are some of

the fastest growing markets in the world. In addition, the Malaysian grown holding

company has assets in telecommunication operations in Thailand, Pakistan and

Iran. As of December 2008, the Group, including its subsidiaries and associates,

has close to 90 million mobile subscribers in Asia. The Group provides

employment to over 25,000 people across Asia. Upon its de-merger from Telekom

Malaysia in April 2008, AXIATA became an independent entity and

simultaneously listed on the Malaysian stockexchange.

Providence Equity Partners, through its affiliates has a 10.6% shareholding in Idea,

and has also invested Rs. 20982 mn in ABTL through Compulsorily Convertible

Preference Shares.

26.

26

C. CorporateStructure

Idea CellularLimited (Idea)

100% -- Idea Cellular Infrastructure Services Limited (ICISL) 100% --

Idea Cellular Services Limited (ICSL) 100% -- Swinder Singh Satara & Co

Limited (SSSL) 41.1% -- Spice Communications Limited (Spice)

100% -- Aditya Birla Telecom Limited (ABTL)

100% -- Idea Cellular Tower Infrastructure Limited (ICTIL) 16% --

Indus Towers Limited (Indus)

IICCIISSLL – tower company owning towers in Bihar and Orissa service area.

IICCSSLL – provides manpower services to operating entities i.e. Idea & ABTL.

SSSSSSLL– holds MSC real estate in the Delhi service area.

SSppiiccee – provides GSM based mobile services in Punjab and Karnataka

service areas. AABBTTLL – provides GSM based mobile services in Bihar service

area, and has 16% shareholding in Indus. IICCTTIILL – holds towers de-merged

from Idea, which will subsequently merge in Indus. IInndduuss – a joint venture

between Bharti Infratel, Vodafone Essar and Idea (through ABTL), to provide

passive infrastructure services in 15 service areas.

27.

27

Operating Service Areas(as on April 2009))

Brand “!dea” covers 16 telecom service areas, viz, Maharashtra & Goa, Gujarat,

Andhra Pradesh, Madhya Pradesh & Chhattisgarh, Delhi, Kerala, Haryana, Uttar

Pradesh West & Uttaranchal, Rajasthan, Uttar Pradesh East, Himachal Pradesh,

Mumbai, Bihar & Jharkhand, Orissa, Punjab and Karnataka, covering ~ 80% of

the all India subscriberbase. Of these, the 3 service areas of Rajasthan, UP East

and Himachal Pradesh, were rolled out during Sep-Nov’06, while the 2 service

areas of Mumbai and Bihar became operational during Aug-Oct‘08. The service

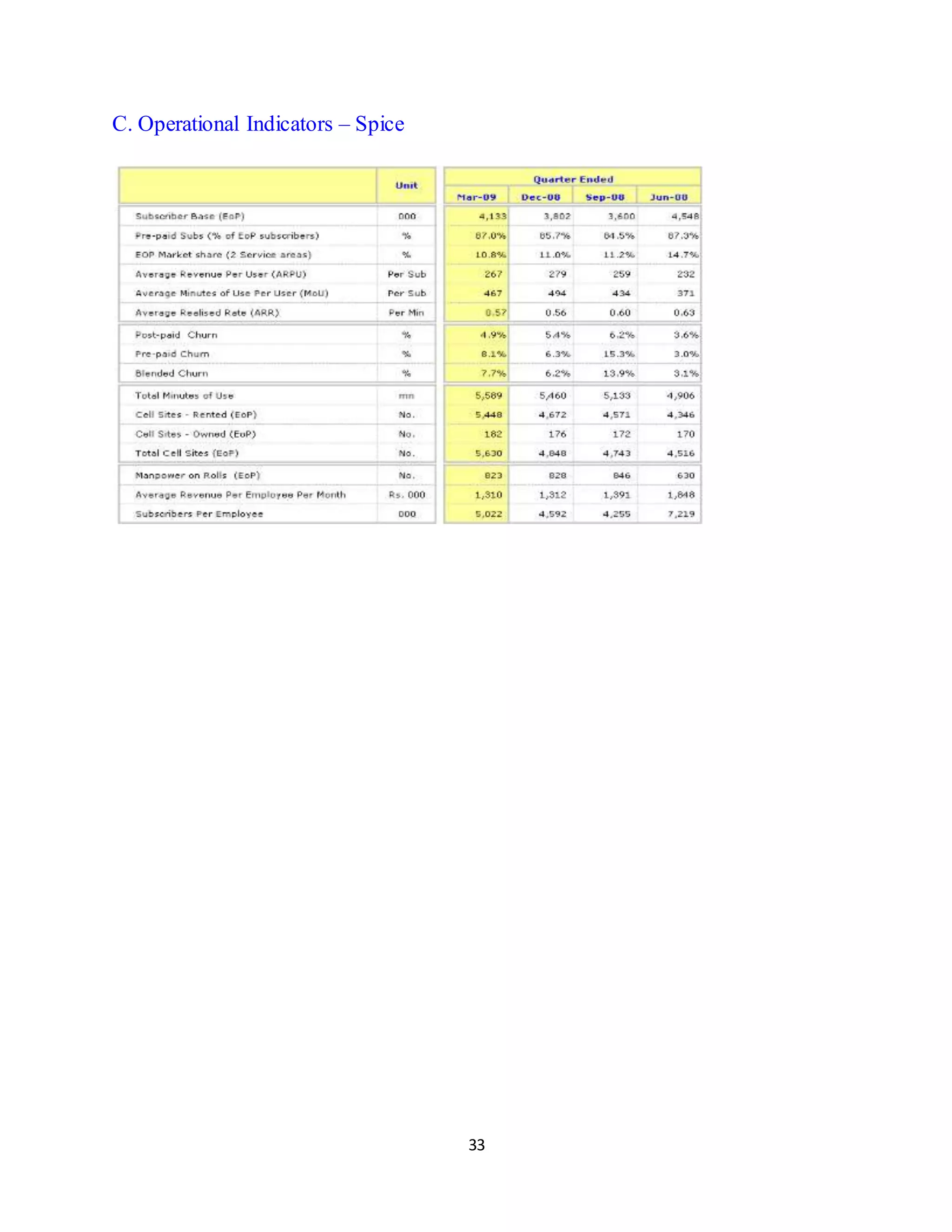

areas of Punjab and Karnataka were added through Spice w.e.f October16,

2008.

28.

28

3. Reporting Guidelines:

Tofacilitate an analytical perspective, the results have been formatted and grouped

as under: a) Standalone – Idea, and its 100% subsidiaries, grouped together on a

standalone basis. Effectively, this encompasses all mobile operations in India,

excluding Spice and Indus.

b) Consolidated – Idea and its 100% subsidiaries, and JVs, grouped together. This

covers Idea operating service areas and the ABTL operating service area of Bihar,

the proportionate consolidation of Indus (16%), and the proportionate

consolidation of Spice (41.09% w.e.f. October16, 2008).

JV financials have been consolidated as jointly controlled entities as per “AS 27 -

Financial reporting of Interests in Joint Ventures ”. It may be noted that the

consolidation of financials of two or more entities requires elimination of inter

entity transactions. Illustratively, rentals paid by Idea to Indus, become expenses

for Idea and revenues for Indus, on a standalone basis. However, upon

consolidation, the proportionate revenue of Indus gets reduced to the extent

contributed by Idea. The rental expenses of Idea also stand correspondingly

reduced in the consolidated financials.

34

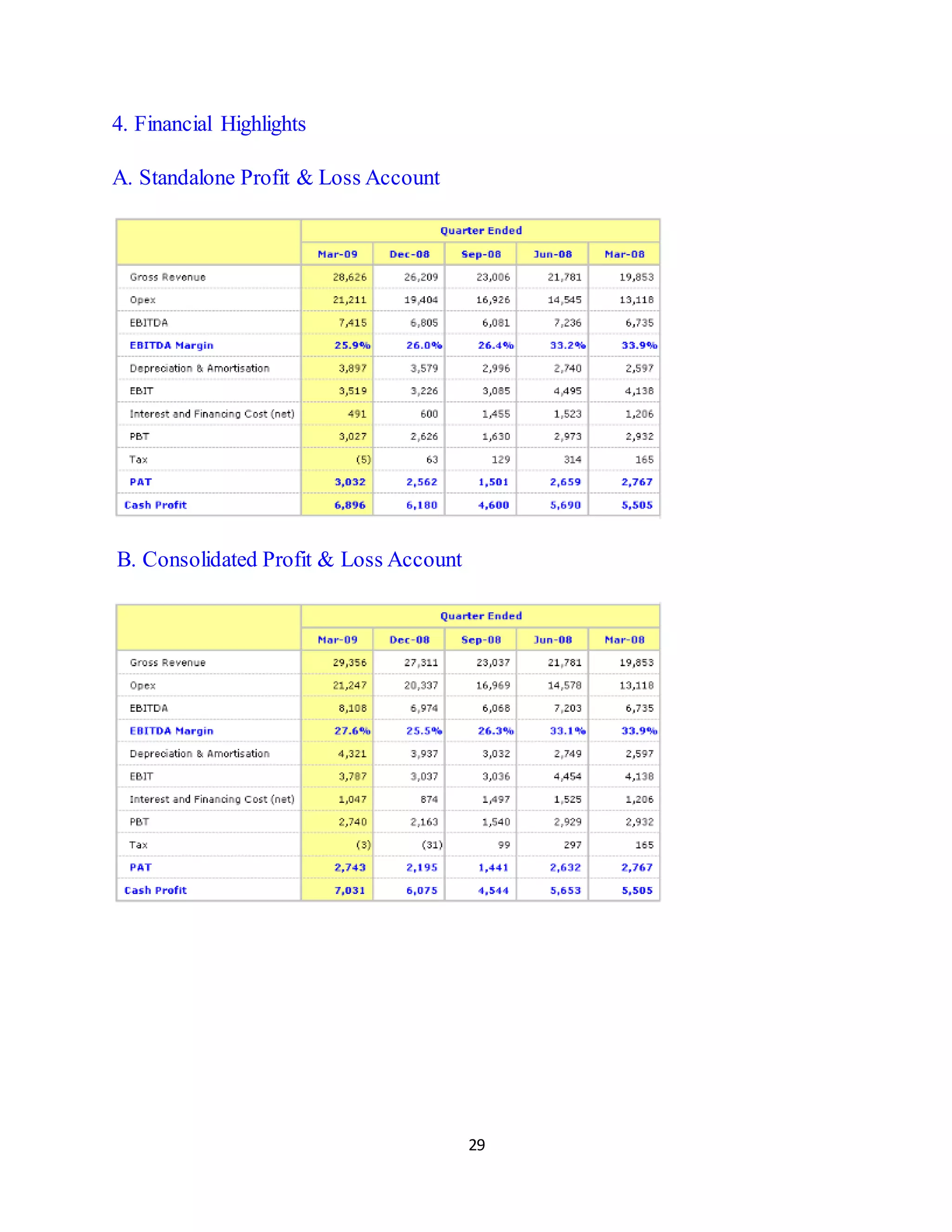

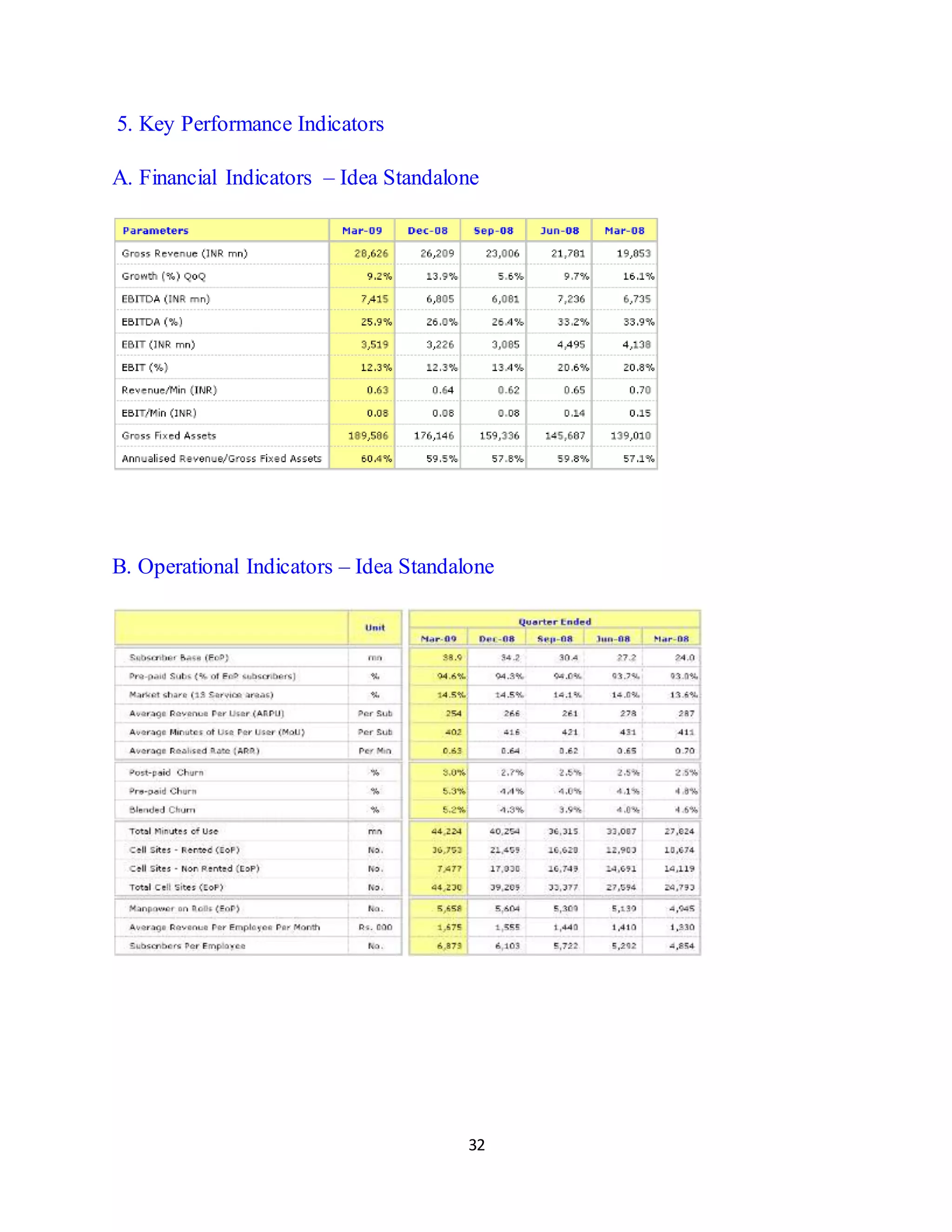

6. Management Discussion& Analysis

Fastest Growing Major Telco – Back to Back Years of Strong Market Gains

Standalone revenues for the quarter at Rs. 28,626 mn, grew 9.2% on a QoQ basis.

In a period marked by economic downturn and increased competitive and price

pressure, Idea was able to maintain its strong growth momentum. Annual revenues

of 99,622 mn show a growth of 47.9%

compared to the last year. This revenue growth

of 47.9%, on the back of the FY08 revenue

growth of 53.6%, places Idea as the fastest

growing major operator in one of the largest, fastest growing, and most

competitive telecom markets in the world. Idea on a standalone basis, added 4.7

mn subscribers in the

quarter, its highest ever. For the entire year FY09, subscriber base has grown

by 79.2 %. In its 8 established service areas, Idea strengthened its market position

by gaining 1% market share, and consolidating its position close to the market

leader. In the 3 gestating service areas, Idea also increased its market share to

6.3%, from 5.8% a due to change in subscribers recognition criteria year ago.

In the newly launched service areas of Mumbai and Bihar, Idea has

acquired a 4.0 % share of the combined market, with a net adds market share of

16.6%, during last 6 months.

Total Minutes on the Network at 44,224 mn grew by 9.9% on a QoQ basis.

The Average Realised Rate per Minute, which had moved up from 62p to 64p in

the previous quarter, settled at 63p.

35.

