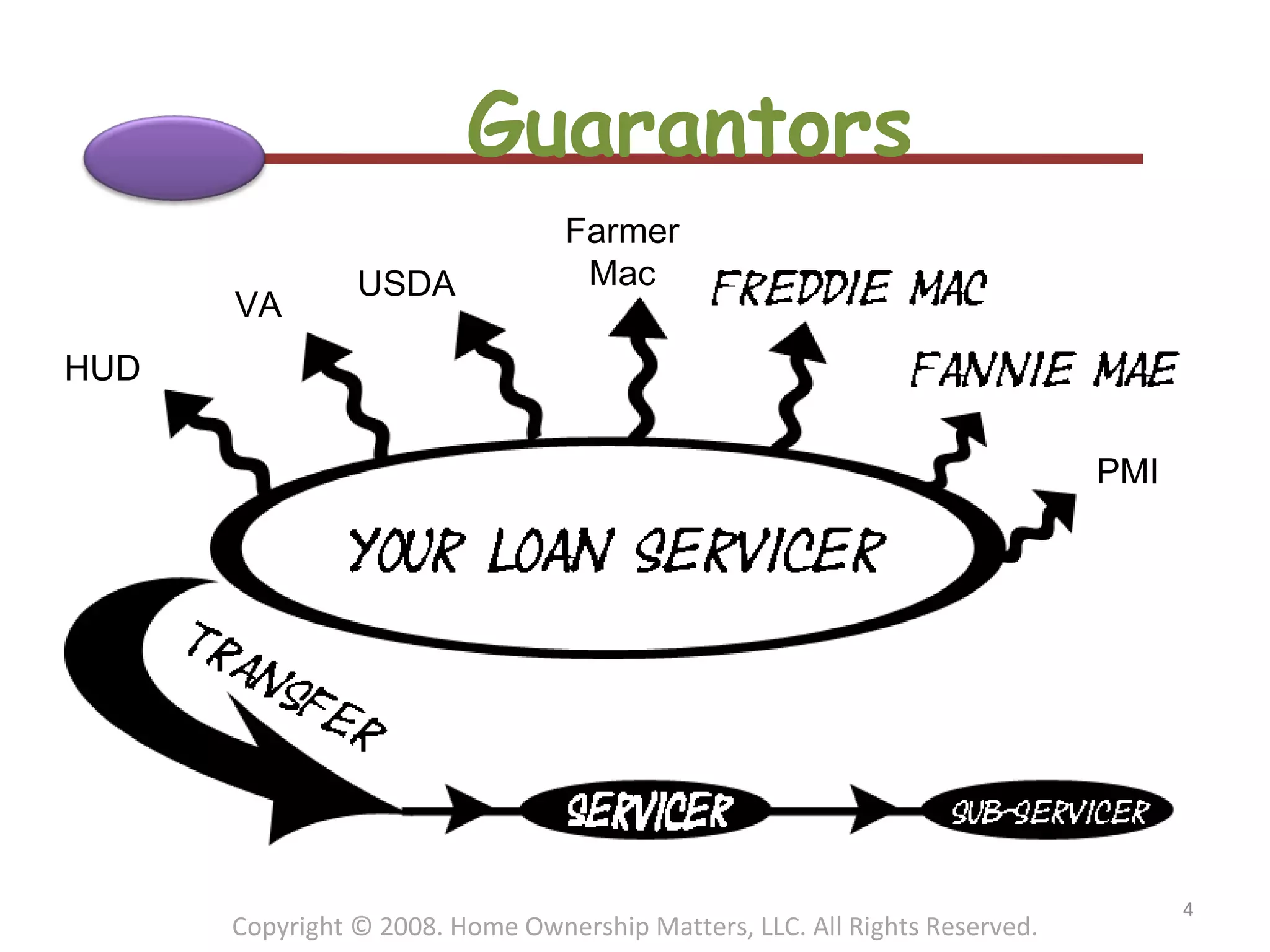

The document offers guidance for individuals facing issues with uncooperative lenders, outlining steps to find their specific servicer and seek assistance through various government and private loan resources. It emphasizes the importance of researching current procedures and legal rights regarding housing situations, while also providing a list of webinars and additional resources for consumers. A disclaimer indicates that the information is for community service purposes and advises seeking legal counsel for specific situations.