Download to read offline

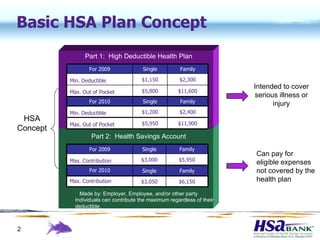

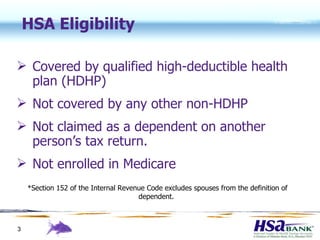

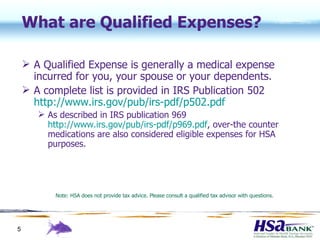

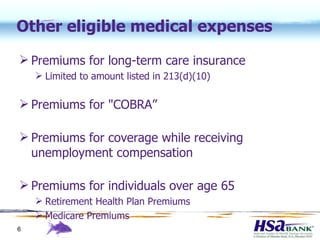

This document provides an overview of health savings accounts (HSAs), including: - HSAs are used in conjunction with high deductible health plans and can be funded by employers, employees, and others. - Contributions up to an annual maximum amount are tax-deductible and the account grows tax-free. - Funds can be withdrawn tax-free for qualified medical expenses or after age 65 for any purpose. - HSAs offer portability, tax benefits, and the potential for long-term savings if unused funds are invested.

![[Guide] The Best Introduction to Health Savings Accounts](https://cdn.slidesharecdn.com/ss_thumbnails/hsa-guide-final-150724142325-lva1-app6891-thumbnail.jpg?width=640&height=640&fit=bounds)

![The Best Introduction to Health Savings Accounts [Guide]](https://cdn.slidesharecdn.com/ss_thumbnails/hsa-guide-final-160129173610-thumbnail.jpg?width=640&height=640&fit=bounds)