35

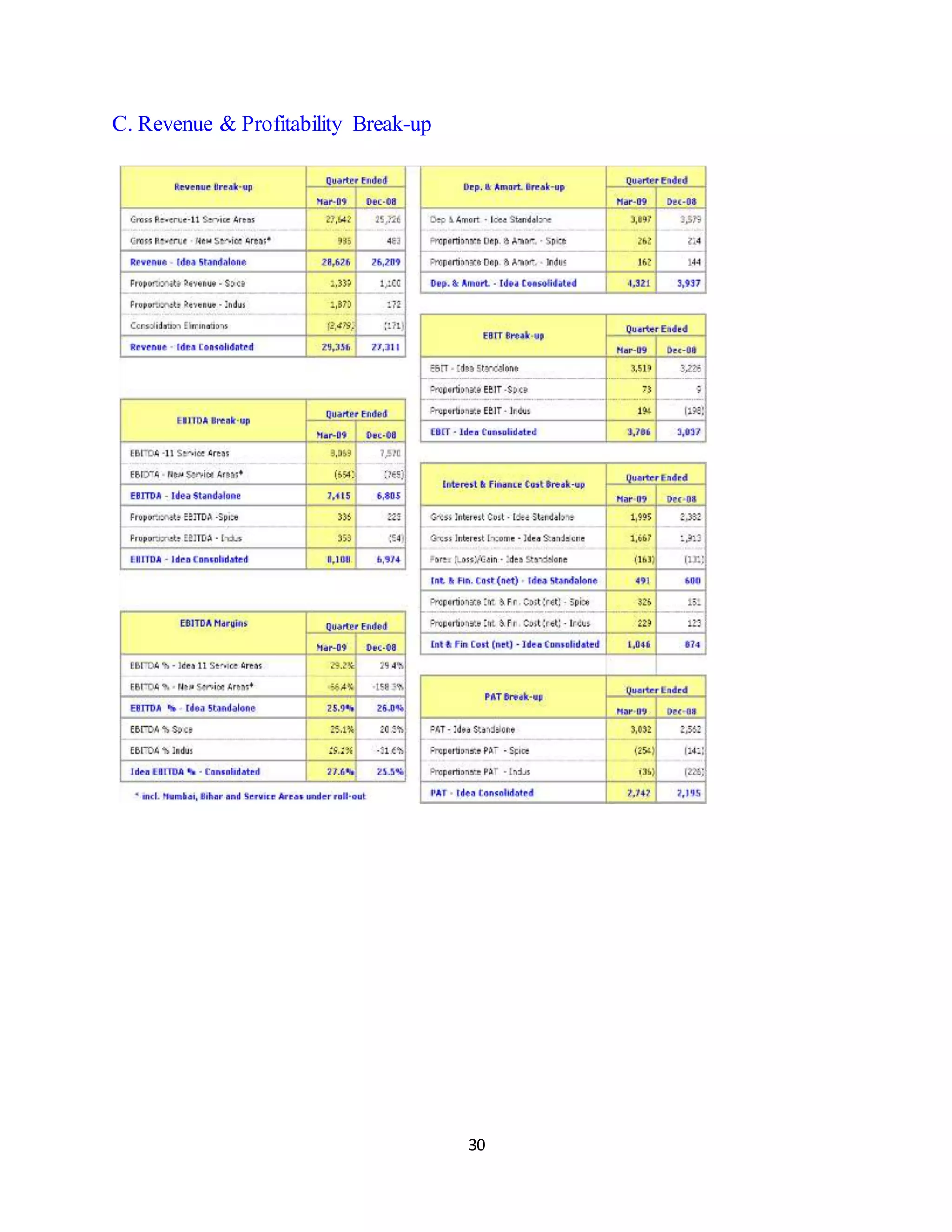

Indus IRU Impact

Idea(standalone) rent-paying cell sites jumped from 21,459 at Dec’08 quarter end

to 36,573 at Mar’09 quarter end. This increase of 15,294 cell sites includes 11,094

cell sites on Idea towers, transferred to Indus, through the IRU effective January 1,

2009. As of March’09, out of the 36,573 rent paying cell sites, 25,150 cell sites are

on Indus Towers. The accounting treatment of the IRU arrangement increased the

network operating cost for the March’09 quarter. Rental income that Idea was

deriving from guest sites also ceased w.e.f. January 1, 2009, as these would accrue

to Indus. The combined impact of these 2 factors was the equivalent of ~ 3.4 %

EBITDA contraction for the quarter ended March’09. Until the merger into Indus

is consummated, Idea will account for depreciation for the IRU towers. However,

Idea will receive an IRU income for the transferred towers until the merger, which

for the quarter ended March’09 was the equivalent of ~1.2% of the EBITDA.

Therefore, the net negative EBITDA impact for the quarter was ~2.2 %. The above

treatment does not include Idea’s pro-rata share of Indus’ profit/loss. The

financials do not also capture the notional capex cost saving derived because of

Indus, and the speed to market benefit.

Upon consolidation, Idea’s share of 16% of Indus revenues is Rs. 1,870 mn.

However, with consolidation eliminations, no revenue has been consolidated. An

equal amount has been eliminated from the Indus rentals accounted by Idea.

Further Idea has consolidated Rs. 1,196 mn as 16% share of Indus operating

expenses, after elimination of IRU income received from Indus.

36.

36

Network Capacity

Cell sites

Idearolled out 4,941 cell sites during the March’09 quarter, taking the FY09

4423050000tally to 19,437, and the EoP cell sites to 44,230. In the preceding year

FY08, 40000Idea had added 14,679 cell sites. Thus, in the last 2 fiscal years, Idea

has enhanced its cell site capacity 4.4 times, representing a massive

2479330000enhancement of capacity to build competitive strength.

2000010114The capacity already built, together with improved spectrum

availability and 47631000018433049enhanced technology features will result in

greater capex efficiency in FY10, 0and reduced capex intensity.

FY04FY05FY06FY 07FY08FY09Total capex for FY09 was Rs. 54.5 bn. For

FY10, including for new service area launches, the capex will indicatively be in the

region of Rs. 60.0 bn. This estimate does not factor the unknown impact of a

possible 3G auction. Financial Performance

At the EBITDA level the net negative impact of Indus IRU is 2.2% for the quarter.

However, EBITDA margin for Q4 at 25.9% is almost similar to the Q3 margin,

indicative of other operational efficiencies which have absorbed the negative Indus

IRU impact.

Depreciation & Amortization for FY09 at Rs.13,212 mn increased by 50.7% on a

YoY basis. Net interest and finance cost for FY09 at Rs.4,070 mn increased by

46.6% on a YoY basis.

PAT for the quarter at Rs.3,032 mn was higher by 18.3% on a QoQ basis. After

absorbing the losses of the new launches of Mumbai and Bihar, Profit after Tax for

FY09 was Rs.9,754 mn.

37.

37

New Launches

thBrand Ideahas expanded its wings to its 16 service area, with the commercial

launch of Orissa in April 2009. With this, Idea now covers ~ 80% of the national

subscriber base. Preparatory work for other roll outs is on track, with Tamil Nadu

planned for the Jun’09 quarter. Within the calendar year 2009, Idea plans to have

pan India operations. Tailored Approachfor Different Service Areas

Idea holds 900 MHz GSM spectrum in 9 service areas, which make up ~50% of

the national market. This frequency band confers capex and opex benefits. It is also

accompanied by early mover advantage. Idea is the mobility revenue market

leader in 3 of these service areas, and is overall in the second spot. Thetwin

advantages of spectrum and scale underpin Idea’s enduring competitive edge.

In some of the remaining service areas, Idea pursues a strategy of optimisation

as opposedto maximisation. It plans to achieve a pan India footprint and

leverage synergies of scale and wider presence, and calibrated capex spend

through infrastructure sharing. The focus is on operational and financial goals,

and not on league tables.

The service area tailored strategy is designed to enhance Idea’s long term

competitiveness.

38.

38

Update on SpiceCommunications

The accounts of Spice continue to be consolidated in proportion of the

shareholding of 41.09%, until its eventual merger into Idea. Finalisation of the

merger scheme is in an advanced stage and will be effective after the court order.

Update on Indus Towers

As the 3 shareholders, Bharti Infratel, Vodafone Essar Ltd and ABTL (100%

subsidiary of Idea) signed the IRU with Indus effective January 01, 2009, Indus

has started invoicing respective entities for the sites covered by the IRU. Idea has

filed the scheme for demerger of towers to ICTIL. This will be followed by the

filing of the merger scheme of ICTIL with Indus.

39.

39

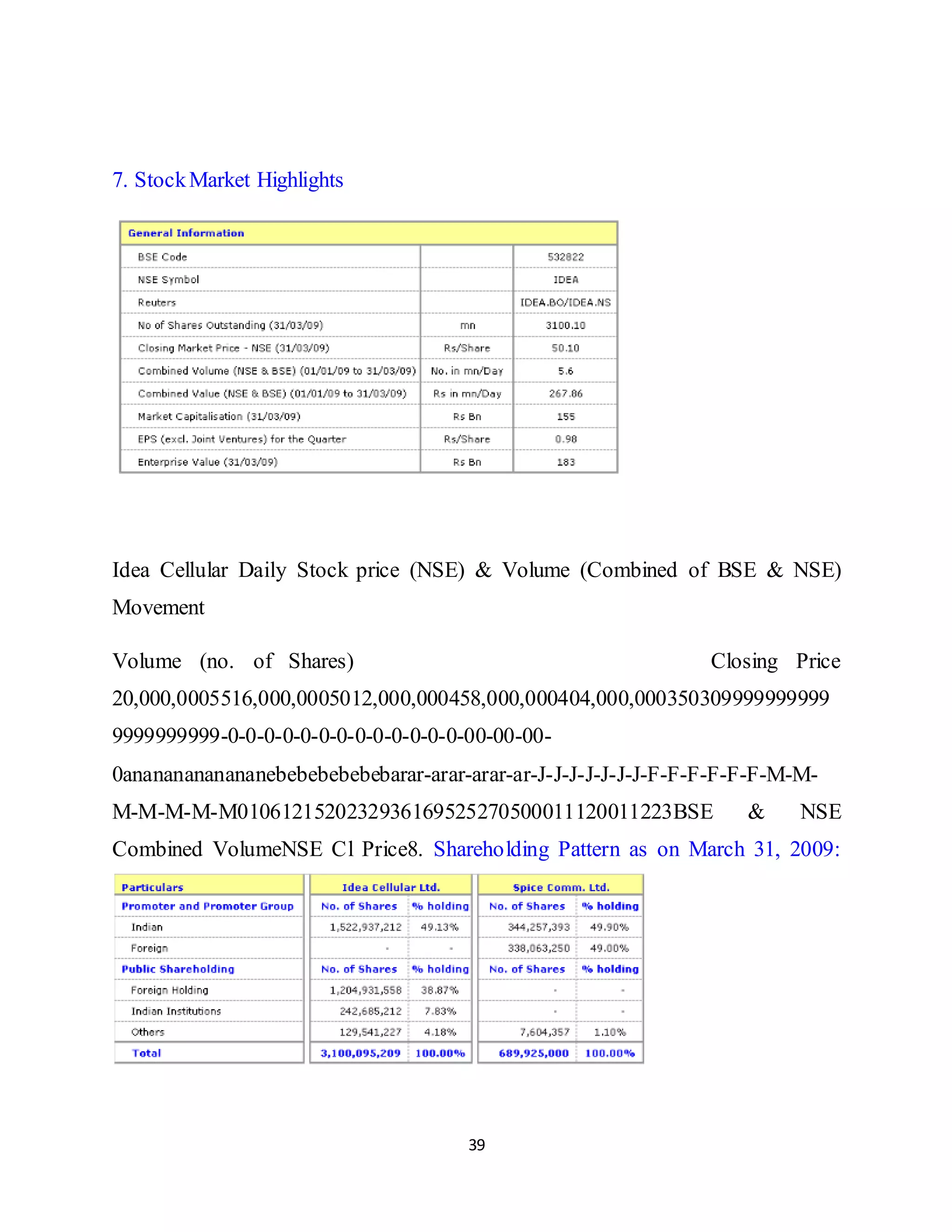

7. StockMarket Highlights

IdeaCellular Daily Stock price (NSE) & Volume (Combined of BSE & NSE)

Movement

Volume (no. of Shares) Closing Price

20,000,0005516,000,0005012,000,000458,000,000404,000,000350309999999999

9999999999-0-0-0-0-0-0-0-0-0-0-0-0-0-00-00-00-

0anananananananebebebebebebarar-arar-arar-ar-J-J-J-J-J-J-J-F-F-F-F-F-F-M-M-

M-M-M-M-M0106121520232936169525270500011120011223BSE & NSE

Combined VolumeNSE Cl Price8. Shareholding Pattern as on March 31, 2009:

40.

40

9. Glossary

Definitions/Abbreviation Description/FullForm Annualized EBITDA Annualised

figure of quarterly EBITDA ARPU (Average Revenue Per User) Is calculated by

dividing services revenue (exclusive of activation charges and infrastructure

revenues) for the relevant period by the average number of subscribers during the

period. The result obtained is divided by the number of months in that period to

arrive at the ARPU per month figure

AS Accounting Standards as issued by the Institute of Chartered Accountants of

India

ARR (Average Realised rate) ARR is calculated as ARPU divided by MoUs Churn

Churn relates to subscribers who are removed from the EoP base for discontinuing

to use the service of the company.

Circle/ Service Area Unless otherwise specifically mentioned, means telecom

circles in India (including metropolitan circles) as defined by the DoT. Circles are

classified as metropolitan circles and as category ‘A’, ‘B’ or ‘C’ Circles. The

Circles are classified on the basis of the revenue generation capacity of each circle

with category ‘A’ being considered the most revenue generating

EBIT Earnings Before Interest and Tax EBITDA (Earnings before interest, This is

the amount after deducting operating expenditure from total tax, depreciation and

amortisation) income. Total income is comprised of service revenue, sales of

41.

41

trading goods andother income. Operating expenditure is comprised of cost of

trading goods, personnel expenditure, network operating expenditure, license and

WPC charges, roaming and access charges, subscriber acquisition and servicing

expenditure, advertisement and business promotion expenditure and administration

and other expenses EoP End of period

FY /Fiscal Financial year ending March 31 GSM Global System for Mobile

communications, the most popular standard for mobile phones in the world

Indian GAAP Indian Generally Accepted Accounting Principles IRU Indefeasible

right of use MoUs/Sub (Average Minutes of We calculate the MoUs/Sub as , total

Minutes of Use in our network Usages per Subs) during the period divided by

average of subscribers during the period Net Adds Refers to net customer additions

which is calculated as the difference between the closing and the opening

customers for the period Net Debt Total loan funds reduced by cash and cash

equivalents Calculated as summation of Share Capital and Reserves & Surplus Net

Worth

reduced by debit balance of profit & loss account

PBT Profit before tax

PAT Profit after tax

ROCE ROCE is calculated as a) for the year : PAT plus gross int. & fin. cost

divided by average capital employed for the year, b) for the quarter : PAT plus

gross int. & fin. cost for the quarter is annualised and divided by capital employed

for the quarter. Capital employed is taken as average of opening and closing of

Shareholders funds and Loan Funds reduced by debit balance of P&L account, for

the respective period Subscribers Mobile telephone service customers TRAI

43

SWOT ANALYSIS ORGANIZATION

Attractiveexisting footprint–The subscriber base under brand Idea, increased from

24 million as of end March 2008 to 43.02 million as of end March 2009, a growth

of around 79%, taking its national market share to 11%.

Original licensee in seven of the Established Circles, providing incumbency

advantages-The established service areas are Delhi, Andhra Pradesh, Gujarat,

Maharashtra, Haryana, Kerala, Madhya Pradesh and Uttar Pradesh (West). The

New Service Areas are Uttar Pradesh (East), Rajasthan, Himachal Pradesh, Bihar,

Mumbai, Karnataka, Punjab, Orissa, Chennai & Tamil Nadu, Jammu & Kashmir,

Kolkata & West Bengal, and Assam & North East. leader in two of, and

established positions in the remainder of, the Established Circles.

Strong distribution channels.

High quality network structure.

Innovation –always comes out with new products.IDEA is the winner of ‘The

Emerging Company of the Year Award' at The Economic Times Corporate

Excellence Awards 2008-09. The company has received several other national and

international recognitions for its path-breaking innovations inmobile telephony

products & services. It won the GSM Association Award for “Best Billing and

Customer Care Solution” for 2 consecutive years. It was awarded “Mobile

Operator of the Year Award -India” for 2007 and 2008 at the Annual Asian Mobile

News Awards.

A national brand -The Company through its participative work

environment, skill development activities, and by championing the values of

commitment, integrity, passion, seamlessness and speed, promotes strong bonding

44.

44

with its employees.During the year, it has again undertaken sharing of value

creation by granting another tranche of employee stock options to the eligible

employees. The findings of OrganizationHealth Study (OHS) have been analyzed,

which are very encouraging, and concern areas are being suitably addressed. The

employee strength onrolls stood at 6,481 as on March 31, 2009.

