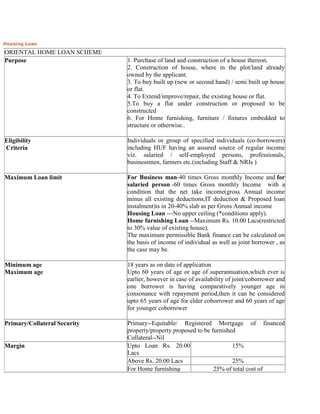

1. Housing Loan

ORIENTAL HOME LOAN SCHEME

Purpose 1. Purchase of land and construction of a house thereon.

2. Construction of house, where in the plot/land already

owned by the applicant.

3. To buy built up (new or second hand) / semi built up house

or flat.

4. To Extend/improve/repair, the existing house or flat.

5.To buy a flat under construction or proposed to be

constructed

6. For Home furnishing, furniture / fixtures embedded to

structure or otherwise..

Eligibility Individuals or group of specified individuals (co-borrowers)

Criteria including HUF having an assured source of regular income

viz. salaried / self-employed persons, professionals,

businessmen, farmers etc.(including Staff & NRIs )

Maximum Loan limit For Business man-40 times Gross monthly Income and for

salaried person -60 times Gross monthly Income with a

condition that the net take income(gross Annual income

minus all existing deductions,IT deduction & Proposed loan

instalment)is in 20-40% slab as per Gross Annual income

Housing Loan ---No upper ceiling (*conditions apply).

Home furnishing Loan --Maximum Rs. 10.00 Lacs(restricted

to 30% value of existing house),

The maximum permissible Bank finance can be calculated on

the basis of income of individual as well as joint borrower , as

the case may be.

Minimum age 18 years as on date of application

Maximum age Upto 60 years of age or age of superannuation,which ever is

earlier, however in case of availability of joint/coborrower and

one borrower is having comparatively younger age in

consonance with repayment period,then it can be considered

upto 65 years of age for elder coborrower and 60 years of age

for younger coborrower

Primary/Collateral Security Primary--Equitable/ Registered Mortgage of financed

property/property proposed to be furnished

Collateral--Nil

Margin Upto Loan Rs. 20.00 15%

Lacs

Above Rs. 20.00 Lacs 25%

For Home furnishing 25% of total cost of

2. renovation/furnishing

Rate of Interest Click here to view Rate of Interest

Concession in rate of interest to captive and loyal customers,

group of employee borrowers. (Conditions apply. )

Interest switchover option to existing During the currency of housing loan, if borrower feels that

borrowers. the current prevailing card rate of Home loan is in favour as

compared to interest actually applied in his account ,he can

use the switchover option.

Process fee 0.50% of the loan amount, subject to maximum of Rs. 20000/-

plus service tax, if any

Other Charges Prepayment Penalty / documentation charges/ upfront fee-

NIL

Repayment For Home Loan -Upto 300 months, preferably in EMI

Period including the moratorium period of 18 months

For Home Furnishing Loan-Maximum 120 months

Second home loans, takeover of home loan accounts, loan to NRI's facility is available as per the

detailed scheme.

List of Documents/ Information to be provided by the applicant along with Loan Application Form.

(These documents are indicative, relevant documents be obtained on case to case basis)

Loan application Form-cum-process note LF-2/Passport size photograph of applicant and co-applicant, ID

Proof i.e. copy of valid passport / driving license / pan card/ voter ID card /Copy of bank account statement for

last 6 months, Saving as well as current accounts. In case of bank take over, copy of home loan account

statement for the entire period shall be obtained/Also a certificate from the lending institution giving pre-

closure amount./Affidavit as per Format.

Title clearance report from advocate and valuation report from architect on Bank's panel alongwith all

required Documents/papers relating to title deeds of property be submitted