Attractive growth –From 11.8 million subscribers in 2006 to 24 millionin 2008

,then to 43 million by end of March 2009 and to 51 by end of 2009 is really a great

performance from Idea.

Part of the Aditya Birla Group-IDEA Cellular is an Aditya Birla Group Company,

India's first truly multinational corporation. The group operates in 25 countries, and

is anchored by over 1, 30,000employees belonging to 30 nationalities. The Group

has been adjudged the ‘6th Top Company for Leaders in Asia Pacific Region' in

2009, in a survey conducted by Hewitt Associates, in partnership with The RBL

Group, and Fortune. The Group has also been rated ‘The Best Employer in India

and among the Top 20 in Asia' by the Hewitt-Economic Times and Wall Street

Journal Study 2007.Their promoters-1. Aditya Birla Nuvo Limited2. Grasim

Industries Limited

3. Hindalco Industries Limited

4. Birla TMT HoldingsPrivate LimitedWeaknesses -Equity Ratio: The

Company's Debt-Equity ratio is high as compared to its peers. Moreover, the

Company needs the approval of the lenders under its financing arrangements

before undertaking certain significant corporate actions. The

Company revenues are derived solely from providing mobile services and it is

dependent on four of the Established Circles for a significant proportion of its

revenues.

45.

45

The Company hadaccumulated losses amounting to Rs. 19.23 billion and Rs.

17.23 billion for financial years 2005 and 2006 respectively. The Company may

not be in a position to pay dividends until it clears its accumulated losses.

Opportunities Indian telecommunication industry is expected to continue to

enjoygrowth due to its low teledensity and increasing affordability of mobile

telephone and services. The strong growth in the sector continues, mainly due to

expansion of telecom networks to rural India, the reduced cost of entry and the

reduced cost of handsets. Low penetration, more particularly in rural India,

provides opportunity for further growth, and your company, an

incumbent GSM player with 900 MHz spectrum in about half of India, is well

positioned to tap this opportunity.

The contribution of service sector to the GDP has improved significantly from

29% in 1950 to 54% in 2005. This is primarily due to growth of information-

technology and information technology enables services. This will further

stimulate the demand for mobile telecommunication services.

The regulatory environment is improving and there is greater clarity in existing

rules and procedures. This would enable operators in improving network quality.

Also raising of funds will become easier due to greater predictability of operational

environment. from new technologies is an inherent threat. While the

planned 2100 MHz spectrum auction for 3G services will lead to additional cash

outflow, it will also open new revenue streams. The Company’s strong balance

sheet and market standing, positions it to participate effectively in such auction.

Threats There is intense competitionin the Indian telecommunication industry. Idea

Cellular faces significant competition from private companies that have a pan-

46.

46

India footprint suchas Bharti Airtel, Tata Teleservices and Reliance

Communication Ventures. Also it faces competition from government owned

companies such as BSNL and MTNL. technology is evolving very

rapidly in the telecommunications industry. For instance, “Wi-Fi”and “Wi-

Max”which allows for voice data transfer have been tested and handsets with

such technology maysoon be available in the Indian market. Moreover, satellite

communication voice data transport medium like “Skype”may become a serious

competitor in the long distance voice data transfer business.Porter’s five forces -

Analysis the external environment1.Competitive rivalry within the

Industrya.Principal competitors- industry

leader Bharti Airtel. Bharti Airtelhas 24.3% customer market share and 33.8%

revenue market share. India has 18.8% customer market share and

20.7% revenue market share.

Idea Cellular has 11.2% subscribers market share and 12.1% revenue market share

BSNL has subscriber share of 12.7% and mere 10.2% of revenue share Reliance

Communications is the worst performerwith 18.9% customer market share and

pathetic 11.5% revenue market share.

(Data mentioned are by end of August 2009)b.Salient strengths -

full advantage of its wide network and fixed line subscriber base, and has

established itself as the provider with maximum coverage over the country.

Bharti Airtel has dominated the scene with wide reach, innovative

packages, catchy ads, and has emerged the leader of the pack. Reliance

Communications also has the wide network to its advantage. Tata tele-services

banks on the Tata-trust factor to gain foothold in the market. Vodafone is hitting

the Indian market in a huge way. They have large cash reserves at their disposal to

47.

47

wipe out thecompetition in future. Weaknesses- BSNL lines are mostly marred by

congestion,bottlenecks and they have failed to capture the attention of the

customers with attractive offers. Unstable range and poor customer support are

Airtel ’ s minuses. Ambiguous schemes have reduced Reliance ’ s

popularity. Indicom has not really been able to fully capitalize its goodwill

factor. c.Their basis for competition-Vodafone and Idea are comparatively new

entrants into the market and hence the rest of the competition has anadvantage over

them. Also both these brands have undergone rebranding more than once, and

subsequently have had hiccups with people not realizing the transformation. Giants

like BSNL, Airtel and Reliance have wide networks in the nooks and crannies of

thecountry, while Idea is still to open account in several states.

2.Bargaining Power of CustomersThe bargaining power of customers determines

how much customers can impose pressure on margins and volumes. Customers

bargaining power is likely to be high because

Customersuse multiple mobile services these days and hence have a good

knowledge of the pros and cons of each service provider.

Telecommunication industry comprises a number of operators

is not related to h shave low margins and are price

sensitive

product.3.Bargaining power of suppliersIn this industry there is less number of

suppliers compared to other industries such as the manufacturing or textile

industry.

48.

48

I.Mobile handset suppliers–although there are many handset suppliers in the

country, some service providers have their own handset manufacturing units

operating inthe country like the Reliance Classic and Tata Indicom (backward

integration). Some of the telecom companies also have some collaboration with

major handset manufacturers like Samsung, L.G, and the Blackberry for their

CDMA services.II.Some other suppliers include optical fibre suppliers and

aluminium (for the construction of towers) suppliers. Here the suppliers have a

limited bargaining power.III.Another important one is the software assistance

where the suppliers have some edge. Major solution providers include TCS,

Infosys, Wipro, etc. While Reliance and Tata have their own software services

other players like Vodafone and Idea depend on the above mentioned software

service providers.

4.Threat ofnew entrantsIndian telecom sector provides unprecedented

opportunities for foreign companies in various areas such as 3G, virtual private

network, international long distance calls, value added services etc.

The market is witnessing M&A activities that are leading to consolidations in the

industry. This trend has assisted companies in expanding their reach in the Indian

telecom market to offer better services to the customers. The Indian telecom

industry has always attracted foreign investors. In fact, the cumulative FDI inflow,

from August 1991 to March 2007, in this sector amounted to $3,892.19 million.

This makes telecom the third largest sectorto attract FDI since the liberalization.

Although the entry barriers are in place like license and high fixed costs, still we

observe many new players emerging from the state-level to national-level. This

includes Aircel, Virgin, Spice and Unitech.

49.

49

5.Threat from substitutesTelecomsector offers a wide range of services in India

such as wireline, CDMA, GSM, internet, VoIP, IP etc.

Internet telephone is emerging as a best substitute for the mobile telephony

because it is cheaper and video can also be added. The increasing use and

penetration of internet in the country also augments this. Other facilities on the

internet such as Google talk, Yahoo Messenger, Rediff Bol are used at an

unprecedented level by the youngsters of this country. These are the major

substitutes for the mobile telephony. Maybe this is on of the reasons why the major

service providers also have their presence in internet service. Idea’s strategyIdea

is not the market leader in India. They were operating in a few circles earlier and

were considered a regional player. Recently Idea started operations in many states

as part of their national roll out plan and they have operations in 2200 towns in

India. Idea has been focusing on value added services (VAS) from its inception

which is reflected in its products. They have always taken extra care in providing

customer friendly and competitive Pre Paid offerings. Differentiation and

innovation can be associated with Idea right from its beginning. It’s clear from

the following:

Power', ‘2 Minutes Outgoing Free’, ‘Lifelong offer’, ‘Women'sCard’,

'Lifetime Idea'etc are some of the offerings of IDEA.

first cellular company to launch music messaging with 'Cellular

Jockey','Background Tones', 'Group Talk',a voice portal with 'Say IDEA'and a

complete suite of Mobile EmailServices.

are also providing GPRS and EDGE services for transferring data.

new product introduced by IDEA is the EDGE enabled USB Data Card which is

50.

50

named as 'NetSetter'.Initially ‘NetSetter’ was offered to post paid customers

only. Now it is available to prepaid customers in selected circles.

partnership with IIFA for 10th Anniversary Awards, its association with

Mumbai Indians in IPL and major sought after programs in television like MTV

Roadies and Idea Star singerclearly shows its marketing strategies. They always

seek something different and is always in touch with the youth of the country as

they easily switch to other services.

ad campaign showing AbhishekBachanin different settings but all clearly

showing their corporate social responsibility is great. Their approach is different

from others. was the first to provide one rupee STD calls in the country.

Now when every one else gives per second billing and also 50 paisaper minute,

Idea offers at 49 paisaper minute.

As far as Idea is concerned it should not start a price war with Vodafone and other

large players in the industry. This is because Vodafone has a lot ofmoney with

them to suffer the losses and eventually emerge as the winner and it is almost

doing that. Idea can only afford to come out with some differentiated tariff plan

that does not result in a war with the leaders like Airtel and Vodafone. Indian

telecom is already in trouble with the lowest tariff in the world. Differentiation and

innovation is the way forward for Idea in this already bleeding industry, otherwise

it will be a severe bloodshed.

51.

51

Growth in InstalledCapacity

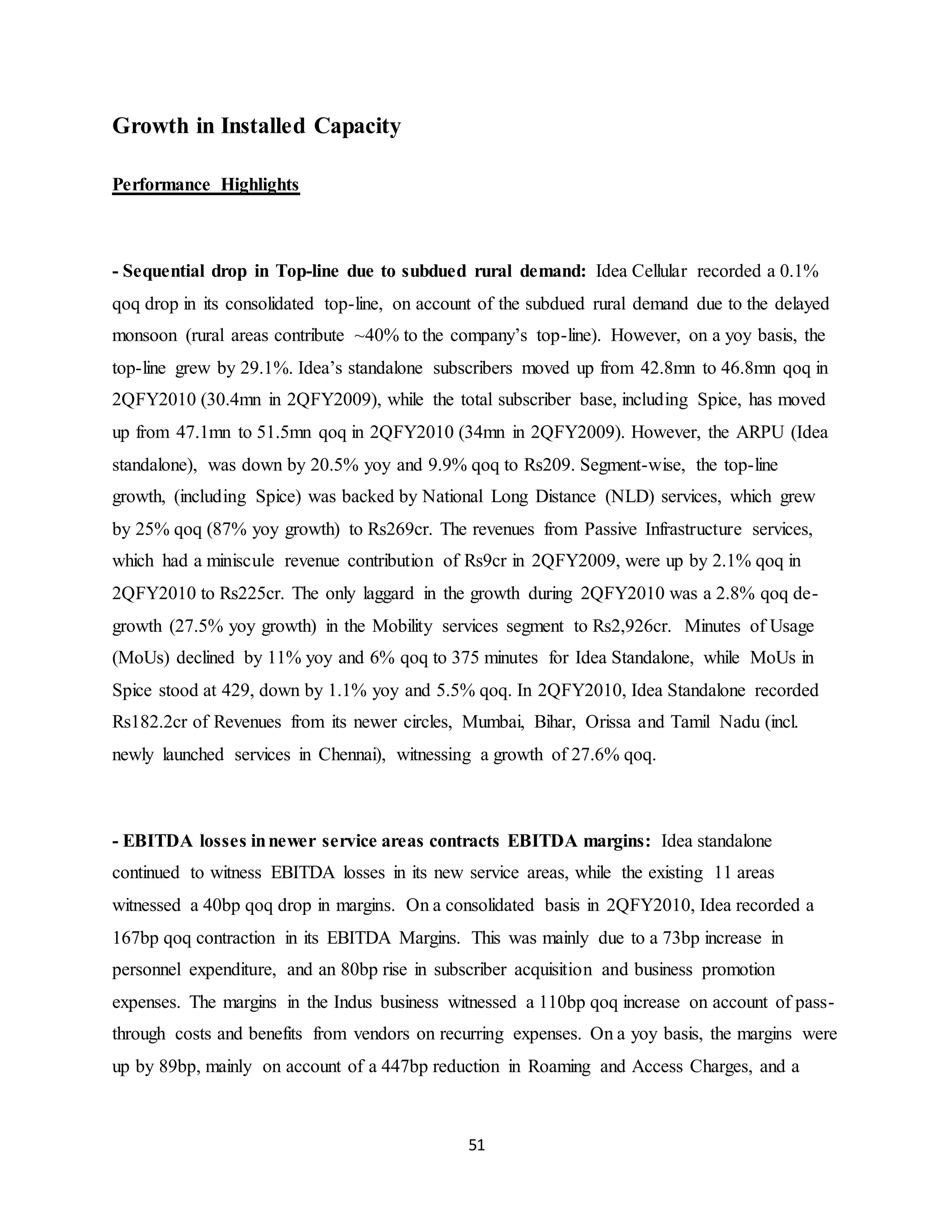

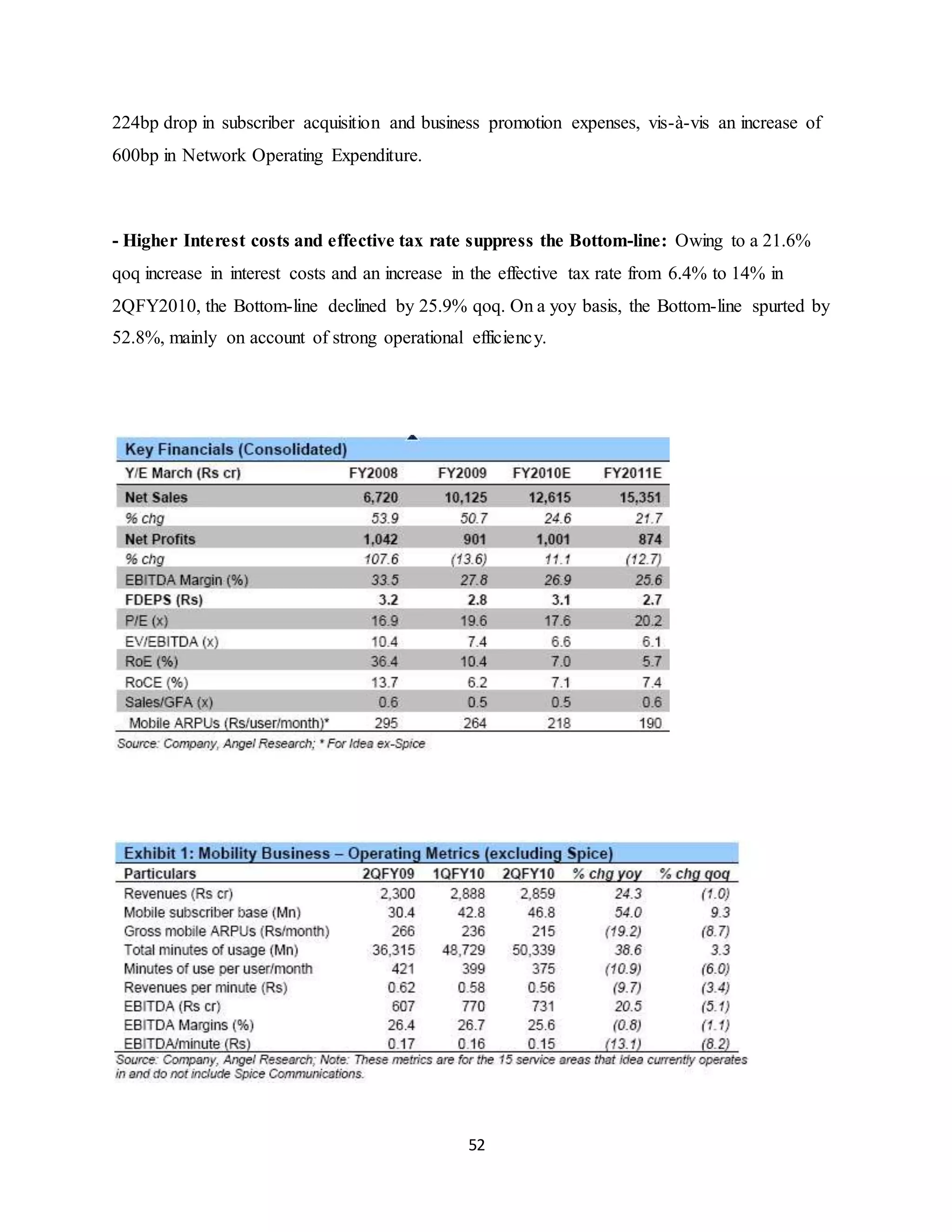

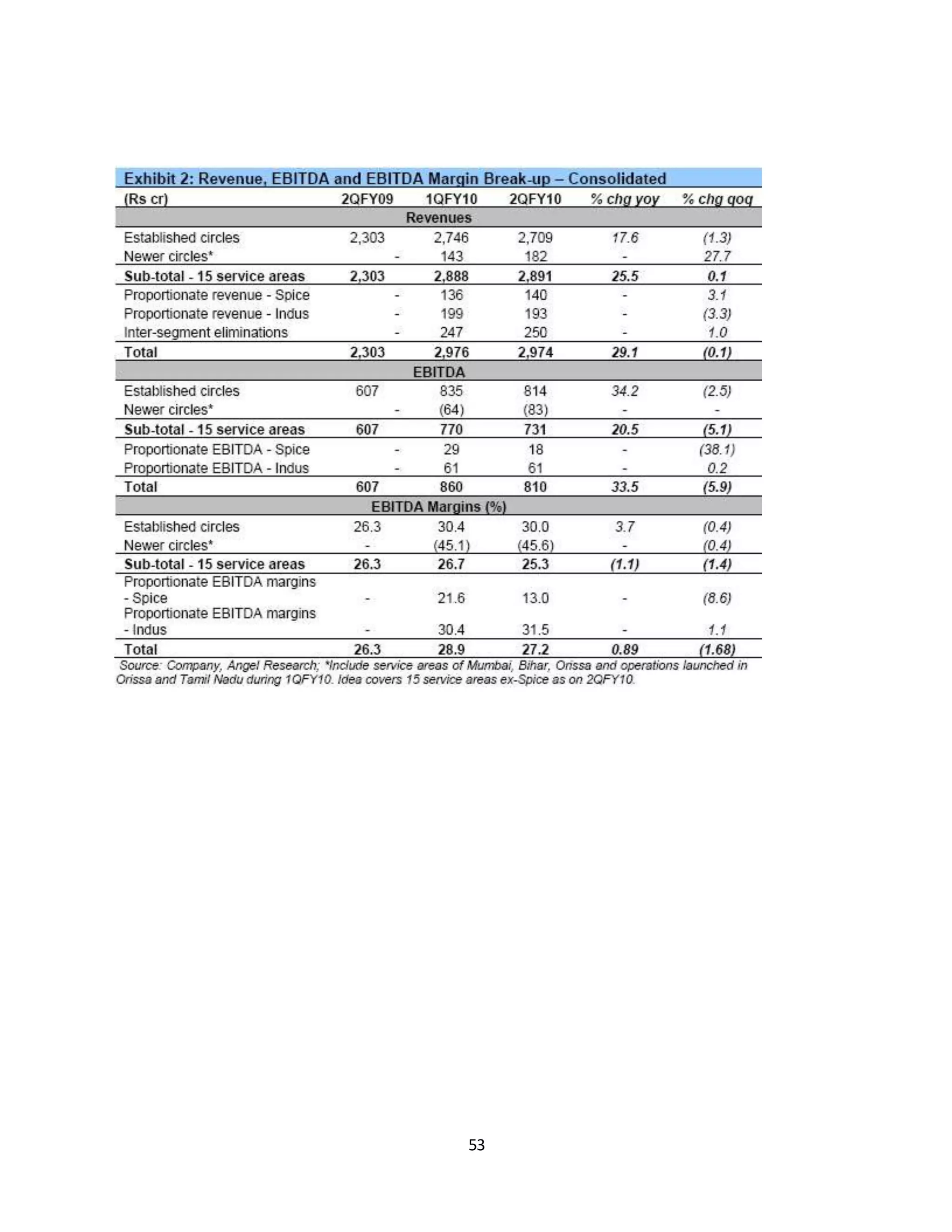

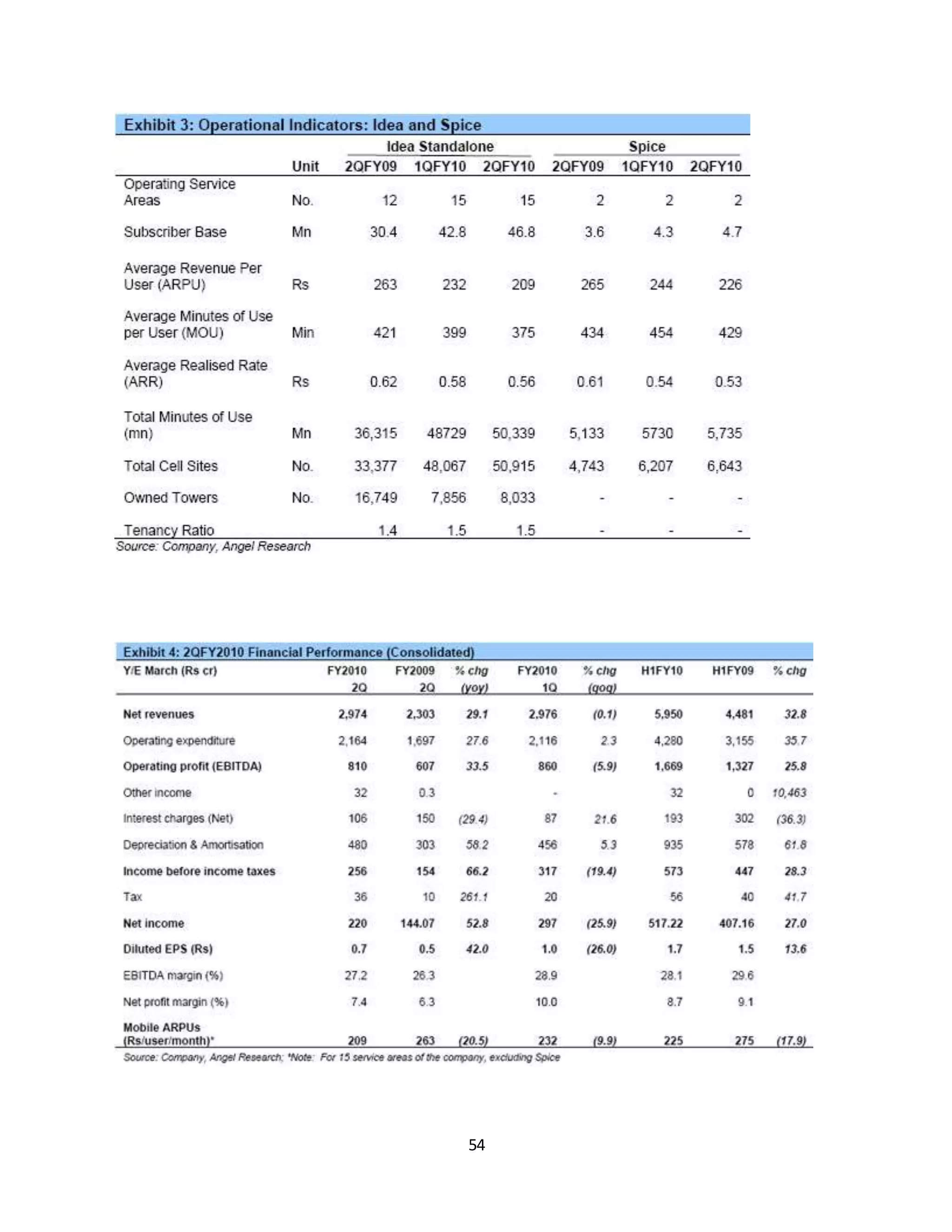

Performance Highlights

- Sequential drop in Top-line due to subdued rural demand: Idea Cellular recorded a 0.1%

qoq drop in its consolidated top-line, on account of the subdued rural demand due to the delayed

monsoon (rural areas contribute ~40% to the company’s top-line). However, on a yoy basis, the

top-line grew by 29.1%. Idea’s standalone subscribers moved up from 42.8mn to 46.8mn qoq in

2QFY2010 (30.4mn in 2QFY2009), while the total subscriber base, including Spice, has moved

up from 47.1mn to 51.5mn qoq in 2QFY2010 (34mn in 2QFY2009). However, the ARPU (Idea

standalone), was down by 20.5% yoy and 9.9% qoq to Rs209. Segment-wise, the top-line

growth, (including Spice) was backed by National Long Distance (NLD) services, which grew

by 25% qoq (87% yoy growth) to Rs269cr. The revenues from Passive Infrastructure services,

which had a miniscule revenue contribution of Rs9cr in 2QFY2009, were up by 2.1% qoq in

2QFY2010 to Rs225cr. The only laggard in the growth during 2QFY2010 was a 2.8% qoq de-

growth (27.5% yoy growth) in the Mobility services segment to Rs2,926cr. Minutes of Usage

(MoUs) declined by 11% yoy and 6% qoq to 375 minutes for Idea Standalone, while MoUs in

Spice stood at 429, down by 1.1% yoy and 5.5% qoq. In 2QFY2010, Idea Standalone recorded

Rs182.2cr of Revenues from its newer circles, Mumbai, Bihar, Orissa and Tamil Nadu (incl.

newly launched services in Chennai), witnessing a growth of 27.6% qoq.

- EBITDA losses innewer service areas contracts EBITDA margins: Idea standalone

continued to witness EBITDA losses in its new service areas, while the existing 11 areas

witnessed a 40bp qoq drop in margins. On a consolidated basis in 2QFY2010, Idea recorded a

167bp qoq contraction in its EBITDA Margins. This was mainly due to a 73bp increase in

personnel expenditure, and an 80bp rise in subscriber acquisition and business promotion

expenses. The margins in the Indus business witnessed a 110bp qoq increase on account of pass-

through costs and benefits from vendors on recurring expenses. On a yoy basis, the margins were

up by 89bp, mainly on account of a 447bp reduction in Roaming and Access Charges, and a

52.

52

224bp drop insubscriber acquisition and business promotion expenses, vis-à-vis an increase of

600bp in Network Operating Expenditure.

- Higher Interest costs and effective tax rate suppress the Bottom-line: Owing to a 21.6%

qoq increase in interest costs and an increase in the effective tax rate from 6.4% to 14% in

2QFY2010, the Bottom-line declined by 25.9% qoq. On a yoy basis, the Bottom-line spurted by

52.8%, mainly on account of strong operational efficiency.

55

Outlook and Valuation

Inaddition to the five newer service areas, Idea has recently expanded to the service areas of

Jammu & Kashmir, Kolkata & West Bengal, and North East & Assam. It now covers a total of

18 service areas, which will contribute to revenues from 3QFY2010 onwards. This move is in

line with the company’s expansion plan to garner a pan-India presence, for seizing upcoming

opportunities, like the demand in Broadband services, Value Added Services and the

forthcoming 3G auction, once the regulatory and pricing environment in the Indian Telecom

Sector stabilises. Hence, the company’s operational expense is expected to be on the higher side

in the coming quarters, as it focuses on brand-building and high-end technology to match up with

the growing demand, and for increasing its coverage in rural areas. For these initiatives, Idea has

planned a capex of Rs45bn in FY2010.

Going forward, we expect Idea Cellular to record a CAGR of 23% in its consolidated Top-line

over FY2009-11E, while the Bottom-line is expected to record a CAGR de-growth of 1.5% over

the same period. We estimate the company’s mobile subscriber base (excluding Spice) to post a

CAGR of 32% over FY2009-11E and to touch 67.9mn, while including Spice, the subscriber

base is estimated to post a CAGR of 31.4% to touch 74.3mn. We estimate blended ARPUs (ex-

Spice) to post a CAGR decline of 15% to Rs190.4 by FY2011E. At the CMP, the stock is trading

at a P/E of 20.2x FY2011E EPS and an EV/EBITDA of 6.1x FY2011E EBITDA.

On account of the significant headwinds being faced by the Indian Telecom Sector in general,

and little scope of an improvement in the near-term profitability of Idea in particular (with an

increase in the opex and capex), we believe that the company is currently trading at expensive

valuations. Hence, we maintain a Reduce on the stock, with a Target Price of Rs49. We have

valued Idea’s core business at Rs27 and have valued the Tower business (16% stake in Indus) at

Rs22 per share, based on our DCF estimates.

56.

56

ACCUMULATE

Performance Highlights PriceRs43 „ Top-line soars on strong subscriberadds,Spice consolidation: Idea Cellular

recorded a strong 59.6% yoy and 18.5% qoq growth in consolidated Target Price Rs48 Top-line in 3QFY2009 driven by

an increase in its mobile subscriberbase, which grew by an impressive 62.4% yoy and 12.6% qoq.At the end of

Investment Period 12months

3QFY2009, Idea had a mobile subscriber base of 34.2mn, recording net adds of 3.8mn over the quarter. Including

Spice, the company’s subscriber Stock Info

base stands at 38mn. Gross mobile average revenues per user (ARPUs, ex-Spice) rose 1.6% qoq (fall of 5.7% yoy)

to Rs271 (Rs266 in 2QFY2009, Sector Telecom

Rs287 in 3QFY2008). The sequential rise in ARPUs was due to higher Market Cap (Rs cr) 13,299 in-roaming Revenues.

Spice ARPUs rose 8% qoq to Rs279 (Rs259 in 2QFY2009). Part of the Revenue growth was due to consolidation of

Spice Beta 1.0

with effect from October 16, 2008 (proportionate basis,with 41.09% stake) and proportionate Revenues from Indus

Towers.

52 WK High / Low129 / 34

Minutes of Usage (MoUs) declined 1.7% qoq to 410 minutes per user per Avg Daily Volume 1948137

month. On a yoy basis,however, this metric grew by a decent 8.8%. Thus, Face Value (Rs) 10 the MoU fall

sequentially led to rise in realisations, with Revenues per Minute (RPMs) increasing 3.2% qoq, even as they fell by

over 13% on a yoy basis. BSE Sensex 8,674 In 3QFY2009, the company launched operations in the Bihar circle and full

impact of the Mumbai launch was also absorbed.These circles recorded Nifty 2,679

Rs48.3cr of Revenues.Top-line for the 13 service areas of the company (ex-Spice) grew by a robust 53.2% yoy and

13.9% qoq.BSE Code 532822

NSE Code IDEA „ Margins fall on expansion, higher rental sites and Access Charges: In 3QFY2009, Idea recorded a

significant 777bp yoy and 81bp qoq contraction Reuters Code IDEA.BO in EBITDA Margins. Network Expansion costs

rose, as a percentage of Sales, by 513bp yoy and by 270bp qoq.This quarter, the number of BloombergCode IDEA@IN

57.

57

rent-paying sites forIdea rose by 146% yoy to 21,459 (8,721 in 3QFY2008). ShareholdingPattern(%) This led to the

significant rise in Network Expenses. Roaming & Access Charges also rose by 148bp yoy, as a percentage of Sales

(7bp qoq). Promoters EBITDA losses of158.4% (Rs76.5cr) in the Mumbai and Bihar circles also 49.1

adversely impacted the company’s Margin profile.

MF/Banks/IndianFIs

6.7 „ Lower Margins, higher Depreciation reduce Bottom-line: Owing to FII/ NRIs/ OCBs Margin contraction and

higher Depreciation (up 72.9% yoy), Idea’s 40.1

Bottom-line for the quarter declined 7.3% yoy. However, on a qoq basis, Indian Public/Others 4.1 strong growth of

52.3% was recorded due to lower Net Interest Costs (down 42% qoq) due to Rs179.4cr of Interest Income recorded.

Abs. 3m 1yr 3yr*

Key Financials (Consolidated)

Sensex (%) (11.2) (50.7) (32.7) Y/E March (Rs cr) FY2007 FY2008 FY2009E FY2010E Net Sales 4,366 6,720 10,094

14,451 Idea Cellular (%) (3.5) (61.3) (49.9)

% chg 47.2 53.9 50.2 43.2 * Since listing on March 9, 2007

Net Profit 502 1,042 804 909

% chg 148.2 107.6 (22.8) 13.0 Harit Shah

EBITDA Margin (%) 33.6 33.5 26.7 25.1

FDEPS (Rs) 1.6 3.2 2.5 2.8 Tel: 022 – 4040 3800 Ext: 345

P/E (x) 27.6 13.3 17.2 15.3 e-mail: harit.shah@angeltrade.com

EV/EBITDA (x) 10.7 8.6 5.3 4.3 RoE (%) 30.3 36.4 10.5 7.4

RoCE (%) 18.4 19.8 12.2 17.1 Sales/GFA (x) 0.6 0.6 0.6 0.7

Mobile ARPUs (Rs/user/month)340 295 257 247

Source: Company, Angel Research

January 23, 2009 1

58.

58

Idea Cellular

Telecom

Subscriber growthdrives Top-line; first quarter of Spice consolidation

In 3QFY2009, Idea Cellular recorded a strong 59.6% yoy and an impressive 18.5% qoq

growth in consolidated Top-line primarily driven by growth in the company’s mobile subscriberbase, which grew

62.4% yoy and 12.6% qoq to 34.2mn. Over the year, Idea added 13.1mn mobile subscribers,while over the quarter

it added 3.8mn subscribers,implying monthly net adds of 1.3mn. Gross mobile ARPUs fell by 5.7% yoy but rose

1.6%

qoq to Rs271 (Rs287 in 3QFY2008 and Rs266 in 2QFY2009).

This was the first quarter of consolidation of Spice with the company. The consolidation is with effect from October

16, 2008. At the end of the quarter, Idea held 41.09% stake in Spice Communications, with the balance holding

distributed amongst Telecom Malaysia International (TMI) and Green Acre, an affiliate. Proportionate consolidation

of Indus

Towers was also done, with proportionate Revenues from joint ventures at Rs127.3cr. This

boosted Top-line. Excluding this, Revenues from its 13 service areas (including Mumbai

and Bihar) grew 53.2% yoy and 13.9% qoq.Mumbai and Bihar recorded Rs48.3cr in Top-line and ended the

quarter with 3.3 lakh and 2.7 lakh subscribers,respectively. At the end of 3QFY2009, Idea’s marketshare in its

circles of operations stood at 17.6% v/s 17.2% at the end of 2QFY2009 and 17.3% at the end of 3QFY2008.

59.

59

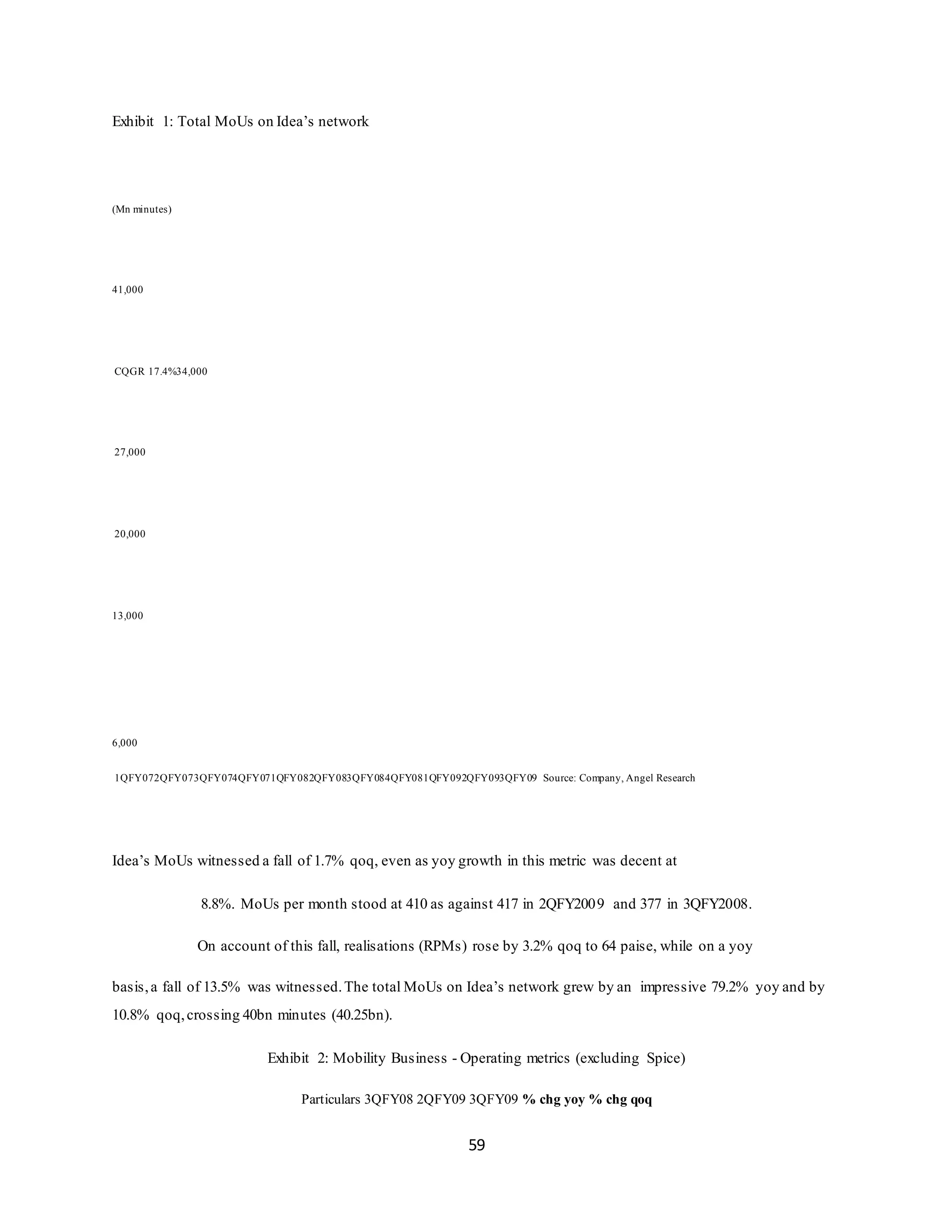

Exhibit 1: TotalMoUs on Idea’s network

(Mn minutes)

41,000

CQGR 17.4%34,000

27,000

20,000

13,000

6,000

1QFY072QFY073QFY074QFY071QFY082QFY083QFY084QFY081QFY092QFY093QFY09 Source: Company, Angel Research

Idea’s MoUs witnessed a fall of 1.7% qoq, even as yoy growth in this metric was decent at

8.8%. MoUs per month stood at 410 as against 417 in 2QFY2009 and 377 in 3QFY2008.

On account of this fall, realisations (RPMs) rose by 3.2% qoq to 64 paise, while on a yoy

basis,a fall of 13.5% was witnessed.The total MoUs on Idea’s network grew by an impressive 79.2% yoy and by

10.8% qoq,crossing 40bn minutes (40.25bn).

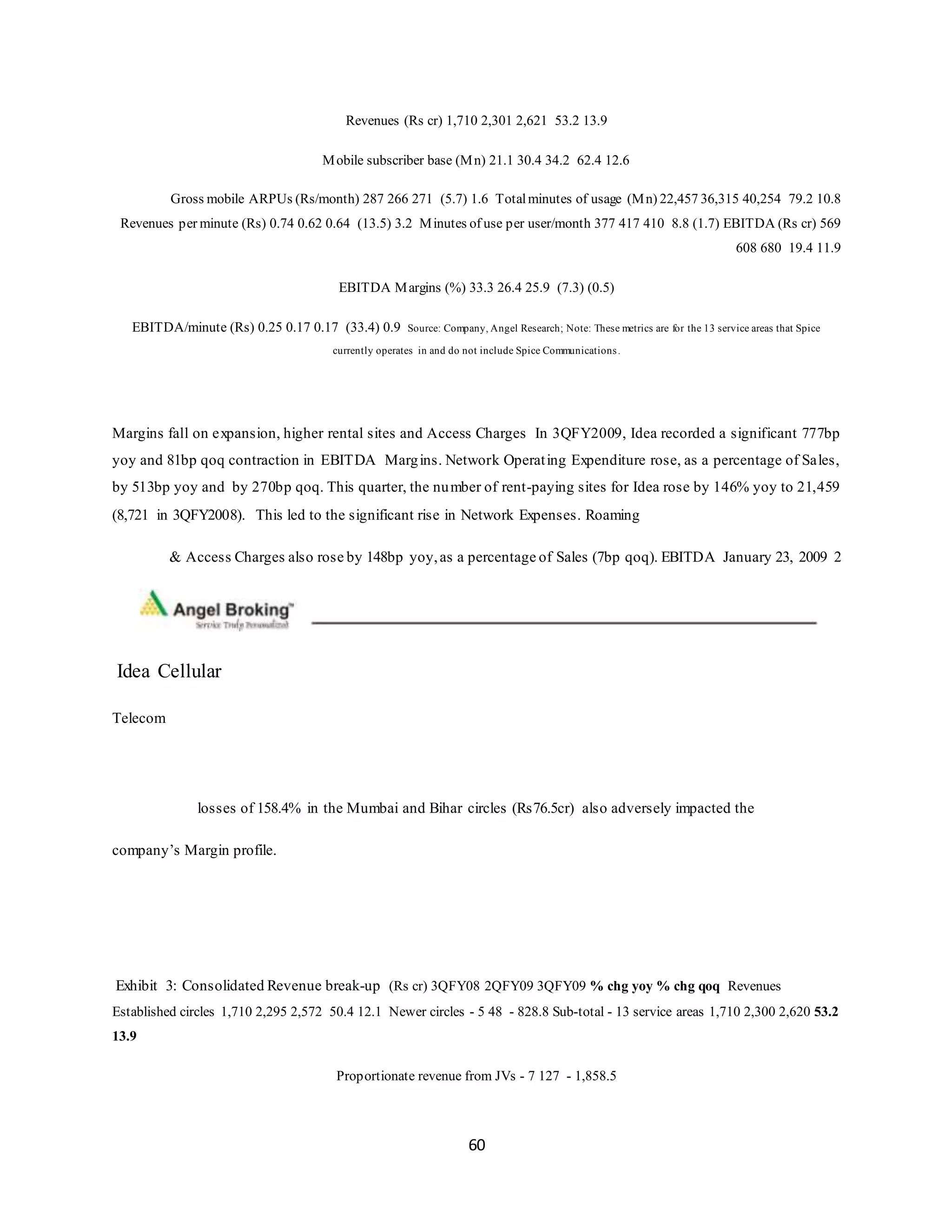

Exhibit 2: Mobility Business - Operating metrics (excluding Spice)

Particulars 3QFY08 2QFY09 3QFY09 % chg yoy % chg qoq

60.

60

Revenues (Rs cr)1,710 2,301 2,621 53.2 13.9

Mobile subscriber base (Mn) 21.1 30.4 34.2 62.4 12.6

Gross mobile ARPUs (Rs/month) 287 266 271 (5.7) 1.6 Totalminutes of usage (Mn) 22,457 36,315 40,254 79.2 10.8

Revenues per minute (Rs) 0.74 0.62 0.64 (13.5) 3.2 Minutes of use per user/month 377 417 410 8.8 (1.7) EBITDA (Rs cr) 569

608 680 19.4 11.9

EBITDA Margins (%) 33.3 26.4 25.9 (7.3) (0.5)

EBITDA/minute (Rs) 0.25 0.17 0.17 (33.4) 0.9 Source: Company, Angel Research; Note: These metrics are for the 13 service areas that Spice

currently operates in and do not include Spice Communications.

Margins fall on expansion, higher rental sites and Access Charges In 3QFY2009, Idea recorded a significant 777bp

yoy and 81bp qoq contraction in EBITDA Margins. Network Operating Expenditure rose, as a percentage of Sales,

by 513bp yoy and by 270bp qoq. This quarter, the number of rent-paying sites for Idea rose by 146% yoy to 21,459

(8,721 in 3QFY2008). This led to the significant rise in Network Expenses. Roaming

& Access Charges also rose by 148bp yoy,as a percentage of Sales (7bp qoq). EBITDA January 23, 2009 2

Idea Cellular

Telecom

losses of 158.4% in the Mumbai and Bihar circles (Rs76.5cr) also adversely impacted the

company’s Margin profile.

Exhibit 3: Consolidated Revenue break-up (Rs cr) 3QFY08 2QFY09 3QFY09 % chg yoy % chg qoq Revenues

Established circles 1,710 2,295 2,572 50.4 12.1 Newer circles - 5 48 - 828.8 Sub-total - 13 service areas 1,710 2,300 2,620 53.2

13.9

Proportionate revenue from JVs - 7 127 - 1,858.5

61.

61

Inter-segment eliminations -3 17 - 402.9

Total 1,710 2,303 2,731 59.7 18.5

EBITDA

Established circles 569 644 756 32.9 17.4 Newer circles - (37) (77) - - Sub-total - 13 service areas 569 608 680 19.4 11.9

ProportionateEBITDA from JVs - (1) 17 - - Total569 606 697 22.4 14.9 EBITDA Margins (%)

Established circles 33.3 28.1 29.4 (3.9) 1.3

Newer circles - (703.8) (158.4) - 545.5

Sub-total - 13 service areas 33.3 26.4 25.9 (7.3) (0.5)

Proportionate JV EBITDA margins - (20.0) 13.3 - 33.3

Total 33.3 26.3 25.5 (7.8) (0.8) Source: Company, Angel Research

Lower Margins, higher Depreciation reduce Bottom-line

Owing to Margin contraction and higher Depreciation (up 72.9% yoy), Idea’s Bottom-line for the quarter declined

7.3% yoy. However, qoq, strong growth of 52.3% was recorded due to lower Net Interest Costs (down 42% qoq)

due to Rs179.4cr of Interest Income earned from investment of the funds raised by the company recently.

Receives GSM spectrumfor all circles

Idea Cellular has received GSM spectrum across all the circles where it hitherto had

licences to operate but had no spectrum. Thus,the company will roll out operations in these circles over the course

of the next few months and is well on course to become a pan-India GSM-based cellular operator. However, being a

late entrant in circles like Orissa (to launch in 1QFY2010), Tamil Nadu (2QFY2010 launch scheduled)and West

Bengal, the company

could face ARPU and EBITDA pressures in these circles as it launches and gains scale.

62.

62

Issues 1.925mn CompulsorilyConvertible Preference Shares to Providence affiliate Idea Cellular on December 5,

2008 received Rs2,100cr from an affiliate of Providence Equity Partners by way of subscription to 1.925mn

Compulsorily Convertible Preference Shares, which will be converted into 16.14% of the equity capital of Aditya

Birla Telecom

(ABTL) post conversion.

Signs IRU with Indus Towers to transfer 11,100 towers; to impact Margins by 4-5% Idea Cellular has signed an

Indefeasible Right to Use (IRU) agreement with Indus Towers, the tower joint venture (JV) between itself, Bharti

and Vodafone involving the transfer of 11,100 of its towers to Indus, each of which will have one cell site for Idea.

Thus, out of the

balance of 17,830 towers that were until now non-rent paying, 11,100 will become

rent-paying on the books of Indus. The approximate book value of these towers is

Rs1,450cr.

This will lead to a significantly higher component of rent-paying towers for Idea and capex will get converted into

opex. There will be a 4-5% impact on EBITDA Margins in FY2010 on

account of this. However, lower Depreciation and Interest costs will offset the impact to an

extent on the Bottom-line. Moreover, with consolidation of 16% of Indus, the impact is likely

to be limited to around 2-2.5% at the Net Profit level.

January 23, 2009 3

63.

63

Idea Cellular

Telecom

Outlook andValuation

Going forward, we expect Idea Cellular to record a CAGR of 46.3% in Top-line over FY2008-10E, while Bottom-

line is expected to record a CAGR fall of 7.5% over the period

on account of significant Margin pressures. We estimate the company’s mobile subscriber

base (including Spice) to post a CAGR of 52.9% over FY2008-10E to 56.1mn, while ARPUs

would post a decline in CAGR of 8.4% over the period to Rs247.

At the CMP, the stock is trading at a P/E of 15.3x FY2010E EPS, EV/EBITDA of 4.3x FY2010E EBITDA and at

an EV/subscriber of US $67.5 on our FY2010E subscriber base.

We believe the company is well-positioned in terms of spectrumholdings across the

country. Strong fund infusion from recent initiatives like the stake sale in ABTL and the

Spice deal with TMI will result in a well-funded Balance Sheet and Net Debt-Equity ratio of just 0.19x. However,

the environment going forward is likely to become more difficult given intensifying competition, falling ARPUs,

cost pressures owing to rapid expansion of coverage area, leading to Margin pressures,which are likely to get

further exacerbated due

to roll outs in newer circles (higher initial EBITDA losses), which would in turn exert

significant pressure on Profitability, and regulatory risks. With RCOM’s GSM roll-out and the

upcoming GSM launches of Tata Teleservices, apart from circle expansion by Aircel (GSM) and Shyam-Sistema

(CDMA) as well as newer operator roll-outs, the competitive environment is expected to further intensify.

We downgrade our 12-month Target Price to Rs48 (Rs66), which includes Rs22 as the

64.

64

value of thecore business after downgrading the P/E multiple to 8x (10x), and Rs26 as the

value of its 16% stake in Indus Towers. We recommend an Accumulate on the stock and believe that while the

company’s recent initiatives will enable it to build a strong business in the longer-term, the increasingly difficult

environment is likely to exert significant strain on its key operating and financial parameters, thereby limiting

major upsides in the stock price.

January 23, 2009 4

Idea Cellular

Telecom

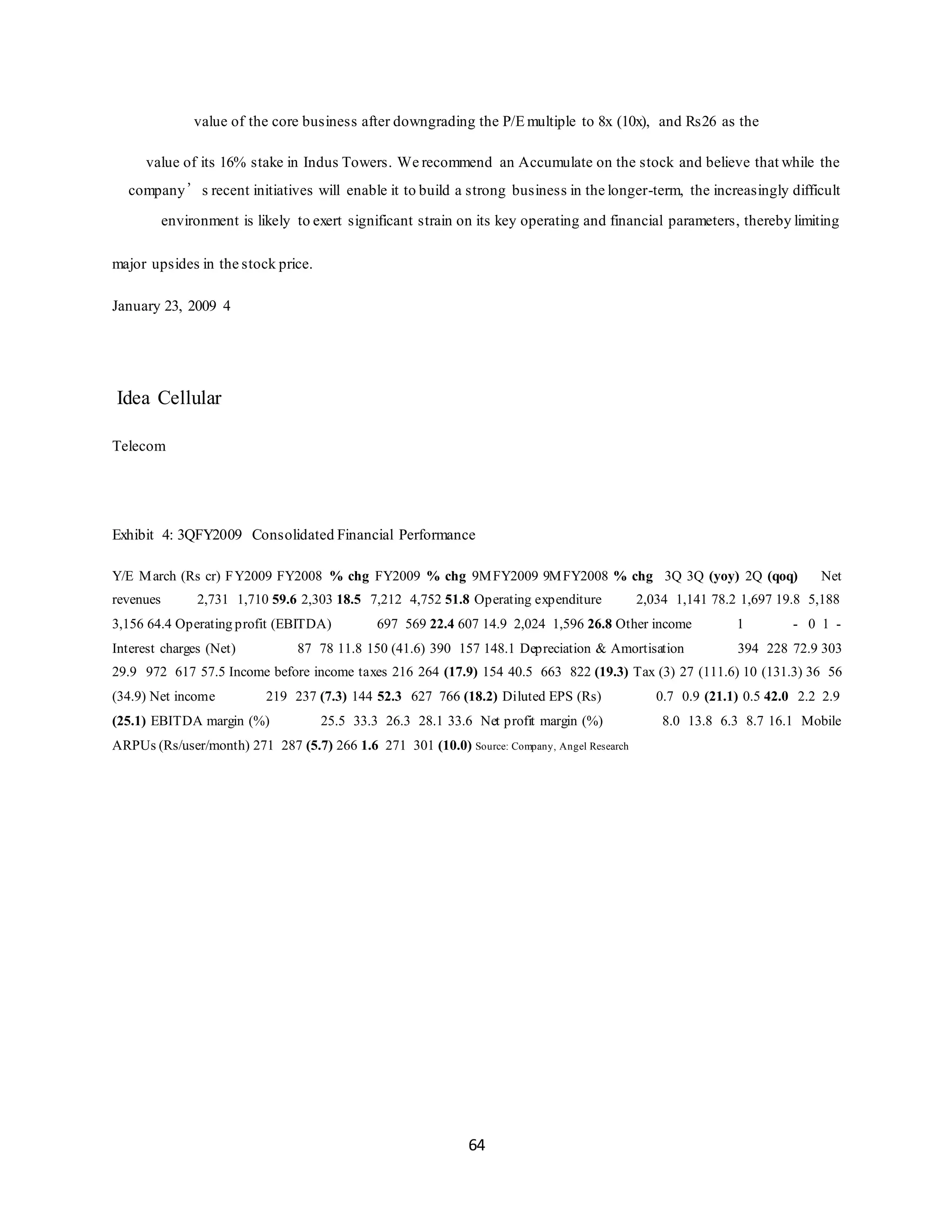

Exhibit 4: 3QFY2009 Consolidated Financial Performance

Y/E March (Rs cr) FY2009 FY2008 % chg FY2009 % chg 9MFY2009 9MFY2008 % chg 3Q 3Q (yoy) 2Q (qoq) Net

revenues 2,731 1,710 59.6 2,303 18.5 7,212 4,752 51.8 Operating expenditure 2,034 1,141 78.2 1,697 19.8 5,188

3,156 64.4 Operating profit (EBITDA) 697 569 22.4 607 14.9 2,024 1,596 26.8 Other income 1 - 0 1 -

Interest charges (Net) 87 78 11.8 150 (41.6) 390 157 148.1 Depreciation & Amortisation 394 228 72.9 303

29.9 972 617 57.5 Income before income taxes 216 264 (17.9) 154 40.5 663 822 (19.3) Tax (3) 27 (111.6) 10 (131.3) 36 56

(34.9) Net income 219 237 (7.3) 144 52.3 627 766 (18.2) Diluted EPS (Rs) 0.7 0.9 (21.1) 0.5 42.0 2.2 2.9

(25.1) EBITDA margin (%) 25.5 33.3 26.3 28.1 33.6 Net profit margin (%) 8.0 13.8 6.3 8.7 16.1 Mobile

ARPUs (Rs/user/month) 271 287 (5.7) 266 1.6 271 301 (10.0) Source: Company, Angel Research

65.

65

Growth in sales:

AdityaBirla Group

A US $28 billion corporation, the Aditya Birla Group is in the league of Fortune 500. It is a

multinational corporation based in Mumbai, India with operations in 25 countries. The group is a

major player in all the industry sectors it operates in. The Group has been adjudged the best

employer in India and among the top 20 in Asia by the Hewitt-Economic Times and Wall Street

Journal Study 2007. The origins of the group lie in the conglomerate once held by one of India's

foremost industrialists Mr. Ghanshyam Das Birla. He bequeathed most of these companies to his

grandson, Mr. Aditya Vikram Birla – the father of the current Chairman of the group, Mr. Kumar

Mangalam Birla. Mr. Kumar Mangalam Birla is the grandson of Mr. Basant Kumar Birla, who

heads his own independent business conglomerate. Several other members of the Birla Family

own and run their independent business groups.

Aditya Birla is organized into various subsidiaries that operate across different sectors. Among

these are viscose staple fibre, non-ferrous metals, cement, viscose filament yarn, branded

apparel, carbon black, chemicals, Modern retail (under the 'More' brand of supermarkets, and

also under the Trinethra, and Fabmall brands until recently), fertilizers, sponge iron, insulators,

financial services, telecom, BPO and IT services. The Group consists of four main companies,

which operate in various industry sectors through subsidiaries, joint ventures, etc. These are

Hindalco, Grasim, Aditya Birla Nuvo, and UltraTech Cement.

We have focused on the Idea Cellular SBU of Aditya Birla Group. It is One of India's leading

GSM mobile service operators; IDEA Cellular is headquartered in Mumbai and has over 30

million subscribers. Innovation is central to IDEA's Value Added Service products. It was the

first to offer 'Global SMS' in over 540 networks across all technology platforms. It has also

acquired Modi family’s Spice. But then it even faces tough competition from various major

players. The leading Mobile Networks today in India are Airtel, Vodafone (sold by Hutchinson

Essar to Vodafone), BSNL, MTNL, Orange, Aircel, Tata Indicom, Idea, BPL etc. Each of these

companies has a tough competition with one another. BSNL & MTNL being government sectors

have more advantages than other Private sector Companies.

66.

66

Strategic Business Unit-Idea Cellular Limited

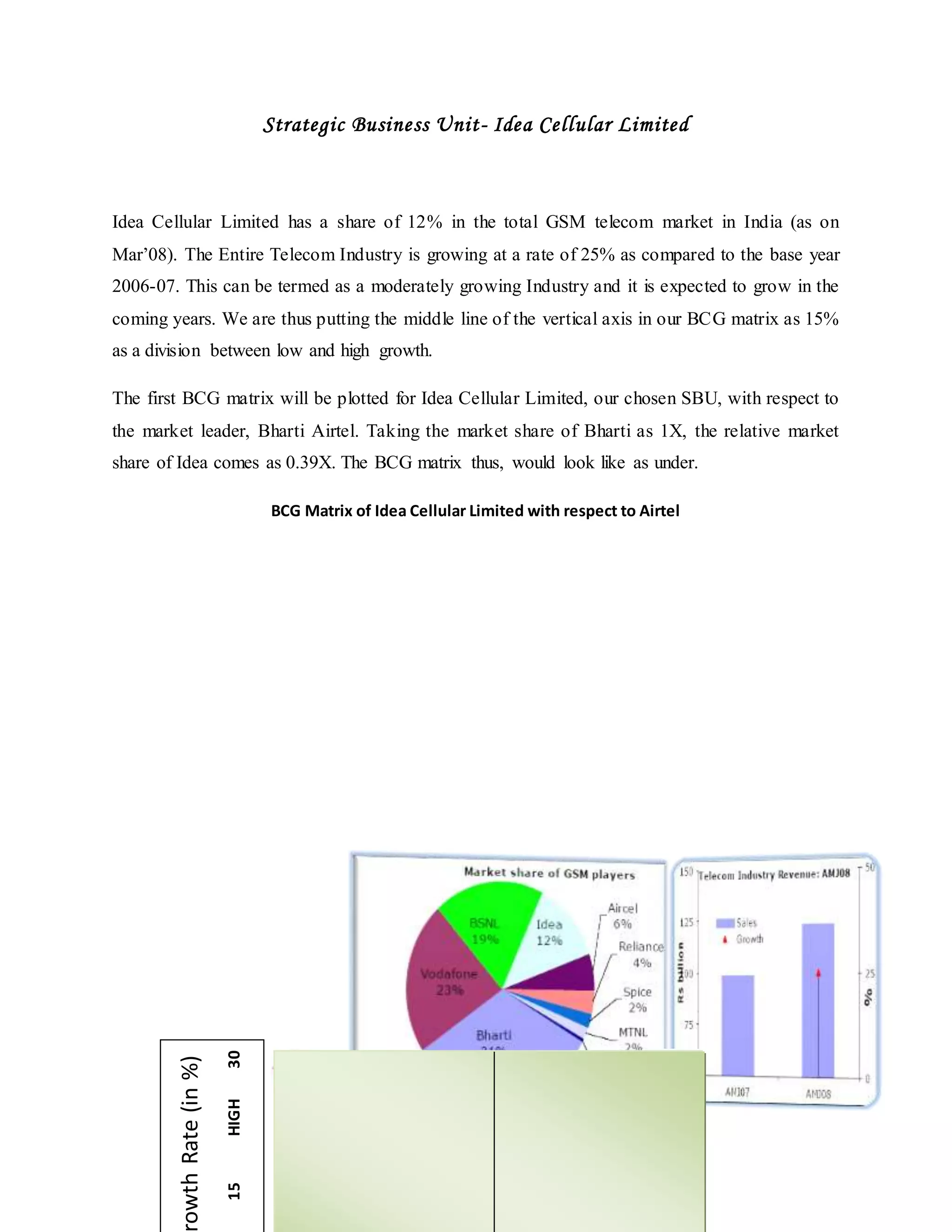

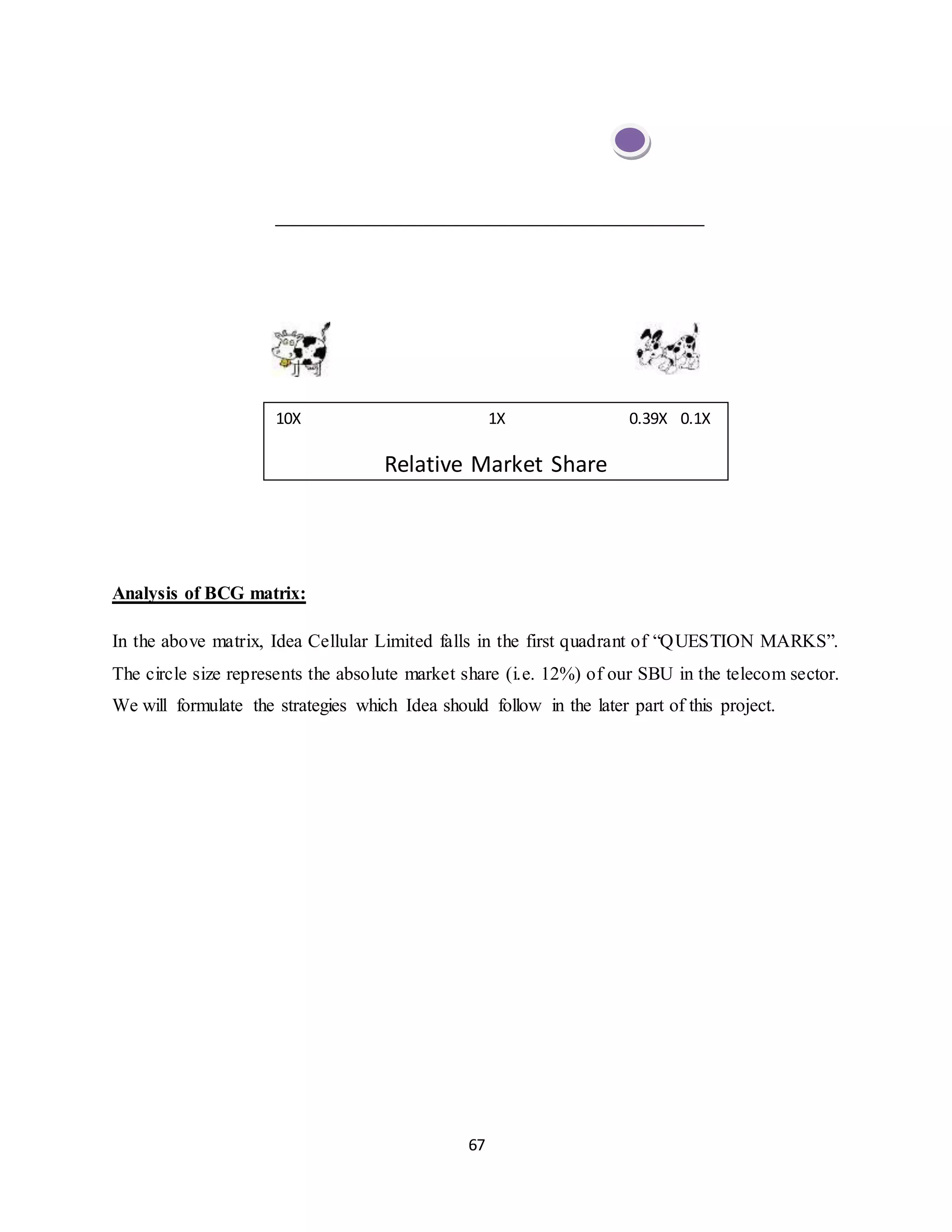

Idea Cellular Limited has a share of 12% in the total GSM telecom market in India (as on

Mar’08). The Entire Telecom Industry is growing at a rate of 25% as compared to the base year

2006-07. This can be termed as a moderately growing Industry and it is expected to grow in the

coming years. We are thus putting the middle line of the vertical axis in our BCG matrix as 15%

as a division between low and high growth.

The first BCG matrix will be plotted for Idea Cellular Limited, our chosen SBU, with respect to

the market leader, Bharti Airtel. Taking the market share of Bharti as 1X, the relative market

share of Idea comes as 0.39X. The BCG matrix thus, would look like as under.

BCG Matrix of Idea Cellular Limited with respect to Airtel

owthRate(in%)

15HIGH30

67.

67

Analysis of BCGmatrix:

In the above matrix, Idea Cellular Limited falls in the first quadrant of “QUESTION MARKS”.

The circle size represents the absolute market share (i.e. 12%) of our SBU in the telecom sector.

We will formulate the strategies which Idea should follow in the later part of this project.

10X 1X 0.39X 0.1X

Relative Market Share

68.

68

Plotting the Competitors

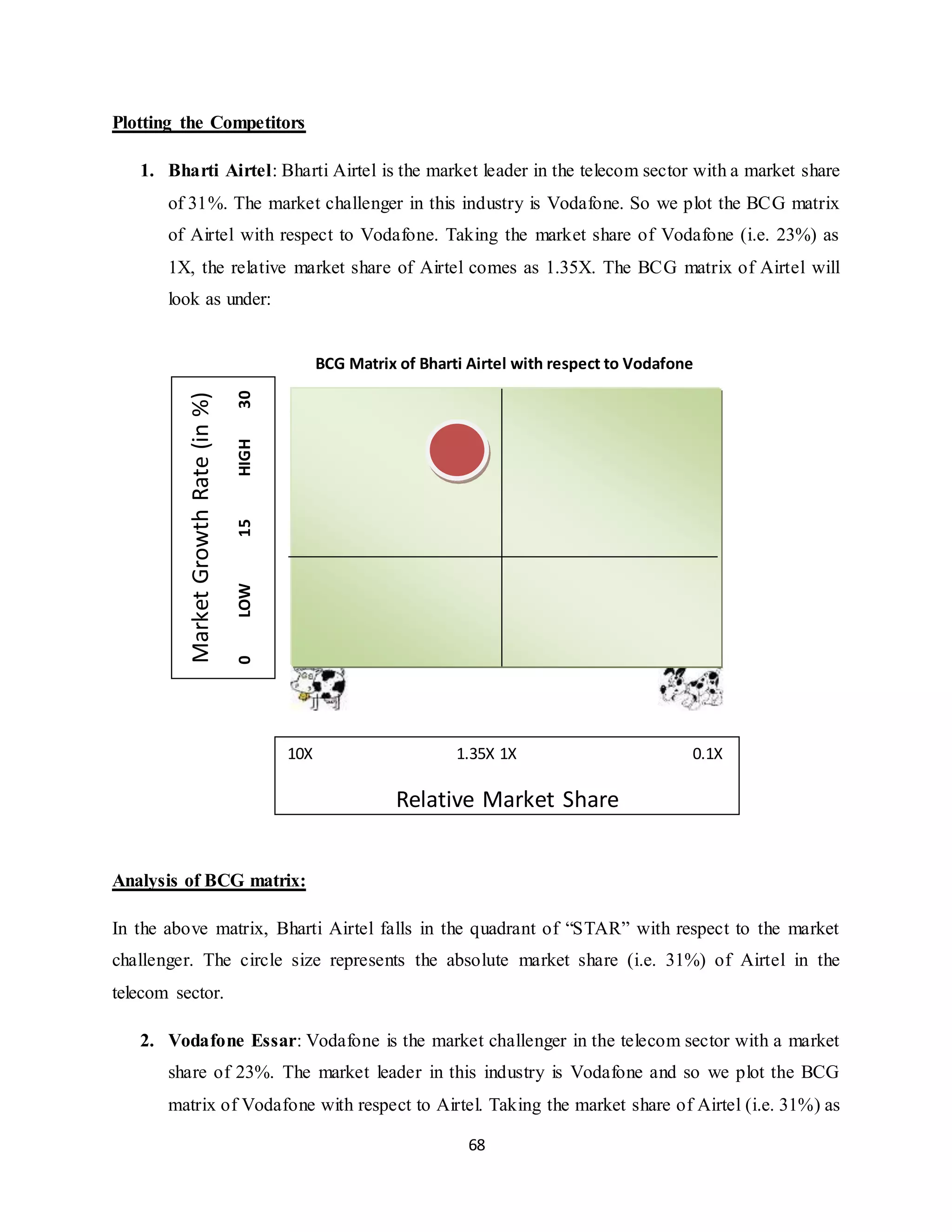

1.Bharti Airtel: Bharti Airtel is the market leader in the telecom sector with a market share

of 31%. The market challenger in this industry is Vodafone. So we plot the BCG matrix

of Airtel with respect to Vodafone. Taking the market share of Vodafone (i.e. 23%) as

1X, the relative market share of Airtel comes as 1.35X. The BCG matrix of Airtel will

look as under:

BCG Matrix of Bharti Airtel with respect to Vodafone

Analysis of BCG matrix:

In the above matrix, Bharti Airtel falls in the quadrant of “STAR” with respect to the market

challenger. The circle size represents the absolute market share (i.e. 31%) of Airtel in the

telecom sector.

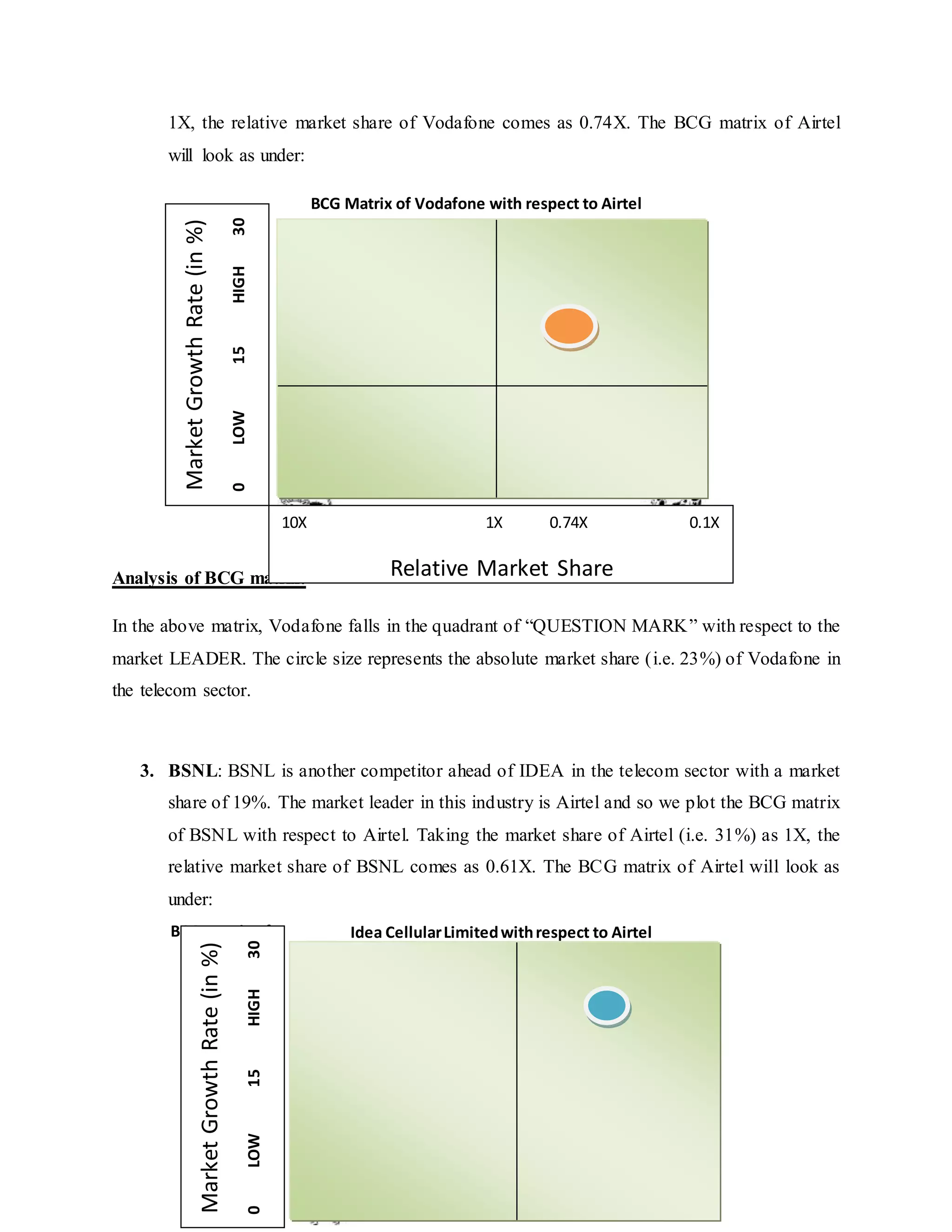

2. Vodafone Essar: Vodafone is the market challenger in the telecom sector with a market

share of 23%. The market leader in this industry is Vodafone and so we plot the BCG

matrix of Vodafone with respect to Airtel. Taking the market share of Airtel (i.e. 31%) as

MarketGrowthRate(in%)

0LOW15HIGH30

HIGH

10X 1.35X 1X 0.1X

Relative Market Share

69.

69

1X, the relativemarket share of Vodafone comes as 0.74X. The BCG matrix of Airtel

will look as under:

BCG Matrix of Vodafone with respect to Airtel

Analysis of BCG matrix:

In the above matrix, Vodafone falls in the quadrant of “QUESTION MARK” with respect to the

market LEADER. The circle size represents the absolute market share (i.e. 23%) of Vodafone in

the telecom sector.

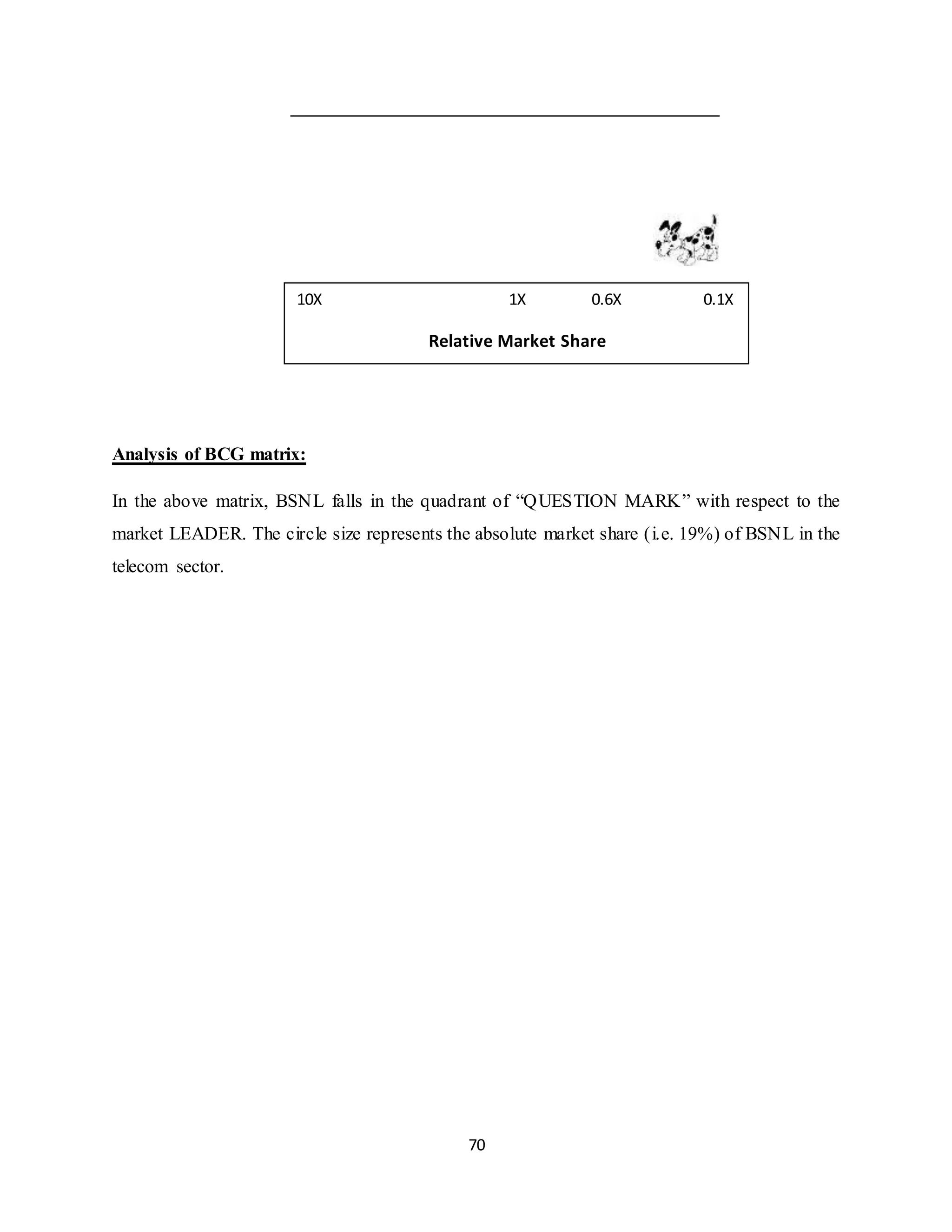

3. BSNL: BSNL is another competitor ahead of IDEA in the telecom sector with a market

share of 19%. The market leader in this industry is Airtel and so we plot the BCG matrix

of BSNL with respect to Airtel. Taking the market share of Airtel (i.e. 31%) as 1X, the

relative market share of BSNL comes as 0.61X. The BCG matrix of Airtel will look as

under:

BCG Matrix of Idea CellularLimitedwithrespect to Airtel

MarketGrowthRate(in%)

0LOW15HIGH30

HIGH

10X 1X 0.74X 0.1X

Relative Market Share

MarketGrowthRate(in%)

0LOW15HIGH30

HIGH

70.

70

Analysis of BCGmatrix:

In the above matrix, BSNL falls in the quadrant of “QUESTION MARK” with respect to the

market LEADER. The circle size represents the absolute market share (i.e. 19%) of BSNL in the

telecom sector.

10X 1X 0.6X 0.1X

Relative Market Share

71.

71

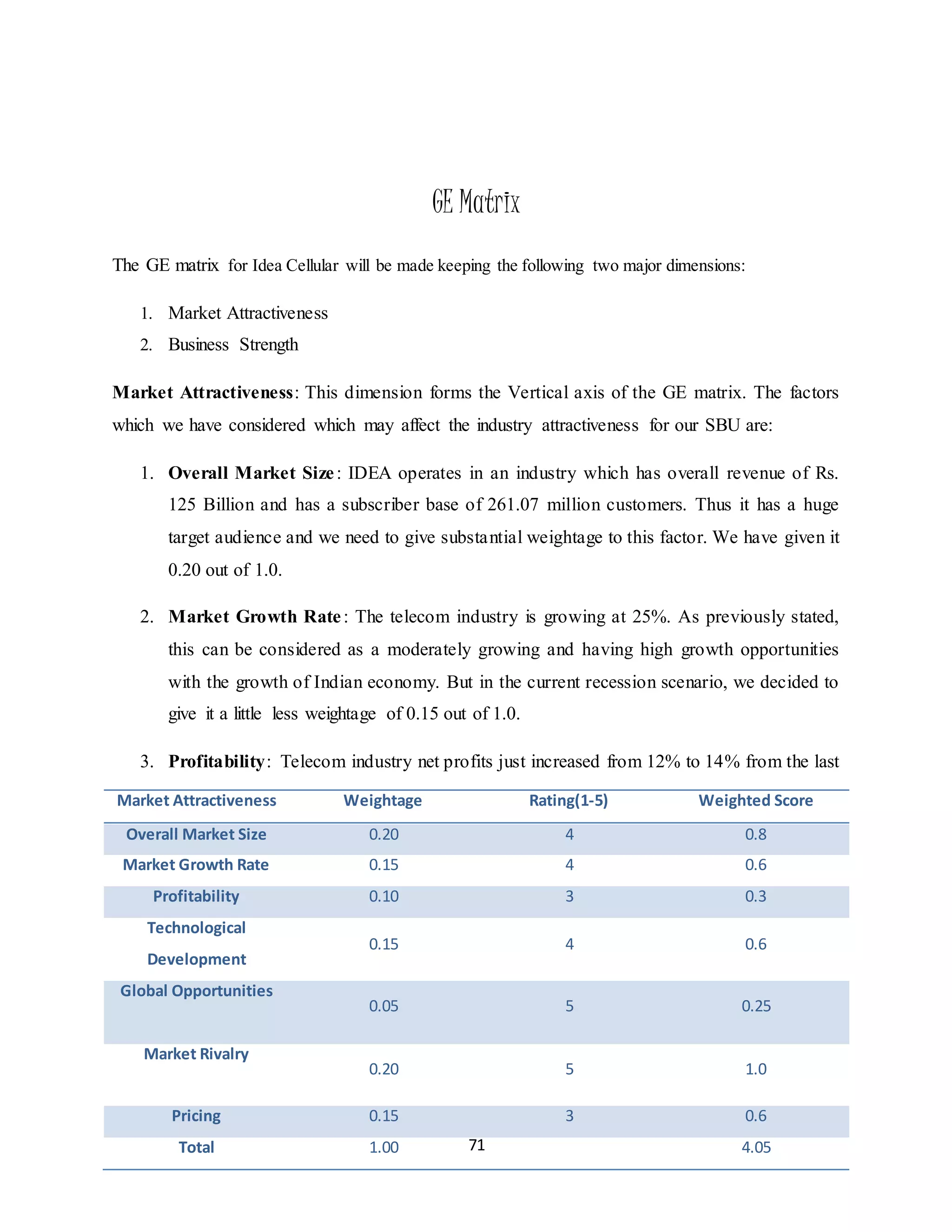

GE Matrix

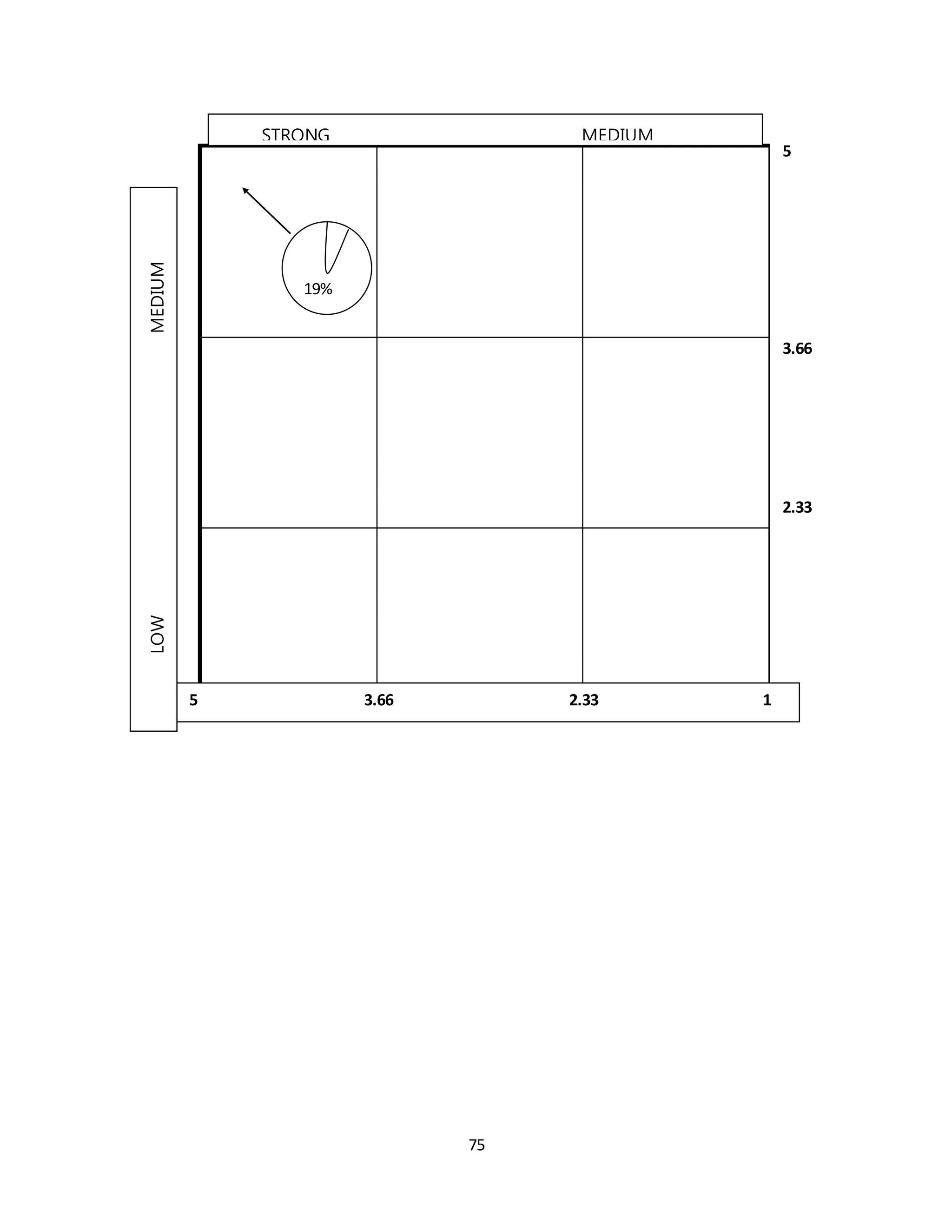

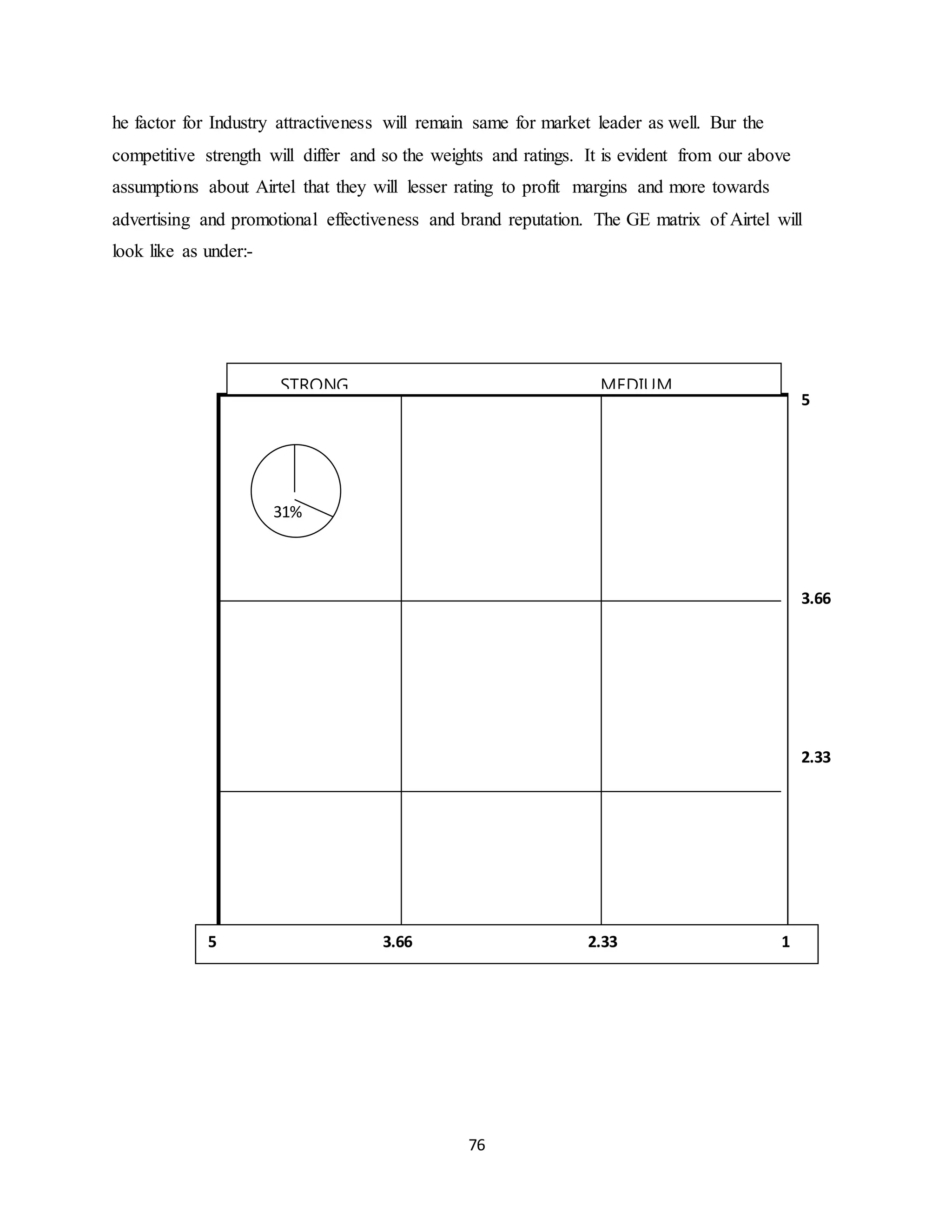

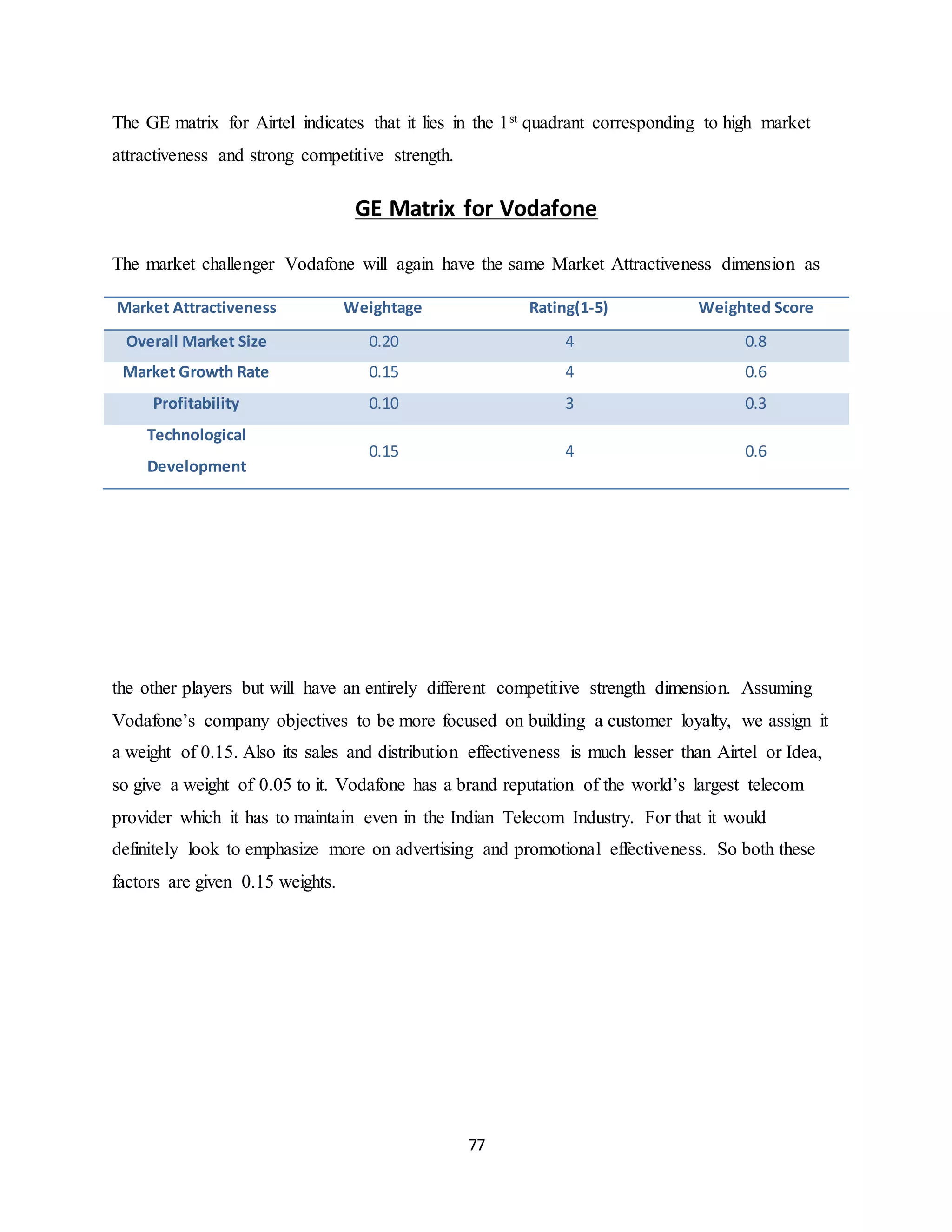

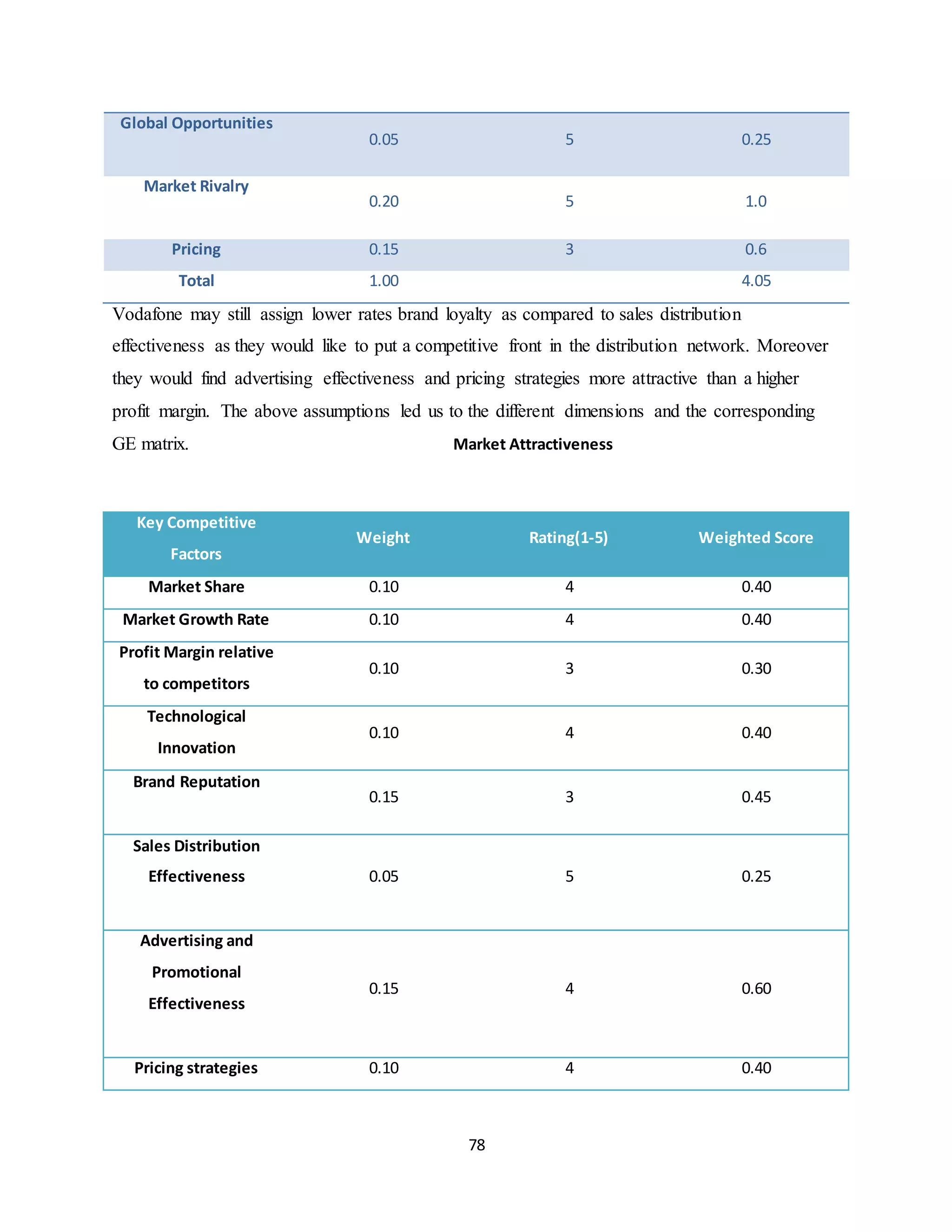

The GEmatrix for Idea Cellular will be made keeping the following two major dimensions:

1. Market Attractiveness

2. Business Strength

Market Attractiveness: This dimension forms the Vertical axis of the GE matrix. The factors

which we have considered which may affect the industry attractiveness for our SBU are:

1. Overall Market Size: IDEA operates in an industry which has overall revenue of Rs.

125 Billion and has a subscriber base of 261.07 million customers. Thus it has a huge

target audience and we need to give substantial weightage to this factor. We have given it

0.20 out of 1.0.

2. Market Growth Rate: The telecom industry is growing at 25%. As previously stated,

this can be considered as a moderately growing and having high growth opportunities

with the growth of Indian economy. But in the current recession scenario, we decided to

give it a little less weightage of 0.15 out of 1.0.

3. Profitability: Telecom industry net profits just increased from 12% to 14% from the last

Market Attractiveness Weightage Rating(1-5) Weighted Score

Overall Market Size 0.20 4 0.8

Market Growth Rate 0.15 4 0.6

Profitability 0.10 3 0.3

Technological

Development

0.15 4 0.6

Global Opportunities

0.05 5 0.25

Market Rivalry

0.20 5 1.0

Pricing 0.15 3 0.6

Total 1.00 4.05

72.

72

fiscal year. Dueto no such significant increase in profitability as compared to sales, we

have given it a weightage of 0.10 out of 1.0.